Current Mortgage Refinance Rates in Idaho Today

Apply online or call for a complimentary mortgage consultation.

Compare mortgage refinance rates in Idaho.

Key Points

• Mortgage refinancing can help reduce monthly payments, shorten a loan’s duration, or unlock home equity.

• Mortgage refinance rates in Idaho are influenced by the 10-year U.S. Treasury Note and housing inventory levels, among other factors.

• Borrowers who can manage somewhat higher monthly payments might refinance to a 15-year mortgage and pay less in total interest over the life of the loan.

• VA refinances, supported by the U.S. Department of Veterans Affairs, are known for their competitive interest rates, making them a smart choice for those who qualify and are eligible in Idaho.

• A refinance might cause a slight, temporary drop in the borrower’s credit score due to the hard credit inquiry.

Introduction to Mortgage Refinance Rates

Mortgage refinancing is the process of replacing your current home loan with a new one featuring updated terms and a different interest rate. Whether your goal is to lower your monthly payments, pay off your loan sooner, or take cash out of your home, the type of mortgage refinance you choose will play a big role in the interest rate you get. Below, we’ll explain how mortgage refinance rates are determined and give you some tips for getting the best rate possible. We’ll also cover the latest mortgage refinance rates in Idaho to help you make an informed decision.

💡 Quick Tip: How soon can you refinance your mortgage? It varies by loan type, but typical waiting periods are 6 to 12 months.

Where Do Mortgage Refi Interest Rates Come From?

Current mortgage rates for a refinance are a product of various economic and personal financial factors. On a large scale, they’re influenced by the bond market, specifically in the performance of the 10-year U.S. Treasury Note. When the rates on the note rise, mortgage interest tends to rise as well.

Another factor is the performance of the housing market. When the market cools and more homes are available than there are buyers, lenders may lower rates to keep attracting customers. A strong jobs market and economic growth can lead interest rates to rise, while a recession is usually accompanied by lower interest rates.

How Interest Rates Affect Home Affordability

Your monthly payment is a product of your loan amount, repayment term, and interest rate, so interest rates play a big role in the affordability of your refinance. The chart below shows how different interest rates affect the size of the monthly payment and the total interest paid on a $200,000 loan.

| Interest Rate | Monthly Payment | Total Interest |

|---|---|---|

| 6.00% | $1,199 | $231,677 |

| 6.50% | $1,264 | $255,085 |

| 7.00% | $1,330 | $279,021 |

| 7.50% | $1,398 | $303,403 |

| 8.00% | $1,467 | $328,309 |

Why Refinance in Idaho?

Homeowners refinance their mortgages for various reasons. If interest rates are lower than your current rate, refinancing could certainly save you money. To qualify for a refinance, you typically need at least 20% equity in your home. Here are more reasons to consider a refinance.

Common Reasons to Refinance a Mortgage

• Your credit score has improved (or rates have declined), and you can qualify for a lower interest rate than you currently have.

• You want to change your repayment terms, either for lower monthly payments (which may mean a longer term) or for a faster loan payoff.

• You want to cash out some home equity to cover expenses like college or home improvements or to cover some higher-interest debt.

• You want to transition from an adjustable-rate mortgage to a fixed rate (or vice versa).

• You’d like to ditch the FHA mortgage insurance premium on your FHA loan once you’ve hit the 20% equity mark.

Think about Idaho refinance rates when considering these options.

How to Get the Best Available Mortgage Refi Interest Rate

To secure the best mortgage refinance rate, these are some key moves to make before you apply for a new loan. Think of this as how to refinance a mortgage in Idaho:

• Take good care of your credit score by paying your bills on time and sidestepping new debt.

• Aim for a debt-to-income (DTI) ratio of 36% or less. (Your DTI ratio is your monthly debts divided by your gross monthly income, multiplied by 100.)

• Think about whether your budget can accommodate the purchase of discount points. Also known as mortgage points, each one will cost about 1% of your principal amount and will reduce your interest rate — how large a reduction will depend on the lender.

• Determine how large a monthly payment you can afford. A shorter loan term, as we’ve noted, may mean a higher monthly payment but will result in less interest paid over the long haul.

While you’re taking the steps above, it also pays to become familiar with Idaho mortgage rates.

Understand Trends in Idaho Mortgage Interest Rates

Over the past few years, mortgage rates have been on a bit of a rollercoaster. In January 2021, the national average for a 30-year fixed mortgage hit a historic low of 2.65%. By 2023, that number had jumped to 7.79%. Here’s a look at trends in Idaho and nationally.

Historical U.S. Mortgage Interest Rates

If you’re awaiting an interest rate drop, understanding the longer history of U.S. mortgage rates can help you get some perspective on the current landscape. As the graphic below shows, there was a long span of time when rates sat comfortably under 5.00%. In more recent years, they have trended upward.

Historical Interest Rates in Idaho

Idaho’s mortgage refinance rates have generally followed national trends, with rates rising and falling in line with changes in the broader interest rate environment. It’s worth noting that it would be unusual for the average rate in Idaho to fall by more than a percentage point year to year.

| Year | Idaho Rate | National Rate |

|---|---|---|

| 2000 | 7.77 | 8.14 |

| 2001 | 6.93 | 7.03 |

| 2002 | 6.53 | 6.62 |

| 2003 | 5.66 | 5.83 |

| 2004 | 5.63 | 5.95 |

| 2005 | 5.86 | 6.00 |

| 2006 | 6.49 | 6.60 |

| 2007 | 6.43 | 6.44 |

| 2008 | 5.99 | 6.09 |

| 2009 | 5.00 | 5.06 |

| 2010 | 4.79 | 4.84 |

| 2011 | 4.67 | 4.66 |

| 2012 | 3.73 | 3.74 |

| 2013 | 3.83 | 3.92 |

| 2014 | 4.19 | 4.24 |

| 2015 | 3.91 | 3.91 |

| 2016 | 3.72 | 3.72 |

| 2017 | 4.08 | 4.03 |

| 2018 | 4.62 | 4.57 |

Choose the Right Mortgage Refi Type

Interest rates vary depending on the type of mortgage refi you’re considering. Here are a few of the more popular options:

Conventional Refi

Conventional refinance loans, also known as rate-and-term refinances, often have higher interest rates than government-backed FHA and VA loans. But conventional loans are a good option for homeowners who want to lower their interest rate or change their loan term. To be eligible for a conventional refinance, you will need a minimum credit score and adequate equity in your home. Two common types are the 15-year refinance and the adjustable-rate refinance.

15-Year Mortgage Refi

It can be a smart move to refinance into a 15-year mortgage. Yes, it means higher monthly payments, but you stand to save substantial interest over the life of the loan. If you owed $350,000 on your mortgage and refinanced into a 15-year loan at 6.50%, your monthly payment would be $3,049 and you would pay a total of $198,798 in interest. Choosing a 30-year term would lower the monthly payment to $2,212 but increase the interest paid to $446,406.

Adjustable-Rate Mortgage Refi

Adjustable-rate mortgages (ARMs) start with a lower interest rate than fixed-rate loans, making them appealing for homeowners who plan to move before the rate adjusts. If you currently have a 30-year fixed-rate mortgage but anticipate leaving your home within a few years, switching to an ARM could lower your monthly payments. However, it’s important to understand the potential for rate increases in the future. (Some people, on the other hand, refinance out of an ARM and into a fixed-rate loan because they think rates will rise in the future and they want a predictable monthly payment.)

Cash-Out Refi

A cash-out refinance is a smart way to make your home’s equity work for you. Imagine your home is valued at $500,000 and you still owe $300,000 on your mortgage. That leaves you with $200,000 in equity. A lender might allow you to borrow up to 80% of that equity in a cash-out refi. You can use the extra cash for any purpose. It’s a popular solution for debt consolidation and renovations. While the rates for cash-out refis can be a bit higher, the financial flexibility they provide can be well worth it.

FHA Refi

An FHA loan refinance, insured by the Federal Housing Administration, often comes with an attractive low interest rate. If you already have an FHA loan, you can opt for an FHA Simple Refinance or an FHA Streamline Refinance, which simplifies the process. For those without an FHA loan, options include an FHA cash-out refinance or an FHA 203(k) refinance (the latter is designed for home renovations).

VA Refi

A VA loan refinance, backed by the U.S. Department of Veterans Affairs, offers some of the lowest interest rates available. The VA Interest Rate Reduction Refinance Loan (IRRRL) can help you secure a lower interest rate or move from an adjustable-rate mortgage to a fixed-rate one. VA refinance rates offer significant savings and financial flexibility for those who qualify.

Compare Mortgage Refi Interest Rates

Snagging a competitive mortgage rate can save you thousands of dollars on mortgage refinancing costs. Here are some tips:

• Shop around and compare current mortgage refinance rates in Idaho to find the best deal.

• When you’re comparing offers, look at the annual percentage rate (APR) to get a full picture of the costs, including fees and mortgage points.

• Think about the trade-off between rate and fees; lower rates often come with higher costs. Some lenders offer a no-closing-cost refinance but may have higher interest rates instead.

An online refinance calculator will be a valuable tool during this process.

Use an Online Refinance Calculator

Online refinance calculators are a great way to get a rough estimate of what your new monthly payments and potential savings could be. You can put in different interest rates and loan terms to see how different offers compare. Here are a few of our favorite calculators.

Run the numbers on your home loan.

-

Mortgage calculator

Punch in your home loan amount and a new interest rate, and we’ll estimate your payoff date.

-

Down payment calculator

Enter a few details about your home loan and we’ll provide your monthly mortgage payment.

-

Home affordability calculator

Provide us with a few details and see how much you can afford to spend on a home purchase.

Using the free calculators is for informational purposes only, does not constitute an offer to receive a loan, and will not solicit a loan offer. Any payments shown depend on the accuracy of the information provided.

The Takeaway

Refinancing your mortgage can be a powerful way to manage debt and improve your financial situation. Whether you want to lower your interest rate, shorten your loan term, or tap into your home’s equity, it’s important to understand the different refinance options available. By getting your financial house in order and shopping around for the best mortgage refinance rates in Idaho, you can make a smart decision that helps you reach your financial goals.

SoFi can help you save money when you refinance your mortgage. Plus, we make sure the process is as stress-free and transparent as possible. SoFi offers competitive fixed rates on a traditional mortgage refinance or cash-out refinance.

A mortgage refinance could be a game changer for your finances.

FAQ

When is it a good idea to refinance?

It’s a savvy financial play to refinance if you can snag a lower interest rate, consolidate debts, or pay off your loan faster. The key is to figure out at what point the money you spend on refinancing in the form of closing costs, discount points, and other fees is outweighed by the money you save in the refinancing process. How long do you plan to stay in the home? If you think you might move before you’ve recouped the cost, a refi may not make sense.

Can I ask my lender to lower my rate?

You can have a conversation with your lender and ask for a lower interest rate on your existing mortgage loan. If you’ve been diligent about making your payments on time, and your credit score is in good standing, your lender might just be open to the idea. But it’s also possible that the lender will instead suggest a refinance or a mortgage recast (which involves paying down a portion of the principal and then recomputing future payments).

How much are closing costs on a refinance?

On average, closing costs typically range from 2% to 5% of the loan amount. So for a $350,000 refinance, you might be looking at $7,000 to $17,500. The final figure can vary based on a few things, like where your property is located, the type of loan you’re getting, and your lender. Keep in mind that these costs can significantly impact the overall price of your loan.

How many times can you refinance your home loan?

There are no limits on how many times you can refinance your home. However, each time you do, you will have to pay closing costs and your credit score could be affected. And even the smoothest refinance takes time and energy. So it’s important to think about the pros and cons before you refinance to ensure that it makes sense for your financial situation.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

†Veterans, Service members, and members of the National Guard or Reserve may be eligible for a loan guaranteed by the U.S. Department of Veterans Affairs. VA loans are subject to unique terms and conditions established by VA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. VA loans typically require a one-time funding fee except as may be exempted by VA guidelines. The fee may be financed or paid at closing. The amount of the fee depends on the type of loan, the total amount of the loan, and, depending on loan type, prior use of VA eligibility and down payment amount. The VA funding fee is typically non-refundable. SoFi is not affiliated with any government agency.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Qualifying for the reward requires using a real estate agent that participates in HomeStory’s broker to broker agreement to complete the real estate buy and/or sell transaction. You retain the right to negotiate buyer and or seller representation agreements. Upon successful close of the transaction, the Real Estate Agent pays a fee to HomeStory Real Estate Services. All Agents have been independently vetted by HomeStory to meet performance expectations required to participate in the program. If you are currently working with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®. A reward is not available where prohibited by state law, including Alaska, Iowa, Louisiana and Missouri. A reduced agent commission may be available for sellers in lieu of the reward in Mississippi, New Jersey, Oklahoma, and Oregon and should be discussed with the agent upon enrollment. No reward will be available for buyers in Mississippi, Oklahoma, and Oregon. A commission credit may be available for buyers in lieu of the reward in New Jersey and must be discussed with the agent upon enrollment and included in a Buyer Agency Agreement with Rebate Provision. Rewards in Kansas and Tennessee are required to be delivered by gift card.

HomeStory will issue the reward using the payment option you select and will be sent to the client enrolled in the program within 45 days of HomeStory Real Estate Services receipt of settlement statements and any other documentation reasonably required to calculate the applicable reward amount. Real estate agent fees and commissions still apply. Short sale transactions do not qualify for the reward. Depending on state regulations highlighted above, reward amount is based on sale price of the home purchased and/or sold and cannot exceed $9,500 per buy or sell transaction. Employer-sponsored relocations may preclude participation in the reward program offering. SoFi is not responsible for the reward.

SoFi Bank, N.A. (NMLS #696891) does not perform any activity that is or could be construed as unlicensed real estate activity, and SoFi is not licensed as a real estate broker. Agents of SoFi are not authorized to perform real estate activity.

If your property is currently listed with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®.

Reward is valid for 18 months from date of enrollment. After 18 months, you must re-enroll to be eligible for a reward.

SoFi loans subject to credit approval. Offer subject to change or cancellation without notice.

The trademarks, logos and names of other companies, products and services are the property of their respective owners.

SOHL-Q125-167

More refinance resources.

-

How Much Does It Cost to Refinance a Mortgage?

-

How to Refinance a Home Mortgage Loan

-

7 Signs It’s Time for a Mortgage Refinance

Apply online or call for a complimentary mortgage consultation.

Current Mortgage Refinance Rates in Hawaii Today

Apply online or call for a complimentary mortgage consultation.

Compare mortgage refinance rates in Hawaii.

Key Points

• Mortgage refinancing can be a smart move to save money by lowering your interest rate or changing your loan term, but it’s important to consider the costs and benefits.

• Mortgage refinance rates in Hawaii are influenced by economic factors like Federal Reserve policy and inflation, but your finances (such as your credit score) matter, too.

• Even a 1% drop in the rate for a $300,000 mortgage could mean roughly $170 more in your pocket each month.

• Hawaii refinance rates can differ by loan type, with FHA and VA loans often offering lower rates compared to conventional loans, making them attractive options for eligible borrowers.

• Ever thought about switching to a 15-year mortgage? It could be a smart move, as it often means paying less interest over time, even if your monthly payments go up.

• Remember, refinancing is a financial strategy that should be approached thoughtfully. Consider the costs vs. the potential savings, and explore alternatives such as a HELOC if it fits your needs.

Introduction to Mortgage Refinance Rates

Mortgage refinancing is like hitting the reset button on your home loan. You’re swapping your current mortgage for a new one, and if you play your cards right, you could snag a better deal — think lower monthly payments or a more favorable interest rate.

This guide is your ticket to understanding how refi rates are determined and how to score the best one out there. Whether you’re in Hawaii or any other state, getting a handle on what’s driving the current mortgage rates will put you in the driver’s seat.

💡 Quick Tip: Wondering how to refinance a mortgage? The process, which takes about 30 to 45 days, is similar to when you got your original home loan.

Where Do Mortgage Refi Interest Rates Come From?

Mortgage refinance interest rates are a product of both the economic landscape and your unique financial standing.

Economic factors like Federal Reserve policies, inflation, the bond market, and housing inventory all play a part in the cost of home loans. For instance, high inflation and federal funds rate hikes usually translate to higher mortgage rates. On the flip side, low inflation and a robust bond market can work in your favor. By keeping an eye on these moving parts, you can better predict when the time is right for your refinance. Understanding the local climate for mortgage refinance rates in Hawaii is key to making a savvy move.

Also know that your own personal financial profile will impact your access to refinancing options. Those with higher scores will likely qualify for more favorable interest rates, while those with lower scores will appear less creditworthy to lenders and therefore typically be assessed loftier rates.

How Interest Rates Affect Home Affordability

Interest rates play a significant role in the affordability of your refinance payment. Here’s a closer look: The amount you owe, the time to repay (aka the term of your loan), and the interest rate all come together to determine your monthly payment.

For instance, with a $200,000 loan, a 6.00% interest rate, and a 30-year term, you’re looking at $1,199 a month. But bump that interest rate to 8.00%, and suddenly, you’re paying $1,467 monthly. Over the life of the loan, a lower interest rate could save you close to $100,000. Even a small difference in Hawaii refinance rates can lead to substantial savings.

Also, on the topic on interest rates, it’s smart to focus on the annual percentage rate (APR), because that reflects what you actually pay, including additional fees and charges, to borrow money. The APR can give you a more accurate picture of what you will be spending every month and over the life of the loan.

Why Refinance in Hawaii?

Homeowners refinance for a variety of reasons, each influencing the type of refinance and the interest rate. Here’s a closer look at some specifics, but first, a note. In terms of how soon you can refinance, you can’t necessarily swap out your home loan right away if rates drop. You should have at least 20% equity in your home, especially if you plan to cash out some equity.

Common Reasons to Refinance a Mortgage

Homeowners refinance mortgages for key reasons:

• Lower rates can mean reduced monthly payments and less interest.

• Adjusting your repayment term can help you better manage payments or pay off your loan sooner.

• Refinancing can be a path to accessing home equity for large expenses.

• Switching from an adjustable to a fixed rate may provide financial peace of mind.

• You may be able to eliminate FHA mortgage insurance premiums by refinancing once you have 20% equity.

💡 Quick Tip: Some lenders offer a so-called no-closing-cost refinance. However, that usually means either rolling the closing costs into the new mortgage principal or exchanging them for a higher interest rate.

How to Get the Best Available Mortgage Refi Interest Rate

If refinancing seems like a wise move, follow this advice to secure the best mortgage refinance rate:

• Build your credit score by paying bills promptly (this is the single biggest factor in determining your score) and sidestepping new debt to keep your credit utilization ratio down.

• Keep your debt-to-income ratio under 36%.

• Compare rates and fees from multiple lenders, including your current financial institution if they offer home loans. You might get a favorable rate since you’re already a client.

• Think about buying discount points (often called mortgage points) to lower your interest rate. Although that means putting down more cash upfront, it can lower your monthly payment and the total overall interest you pay.

• Choose the shortest refi term you can manage to minimize the amount of interest you pay over the life of the loan.

These steps can help you optimize your financial strategy and take advantage of the best Hawaii refinance rates available. Worth noting: While the interest rate is important, make sure you stay tuned into the other fees and costs associated with refinancing. Just as with a primary home loan, mortgage refinancing costs usually involve closing costs to the tune of 2% to 6% of the loan amount.

Understand Trends in Hawaii Mortgage Interest Rates

National mortgage rates have been on a bit of a rollercoaster in recent years, as you will learn about in a moment. The rates in Hawaii tend to mirror these fluctuations. What often makes Hawaii a special case in terms of mortgages isn’t the interest rate on loans, but the fact that Hawaii ranks as one of the most expensive states in the U.S. in terms of property values, with a current median of approximately $947,000. Such elevated prices can push many borrowers into the realm of jumbo loans.

That said, if you’re a homeowner in Hawaii, interest rate trends are something to keep in mind if you’re considering refinancing. Here’s some more detailed intel to consider.

Historical U.S. Mortgage Interest Rates

Mortgage interest rates have seen their share of ups and downs, mirroring the ebb and flow of the economy. In 2021, the average 30-year fixed rate was a modest 3.15%. Fast forward to 2023, and we saw a significant jump to 7.00%. Federal Reserve actions, inflation, and the bond market all play a part in these changes. Moving into early 2025, it’s looking like rates will remain higher for longer, though many had hoped the Fed might cut rates by now.

Below is a graph that gives you an overview of how mortgage rates have varied over the last few decades. By familiarizing yourself with these past trends, you may be better equipped to understand these fluctuations, make decisions about your mortgage, and potentially save money by refinancing when rates are low.

Historical Interest Rates in Hawaii

Hawaii refinance rates tend to follow the national trends, but there can be some differences. Here is a chart summarizing almost two decades’ worth of rates, both in Hawaii and in the U.S. overall, for mortgages. This can provide a closer look at how Hawaii rates typically track; as you’ll see, they are usually slightly lower than the national numbers. (Note that the Federal Housing Finance Agency stopped tracking these numbers in 2018, so the chart ends with that year.)

| Year | Hawaii Rate | National Rate |

|---|---|---|

| 2000 | 7.59 | 8.14 |

| 2001 | 6.81 | 7.03 |

| 2002 | 6.44 | 6.62 |

| 2003 | 5.43 | 5.83 |

| 2004 | 5.40 | 5.95 |

| 2005 | 5.73 | 6.00 |

| 2006 | 6.15 | 6.60 |

| 2007 | 6.01 | 6.44 |

| 2008 | 5.73 | 6.09 |

| 2009 | 4.79 | 5.06 |

| 2010 | 4.83 | 4.84 |

| 2011 | 4.58 | 4.66 |

| 2012 | 3.68 | 3.74 |

| 2013 | 3.80 | 3.92 |

| 2014 | 4.16 | 4.24 |

| 2015 | 3.88 | 3.91 |

| 2016 | 3.73 | 3.72 |

| 2017 | 3.99 | 4.03 |

| 2018 | 4.48 | 4.57 |

Choose the Right Mortgage Refi Type

Next, review the mortgage refinance types that may be available to you. Which one is right for you? That will depend on your financial situation and goals. Do you need to lower your monthly bills ASAP, or is your goal to free up some cash from your home equity, or perhaps shorten your loan term? The answer can play an important role in your choice.

Conventional Refi

A conventional refinance, also known as a rate-and-term refi, involves changing the interest rate or loan term of your mortgage. Conventional refis typically come with higher rates than government-backed loans (FHA, VA, USDA), though those loans have specific qualification requirements.

Conventional refinance loans can be suitable for homeowners who want to lower their interest rate or change their repayment term. To get approved, you generally need a minimum credit score (often 620 or higher), sufficient home equity (typically 20%), and a manageable debt-to-income ratio.

Cash-Out Refi

Cash-out refinances offer a way to tap into your home’s equity and get a new mortgage for more than you currently owe. You can then take the difference in cash. Cash-out refis typically have higher interest rates than traditional refis, but they can be a smart way to get a large sum of money for things like home renovations or paying off high-interest debt. For example, if you have a $500,000 home and a $300,000 mortgage, you have $200,000 in equity, and can typically access up to 80% of that amount.

15-Year Mortgage Refi

Switching from a 30-year to a 15-year mortgage by refinancing could help you pay off your debt that much sooner and save big on interest. Sure, the monthly payments are higher, but the long-term savings are impressive.

Here’s an example:

• A 30-year, $1 million loan at 7.50% APR results in a monthly payment of about $6,992 and a total interest of $1,517,167.

• If you refinanced to a 15-year term at 7.00%, your monthly payment jumps to around $8,988. But the total interest paid plummets to approximately $617,891, saving you nearly $900,000.

When you’re weighing your options for mortgage refinance rates in Hawaii, consider the substantial benefits a 15-year refi can bring.

Adjustable-Rate Mortgage Refi

An adjustable-rate mortgage (ARM) can start with a lower interest rate than a fixed-rate loan, but it’s essential to consider that the rate may increase over time based on market conditions. If you’re planning to move before the rate adjusts, an ARM could be a smart financial move. For example, if you have a 30-year fixed-rate mortgage but anticipate leaving your home within a few years, an ARM could lower your monthly payments and save you money in the short term.

One note of caution: When considering an ARM refi, it’s important to monitor mortgage refinance rates in Hawaii and assess your future plans. You want to make sure that, if you wind up not moving when anticipated, you can afford the higher payments that might be due.

FHA Refi

FHA loans, backed by the Federal Housing Administration, are often associated with lower interest rates, sometimes a full percentage point less than conventional loans. Some FHA refinance options are tailored exclusively for existing FHA loan holders, such as the FHA Simple and Streamline Refinances.

However, alternatives like the FHA cash-out refinance or the FHA 203(k) refinance are designed for home improvements and are available to those without an FHA loan. These options can still provide you with competitive mortgage refinance rates in Hawaii and the flexibility to manage your home equity.

VA Refi

VA loans, backed by the U.S. Department of Veterans Affairs, are known for their low interest rates. To qualify for a VA refinance, technically called an interest rate reduction refinance loan (IRRRL), you must already have a VA loan. (These are available to past and present members of the military, as well as some spouses.) This type of refinance can help you secure a lower rate and reduce your monthly payments, making it a valuable option for veterans and eligible borrowers.

Compare Mortgage Refi Interest Rates

To snag the best possible mortgage refinance rate for your situation, follow this advice:

• Compare offers from multiple lenders. It can be smart to get at least a few and see how rates and terms stack up.

• Look at the annual percentage rate (APR), which encompasses interest rates, fees, and discount points.

• Evaluate the total costs, including closing costs and fees. Really zero in on how much you will need upfront and then how much you will be paying every month.

• If possible, build your credit score which can allow you to qualify for more favorable rates and terms.

• Stay informed about market trends to time your refinance effectively. Plenty of websites offer regularly updated numbers.

• Ensure your refinance aligns with your financial goals, whether it’s lowering your rate, changing your term, or accessing equity. Hawaii refinance rates should be a key factor in your decision, but pick the refi loan that will get you where you want to go in terms of, say, raising cash to start a business or lowering your monthlies so you can afford your new baby’s daycare costs.

Use an Online Refinance Calculator

Online refinance calculators can be a fantastic resource for getting a ballpark figure of what your new monthly payments might look like and for comparing different refinance options. These calculators take into account your current loan balance, the new interest rate, and the term of the loan. By inputting your specific details, you can get a clear picture of your potential savings and the impact of refinancing. For example, you can use a refinance calculator to see how much you could save by refinancing at the current mortgage refinance rates in Hawaii. Using these tools can help make the decision-making process easier and more informed.

Run the numbers on your home loan.

-

Mortgage calculator

Punch in your home loan amount and a new interest rate, and we’ll estimate your payoff date.

-

Down payment calculator

Enter a few details about your home loan and we’ll provide your monthly mortgage payment.

-

Home affordability calculator

Provide us with a few details and see how much you can afford to spend on a home purchase.

Using the free calculators is for informational purposes only, does not constitute an offer to receive a loan, and will not solicit a loan offer. Any payments shown depend on the accuracy of the information provided.

The Takeaway

Refinancing your mortgage in Hawaii could be a smart financial move that saves you money or helps you achieve other financial goals. By refinancing, you might be able to snag a lower interest rate, reduce your monthly payment, pay off your loan sooner, or tap into your home equity. But refinancing isn’t free — you’ll need to pay closing costs, and keep an eye on those all-important interest rates to gauge how much you’ll be paying. It’s usually smart to compare offers from a few lenders to find the right fit.

SoFi can help you save money when you refinance your mortgage. Plus, we make sure the process is as stress-free and transparent as possible. SoFi offers competitive fixed rates on a traditional mortgage refinance or cash-out refinance.

A mortgage refinance could be a game changer for your finances.

FAQ

Can I lower my interest rate without refinancing?

Yes, you can lower your interest rate without refinancing by recasting your mortgage. This means you pay a lump sum toward your loan principal, and your lender recalculates and lowers your payments. Another option: If you’re facing financial hardship, you can request a loan modification to change your rate and avoid foreclosure.

Is there a cost to recast your mortgage?

When considering a mortgage recast, it’s smart to factor in any associated fees, although they are typically much more modest compared to refinance fees. Lenders usually charge a fee ranging from $150 to $500 for a mortgage recast, but the exact amount may vary, compared with refi closing costs of 2% to 6% of the loan amount. However, It’s crucial to carefully review the terms and conditions set by the lender before proceeding with a mortgage recast to ensure that it aligns with your financial goals and circumstances.

Can I tap into my home’s equity without refinancing?

Yes, you can pull equity out of your home without refinancing through a home equity loan (for a lump sum against your equity) or a home equity line of credit (HELOC). A HELOC allows you to borrow funds as needed, typically with a variable interest rate, up to a set limit. These sources of funds can help homeowners who want to use the equity in their home for things like home improvements, debt consolidation, or paying for college.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

†Veterans, Service members, and members of the National Guard or Reserve may be eligible for a loan guaranteed by the U.S. Department of Veterans Affairs. VA loans are subject to unique terms and conditions established by VA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. VA loans typically require a one-time funding fee except as may be exempted by VA guidelines. The fee may be financed or paid at closing. The amount of the fee depends on the type of loan, the total amount of the loan, and, depending on loan type, prior use of VA eligibility and down payment amount. The VA funding fee is typically non-refundable. SoFi is not affiliated with any government agency.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Qualifying for the reward requires using a real estate agent that participates in HomeStory’s broker to broker agreement to complete the real estate buy and/or sell transaction. You retain the right to negotiate buyer and or seller representation agreements. Upon successful close of the transaction, the Real Estate Agent pays a fee to HomeStory Real Estate Services. All Agents have been independently vetted by HomeStory to meet performance expectations required to participate in the program. If you are currently working with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®. A reward is not available where prohibited by state law, including Alaska, Iowa, Louisiana and Missouri. A reduced agent commission may be available for sellers in lieu of the reward in Mississippi, New Jersey, Oklahoma, and Oregon and should be discussed with the agent upon enrollment. No reward will be available for buyers in Mississippi, Oklahoma, and Oregon. A commission credit may be available for buyers in lieu of the reward in New Jersey and must be discussed with the agent upon enrollment and included in a Buyer Agency Agreement with Rebate Provision. Rewards in Kansas and Tennessee are required to be delivered by gift card.

HomeStory will issue the reward using the payment option you select and will be sent to the client enrolled in the program within 45 days of HomeStory Real Estate Services receipt of settlement statements and any other documentation reasonably required to calculate the applicable reward amount. Real estate agent fees and commissions still apply. Short sale transactions do not qualify for the reward. Depending on state regulations highlighted above, reward amount is based on sale price of the home purchased and/or sold and cannot exceed $9,500 per buy or sell transaction. Employer-sponsored relocations may preclude participation in the reward program offering. SoFi is not responsible for the reward.

SoFi Bank, N.A. (NMLS #696891) does not perform any activity that is or could be construed as unlicensed real estate activity, and SoFi is not licensed as a real estate broker. Agents of SoFi are not authorized to perform real estate activity.

If your property is currently listed with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®.

Reward is valid for 18 months from date of enrollment. After 18 months, you must re-enroll to be eligible for a reward.

SoFi loans subject to credit approval. Offer subject to change or cancellation without notice.

The trademarks, logos and names of other companies, products and services are the property of their respective owners.

SOHL-Q125-166

More refinance resources.

-

How Much Does It Cost to Refinance a Mortgage?

-

How to Refinance a Home Mortgage Loan

-

7 Signs It’s Time for a Mortgage Refinance

Apply online or call for a complimentary mortgage consultation.

Current Mortgage Refinance Rates in Connecticut Today

CONNECTICUT MORTGAGE REFINANCE RATES TODAY

Current mortgage refinance rates in

Connecticut.

Apply online or call for a complimentary mortgage consultation.

Compare mortgage refinance rates in Connecticut.

Key Points

• Mortgage refinance rates are influenced by many factors, including your credit history — as well as Federal Reserve policy, inflation, and the bond market.

• Connecticut refinance rates have seen their share of ups and downs, ranging from 3.15% in 2021 to 6.89% in 2025, similar to rates nationwide.

• A 1% drop in your mortgage interest rate can lead to significant monthly savings, and may be worth considering.

• Consider the benefits of a 15-year mortgage, which can save you a substantial amount in interest over the life of the loan, despite the higher monthly payments.

• VA refinances, supported by the U.S. Department of Veterans Affairs, offer some of the most competitive mortgage refinance rates in Connecticut, but they come with specific eligibility criteria.

• When considering a refi, remember to account for closing costs: typically between 2% and 5% of the loan amount.

Introduction to Mortgage Refinance Rates

Refinancing your mortgage is almost like getting a clean slate. You take out a new loan to replace your current one, with new terms and a new interest rate.

Whether you want to reduce your monthly payment, pay off your loan faster, or withdraw some of your home equity as cash (called a cash-out refinance), the type of refinancing you choose will play a big role in the rate you get.

This guide will help you understand how refinance rates are set in general — and how you can get the lowest rate possible for a refi in Connecticut. This can help you decide if a refinance is right for you, and start the application process.

💡 Quick Tip: Some lenders offer a so-called no-closing-cost refinance. However, that usually means either rolling the closing costs into the new mortgage principal or exchanging them for a higher interest rate.

Where Do Mortgage Refi Interest Rates Come From?

Current mortgae ratesare the result of a complex interplay of economic factors and your personal financial situation. Key economic factors include:

• Federal Reserve policy

• Inflation

• The bond market

• Housing inventory levels

In general, higher inflation and more aggressive rate hikes lead to higher mortgage rates. Conversely, periods of low inflation and bond market rallies can lead to lower rates. Homeowners should keep an eye on these factors to get a sense of where rates are headed.

Understanding how these factors may influence Connecticut refinance rates can help you make smarter choices about your own refinancing choices, and decide when the time is right for you to refinance your home loan.

How Interest Rates Affect Home Affordability

As you know, interest rates play a big role in making your refinance payment affordable. Your monthly payment is a product of your loan amount, the time you have to repay it, and the interest rate, in addition to mortgage refinancing costs.

For instance, with a $300,000 loan, a 6.00% interest rate, and a 30-year term, you’re looking at a $1,799 monthly payment. But bump that interest rate to 7.00%, and suddenly you’re paying $1,996 — about $200 more per month.

Over the life of the loan, having a lower interest rate could save you close to $70,000. So keep an eye on Connecticut refinance rates to make sure you’re getting the best deal.

| Interest Rate | Loan Term | Monthly Payment | Total Interest |

|---|---|---|---|

| 6.00% | 30-year | $1,799 | $347,515 |

| 6.00% | 15-year | $2,532 | $155,683 |

| 7.00% | 30-year | $1,996 | $418,527 |

| 7.00% | 15-year | $2,697 | $185,367 |

Why Refi?

A mortgage refinance can be a strategic move that can support a range of financial needs and goals.

Picture this: If the current interest rates are playing in your favor, you could be looking at lower monthly payments and long-term savings. It’s a smart move to have at least 20% equity in your home before you take the leap, especially if you’re eyeing the opportunity to cash out some equity.

You may want to consider how soon can you refinance a mortgage, because you want enough of a difference between your current rate and the new rate to make it worthwhile.

Another factor: If you’re tired of the unpredictability of an adjustable-rate loan, switching to a fixed-rate one could provide just the stability you’re after. You just want to be sure to compare different Connecticut refinance rates to land the best deal.

Common Reasons to Refinance a Mortgage

Here are common reasons homeowners refinance:

• Rates are more attractive due to the homeowner’s improved credit, or simply owing to market changes.

• Homeowners may wish to either ease monthly payments or pay off their loan faster.

• They plan to cash out home equity for their financial goals.

• There’s a desire to switch from an adjustable-rate mortgage to a fixed rate.

• It’s possible to ditch mortgage insurance once the homeowner has 20% equity.

• They want to roll high-interest debt into a lower-rate mortgage.

How to Get the Best Available Interest Rate

Securing a competitive mortgage refinance rate is crucial, and there are various levers you can pull to ensure the best rate. Here’s how to refinance your mortgage effectively:

• Boost your credit score by making on-time payments and avoiding new debt.

• Keep your debt-to-income ratio under 36%.

• Shop around and compare rates and fees from multiple lenders.

• Think about purchasing mortgage points to reduce your interest rate.

• Choose a shorter loan term, like 10 or 15 years, for potentially lower rates (although your payment will likely be higher; you’ll still pay less over time).

Next step is to keep an eye on Connecticut mortgage interest rate trends. Here’s how.

Trends in Connecticut Mortgage Interest Rates

Connecticut’s mortgage rates have been on a wild ride in recent years, along with most other states. The average 30-year fixed mortgage rate in the U.S. was 3.15% in 2021, but it jumped to nearly 7.80% in 2023. Rates then went back on a rollercoaster for most of 2024, fluctuating between about 7.22% earlier in the year, dipping down to about 6.0% that summer, and ending the year closer to 6.90%.

Fortunately, 2025 shows some moderation. But while experts predicted rates might continue to trend lower, the March 2025 meeting of the Federal Reserve suggests that rates will stay more or less where they are for the year: about 6.68%. That could change if there is a shift in policy or another significant event. So it’s best to keep an eye on current mortgage refinance rates before deciding if and when to refinance.

Historical U.S. Mortgage Interest Rates

Mortgage interest rates in the United States have seen their fair share of ups and downs over the years, as many home buyers and home refinancers know.

As noted, back in 2021 the average 30-year fixed rate was a mere 3.15%, giving homeowners a golden opportunity to lock in some very attractive terms. By late 2022, though, that 30-year average rate had surged — rising close to 7.80% toward the end of 2023.

Thankfully, rates moderated in 2024 — although there was still some volatility — with the average 30-year fixed rate hovering at 6.65%, as of March 27, 2025.

Historical Interest Rates in Connecticut

For the most part, Connecticut refinance rates have followed the same patterns as refinance rates in the rest of the country. When national rates are low, Connecticut rates trend lower. When national rates are high, Connecticut rates also move higher.

As noted, rates have been on a rollercoaster ride in the last few years, but may be leveling off for the rest of 2025 — something to keep in mind, as you weigh your refi.

| Year | Connecticut Rate | National Rate |

|---|---|---|

| 2000 | 7.96 | 8.14 |

| 2001 | 7.06 | 7.03 |

| 2002 | 6.51 | 6.62 |

| 2003 | 5.72 | 5.83 |

| 2004 | 5.67 | 5.95 |

| 2005 | 5.77 | 6.00 |

| 2006 | 6.44 | 6.60 |

| 2007 | 6.42 | 6.44 |

| 2008 | 6.09 | 6.09 |

| 2009 | 4.99 | 5.06 |

| 2010 | 4.92 | 4.84 |

| 2011 | 4.60 | 4.66 |

| 2012 | 3.67 | 3.74 |

| 2013 | 3.84 | 3.92 |

| 2014 | 4.19 | 4.24 |

| 2015 | 3.90 | 3.91 |

| 2016 | 3.69 | 3.72 |

| 2017 | 3.92 | 4.03 |

| 2018 | 4.57 | 4.57 |

Choose the Right Mortgage Refi Type

Here’s another thing to keep in mind: Mortgage refinancing rates vary by the type of refinancing you’re considering. Let’s take a closer look.

Conventional Refi

A conventional refinance, also known as a rate-and-term refi, is like hitting the reset button on your mortgage. You replace your current loan with a new one, ideally scoring a lower interest rate or adjusting the term.

While these refis generally come with higher rates than government-backed loans such as FHA, VA, or USDA loans, they can also offer more flexibility and fewer restrictions. To qualify, a good credit score and at least 20% equity in your home are typically required. Be sure to compare Connecticut refinance rates for conventional loans to snag the best deal.

Two examples of a conventional mortgage refi are a 15-year term refi and an adjustable-rate refi.

15-Year Refi

Opting for a 15-year mortgage refinance could be a game-changer, slashing your total interest payments, even if the monthly installments are a bit steeper.

Let’s say you have a 30-year, $500,000 loan at 6.80% interest, which translates to roughly $3,259 per month and total interest paid of $673,462.

By switching to a 15-year term at 5.80%, your monthly payment would climb to about $4,189, but the total interest would plummet to approximately $249,780, saving you over $400,000.

Adjustable-Rate Refi

Adjustable-rate mortgages (ARMs) often kick off with a lower interest rate than fixed-rate loans, which might be just the ticket if you’re planning to refinance (or sell your home) before the rate adjusts. You just have to understand the terms, when and how often the mortgage rate adjusts, and what you can afford.

For instance, if you currently have a 30-year fixed-rate mortgage, but are considering a move within a handful of years, switching to an ARM could translate to lower monthly payments. However, it’s essential to keep in mind that rates have the potential to rise at any point, which could mean your monthly payments would likewise increase.

Cash-Out Refinancing

With a cash-out refinance, you can leverage your home equity to receive a lump sum, which can help you fund various goals, from home improvements to debt management.

For example, if your home is valued at $500,000 and you owe $300,000 on your current mortgage, that gives you about $200,000 in equity. A lender might offer you up to 80% of your equity, which could mean an additional $100,000 in your pocket after settling your existing mortgage. Depending on the current refinance rates in Connecticut, this could be a good deal.

FHA Loan Refi

FHA refinances, insured by the Federal Housing Administration, often offer lower interest rates, making them an appealing choice for homeowners seeking to trim their monthly payments — as long as you meet the eligibility terms. If you already have an FHA loan, you can choose between an FHA Simple Refinance or an FHA Streamline Refinance.

For those without an existing FHA loan, you have the option of an FHA cash-out refinance or an FHA 203(k) refinance, tailored for home improvements. Both avenues can lead to competitive Connecticut refinance rates and increased financial flexibility.

Refinancing with the VA

VA refinances, fully backed by the U.S. Department of Veterans Affairs, are designed to meet the financial needs of veterans. They offer some of the most competitive interest rates available in the market.

The Interest Rate Reduction Refinance Loan (IRRRL) is specifically for individuals with existing VA loans. This loan can help you secure a lower interest rate or switch from an adjustable to a fixed interest rate. While VA loans have strict eligibility requirements, they offer a unique opportunity for veterans to save money.

How to Compare Mortgage Refi Interest Rates

So now you know all the tricks for getting a lower refi interest rate. When you’re ready to pull the trigger, these are the steps you should take:

• Compare rates and fees from multiple lenders. Think about the trade-off between rate and fees.

• Focus on the APR (annual percentage rate), which includes fees, closing costs, and any discount points. This gives you a more accurate comparison than interest rates alone.

• Take care of your credit score, debt-to-income ratio, and home value to secure the best rates.

• Using a mortgage calculator to estimate your monthly payments.

Online Refinance Calculators

Using the right mortgage calculator can help you get a clearer sense of what your new monthly payment might be, and compare different refinance options.

Using a calculator is smart because it takes into account your current loan balance, the new interest rate, and the term of the loan to show you what your potential savings could be. This can help you make a more informed decision about whether refinancing is right for you.

You can also use a calculator to estimate how much equity is in your home, if you’re considering a home equity loan.

Run the numbers on your home loan.

-

Mortgage calculator

Punch in your home loan amount and a new interest rate, and we’ll estimate your payoff date.

-

Down payment calculator

Enter a few details about your home loan and we’ll provide your monthly mortgage payment.

-

Home affordability calculator

Provide us with a few details and see how much you can afford to spend on a home purchase.

Using the free calculators is for informational purposes only, does not constitute an offer to receive a loan, and will not solicit a loan offer. Any payments shown depend on the accuracy of the information provided.

The Takeaway

Mortgage refinancing is a useful financial tool that can help you reduce your monthly payments, consolidate debt, or tap into your home’s equity — when you can secure the best rate. Whether you’re considering a cash-out refinance, an FHA refinance, a VA refinance, or a 15-year mortgage refinance, be sure to weigh your financial goals against the requirements of each loan type, as well as the cost of refinancing itself.

By boosting your credit score, lowering your debt-to-income ratio, and carefully comparing mortgage rates in Connecticut, you can obtain better loan terms so that a refi makes sense.

SoFi can help you save money when you refinance your mortgage. Plus, we make sure the process is as stress-free and transparent as possible. SoFi offers competitive fixed rates on a traditional mortgage refinance or cash-out refinance.

A mortgage refinance could be a game changer for your finances.

FAQ

When is it a good idea to refinance your home?

The general rule of thumb is to refinance when you can get a significantly lower interest rate. Refinancing to a new, lower rate could help lower your monthly payments, pay off your loan faster, and build equity in your home more quickly. Alternatively, you may want to refinance to switch your ARM for a fixed-rate loan, or to remove a cosigner. Generally, the faster you can recoup your closing costs, the better.

How does refinancing affect your credit score?

Refinancing may cause a temporary dip in your credit score due to the hard inquiry and the new account that will show up on your credit report, assuming you take out the new loan. But the impact is usually minor and can be outweighed by the benefits of the lower mortgage rate. Be sure to consider all angles when researching a refi.

Do you have to pay closing costs when you refinance?

Yes, you’ll have to pay closing costs when you refinance your home. These costs can range from 2% to 5% of the loan amount, which can be a significant expense: from $6,000 to $15,000 on a $300,000 loan.

How much does a 1% lower rate change your payment?

A 1% reduction in your mortgage interest rate can make a big difference in your monthly payment. For example, the current Connecticut refinance rates are 6.88% for a 30-year fixed-rate loan. If you can reduce your interest rate by 1%, you can potentially save hundreds of dollars each month.

Can I lower my interest rate without refinancing?

If you’ve got some money to put down and you’re looking to lower your monthly mortgage payment, you might want to consider a mortgage recast. This is where you make a lump sum payment to your principal balance, and your lender re-amortizes the loan, which can lower your monthly payments. Another option is to request a loan modification directly from your lender. If you have a good credit score and a history of on-time payments, you may be able to get a lower interest rate without having to pay the cost of a full-on refi.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

†Veterans, Service members, and members of the National Guard or Reserve may be eligible for a loan guaranteed by the U.S. Department of Veterans Affairs. VA loans are subject to unique terms and conditions established by VA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. VA loans typically require a one-time funding fee except as may be exempted by VA guidelines. The fee may be financed or paid at closing. The amount of the fee depends on the type of loan, the total amount of the loan, and, depending on loan type, prior use of VA eligibility and down payment amount. The VA funding fee is typically non-refundable. SoFi is not affiliated with any government agency.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Qualifying for the reward requires using a real estate agent that participates in HomeStory’s broker to broker agreement to complete the real estate buy and/or sell transaction. You retain the right to negotiate buyer and or seller representation agreements. Upon successful close of the transaction, the Real Estate Agent pays a fee to HomeStory Real Estate Services. All Agents have been independently vetted by HomeStory to meet performance expectations required to participate in the program. If you are currently working with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®. A reward is not available where prohibited by state law, including Alaska, Iowa, Louisiana and Missouri. A reduced agent commission may be available for sellers in lieu of the reward in Mississippi, New Jersey, Oklahoma, and Oregon and should be discussed with the agent upon enrollment. No reward will be available for buyers in Mississippi, Oklahoma, and Oregon. A commission credit may be available for buyers in lieu of the reward in New Jersey and must be discussed with the agent upon enrollment and included in a Buyer Agency Agreement with Rebate Provision. Rewards in Kansas and Tennessee are required to be delivered by gift card.

HomeStory will issue the reward using the payment option you select and will be sent to the client enrolled in the program within 45 days of HomeStory Real Estate Services receipt of settlement statements and any other documentation reasonably required to calculate the applicable reward amount. Real estate agent fees and commissions still apply. Short sale transactions do not qualify for the reward. Depending on state regulations highlighted above, reward amount is based on sale price of the home purchased and/or sold and cannot exceed $9,500 per buy or sell transaction. Employer-sponsored relocations may preclude participation in the reward program offering. SoFi is not responsible for the reward.

SoFi Bank, N.A. (NMLS #696891) does not perform any activity that is or could be construed as unlicensed real estate activity, and SoFi is not licensed as a real estate broker. Agents of SoFi are not authorized to perform real estate activity.

If your property is currently listed with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®.

Reward is valid for 18 months from date of enrollment. After 18 months, you must re-enroll to be eligible for a reward.

SoFi loans subject to credit approval. Offer subject to change or cancellation without notice.

The trademarks, logos and names of other companies, products and services are the property of their respective owners.

SOHL-Q125-162

More refinance resources.

-

How Much Does It Cost to Refinance a Mortgage?

-

How to Refinance a Home Mortgage Loan

-

7 Signs It’s Time for a Mortgage Refinance

Apply online or call for a complimentary mortgage consultation.

Is 706 a Good Credit Score?

Is 706 a Good Credit Score?

A credit score of 706 is considered good, and it may qualify you for more competitive rates and lending options. However, it’s not high enough to land in the very good or exceptional credit score range. As a result, you may not get the best rates possible, and you might not qualify for premium credit cards.

Let’s take a deeper look into the meaning of a 706 credit score and what you need to know about your borrowing options.

Key Points

• A 706 credit score qualifies borrowers for various credit cards, including travel and cash-back options.

• A 706 credit score can lead to competitive interest rates on auto loans.

• A 706 credit score is good for mortgage applications, qualifying for competitive rates.

• A 706 credit score is sufficient for personal loans with competitive rates.

• Strategies to improve a 706 credit score include timely payments, low credit utilization, and maintaining old accounts.

What Does a 706 Credit Score Mean?

Your credit score is a three-digit number that represents your creditworthiness, or how likely you are to repay the money you borrow. The two most common credit scoring models are FICO® and VantageScore. FICO, which is used in most lending decisions, calculates your credit score based on your payment history, amounts owed, length of credit history, credit mix, and new credit.

Here’s a look at how FICO Scores are categorized:

• Poor: 300-579

• Fair: 580-669

• Good: 670-739

• Very Good: 740-799

• Excellent: 800-850

A 706 FICO Score shows lenders that you’re a responsible borrower. As we mentioned, they may offer you credit products, though you might not get the lowest interest rates.

What Can You Get with a 706 Credit Score?

Can you get a credit card, auto loan, mortgage, or personal loan with a 706 credit score? Here’s a closer look at each.

Can I Get a Credit Card with a 706 Credit Score?

There’s no universal credit score required to get approved for a credit card. That said, with a credit score of 706, you can likely qualify for a number of credit cards, including travel credit cards and cash-back credit cards.

Can I Get an Auto Loan with a 706 Credit Score?

A 706 credit score can increase the chances you’ll get approved for an auto loan. What’s more, you’ll likely be offered a competitive interest rate.

According to 2024 data from Experian®, borrowers with a “prime” credit score (661-780) receive an average interest rate of 6.87% for a new car loan and 9.36% for a used car loan. In comparison, people with a “superprime” credit score (781-850) receive an average interest rate of 5.25% for a new car loan and 7.13% for a used car loan.

Keep in mind that your credit score is just one factor a lender considers. They’ll also take into account how much you’re borrowing, your debt-to-income ratio, the loan term length, and the type of car you’re buying.

Can I Get a Mortgage with a 706 Credit Score?

You can qualify for a mortgage with a 706 credit score. You may even qualify for a jumbo loan that exceeds the standard loan size. Let’s walk through some common mortgage loan types and their credit score requirements.

•

Conventional loan: Conventional loans typically require a 620 minimum credit score for fixed-rate mortgages, and 640 for adjustable-rate mortgages. A 706 credit score can give borrowers better interest rates and terms.

• FHA loan: These are guaranteed by the Federal Housing Administration. To get an FHA loan, you’ll typically have to have at least a 500 credit score (with a down payment of 10% or higher) or a 580 credit score (with a 3.5% down payment).

• VA loan: This type of loan is backed by the Veterans Administration, and it’s for active-duty military members, veterans, and surviving spouses. The VA doesn’t set a minimum credit score requirement, but lenders generally want to see at least a 620 credit score.

• USDA loan:The U.S. Department of Agriculture (USDA) backs these loans, which encourage purchasers to buy homes in eligible rural areas. Typically, you’ll need a credit score of 620 or higher to qualify.

Can I Get a Personal Loan with a 706 Credit Score?

A personal loan is a type of installment loan — you receive a lump sum and repay your loan every month. You can use the funds for just about anything, including consolidating debt, travel expenses, and large purchases.

Note that personal loans often carry lower interest rates than credit cards.

Each lender has its own credit score requirements for personal loans, and they also weigh other factors, including your debt-to-income ratio and employment. However, a 706 credit score should be more than enough with most major lenders.

It’s a good idea to shop around. You may also want to use a personal loan calculator to determine how much your monthly payments will be based on the rates and terms you’re offered.

How to Build Your Credit

While a credit score of 706 is good, boosting it even higher could qualify you for the best rates and terms. Here are some strategies to consider:

• Make on-time payments: Consistently making payments on time can help you increase your credit score.

• Pay down balances: Try to keep your credit utilization rate low — ideally, aim to use no more than 30% of your credit limit.

Don’t close accounts: Keep old credit accounts open, as this will lengthen your credit history.

• Diversify your credit: Responsibly managing a variety of credit types can help boost your credit score.

• Limit credit applications: Lenders perform a hard inquiry on your credit when you apply for a new loan, so try minimizing the number of times you apply for credit. See if your lender offers prequalification instead, which involves a soft credit check.

• Check your credit report regularly: Inaccuracies can affect your score, so check your report and dispute any inaccuracies with the credit reporting agencies.

The Takeaway

So is a 706 credit score good or bad? Put simply, it’s considered good, and you may be able to qualify for a range of credit options. But to help land the best rates and terms, you’ll want to build your score to the “very good” (740-799) or “exceptional” (800+) category. Making on-time payments, paying down debts, and keeping older accounts open can all help you build up your score.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. See your rate in minutes.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

†Veterans, Service members, and members of the National Guard or Reserve may be eligible for a loan guaranteed by the U.S. Department of Veterans Affairs. VA loans are subject to unique terms and conditions established by VA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. VA loans typically require a one-time funding fee except as may be exempted by VA guidelines. The fee may be financed or paid at closing. The amount of the fee depends on the type of loan, the total amount of the loan, and, depending on loan type, prior use of VA eligibility and down payment amount. The VA funding fee is typically non-refundable. SoFi is not affiliated with any government agency.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOPL-Q125-015

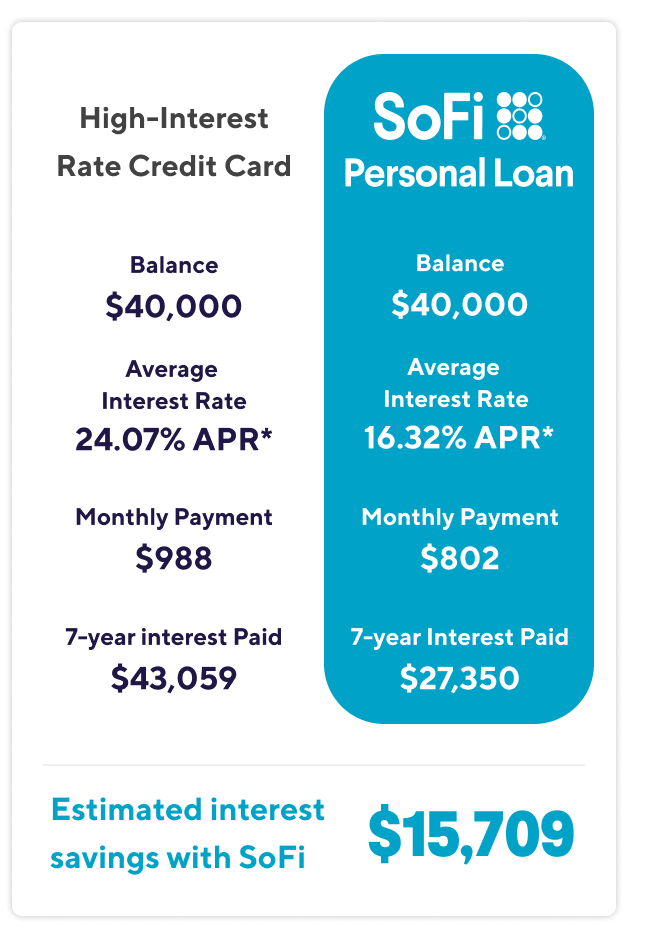

Credit Card Debt Consolidation Loans

Consolidate your credit card debt

with lower interest and save.

-

Low fixed rates

Ditch your high credit card interest and you could save big.

-

No fees required

No origination fees required, plus no prepayment or late fees.

-

One fixed payment

Consolidate multiple debts into one simple monthly payment.

-

$5K to $100K

Get funds as soon as the same day

you sign.‡

View your rate

Real reviews from SoFi members who’ve successfully paid off over $33B in credit card debt.

Ready to join them? Apply for a debt consolidation loan with SoFi.

The savings and experiences of members herein may not be representative of the experiences of all members. Savings are not guaranteed and will vary based on your unique situation and other factors.

Real reviews from SoFi members who’ve successfully paid off over $33B in credit card debt.

Ready to join them? Apply for a debt consolidation loan with SoFi.

The savings and experiences of members herein may not be representative of the experiences of all members. Savings are not guaranteed and will vary, based on your unique situation and other factors.

Received a mailer from

us?

>

Enter confirmation #

A SoFi credit card consolidation loan could help lower monthly payments.

-

Lower interest rates

You could save money by securing a lower fixed APR.

-

Simplified payments

Stop juggling multiple bills. Manage one easy monthly payment.

-

Lower your credit utilization

A personal loan for debt consolidation could help improve your credit score.

-

No fees required

Transparency matters. Enjoy a no-fees-required borrowing experience.

View your rate

What is a credit card consolidation loan? Expand to learn more.

expand={

/>

How does a credit card consolidation loan work?

A personal loan for debt consolidation is a savvy way to potentially save thousands in interest by refinancing high-rate credit cards and existing personal installment loan balances. You could have a clear path to paying off debt, with one fixed monthly payment to budget around and flexible terms from 2 to 7 years. Plus, with Direct Pay, you have the option to receive an even lower fixed rate when you opt to have SoFi pay off your lender(s) directly.

Why SoFi for credit card consolidation loans?

View your rate

Fast and easy application process

View your debt consolidation loan rate in minutes. Literally.

Flexible loan options