Dec

15

2025

Banking Quiz Results

Your Results

Based on your answers, here is the banking style that fits you best.

Analyzing your banking style…

Based on your answers, here is the banking style that fits you best.

Analyzing your banking style…

This article appeared in SoFi's On the Money newsletter. Not getting it? Sign up here.

How do you do the holidays justice when money is tight?

You want to make the holiday season special for your family and friends, and you may feel you need to outdo last year — or at least keep up with everyone else.

Two-thirds of shoppers in a Beyond Finance survey said they feel an unhealthy cultural pressure to buy holiday gifts when they can’t afford them. And 19% admitted they’d bought gifts or trips so they could post about them on social media.

In other words, guilt, FOMO, and Instagram can make it hard not to overspend, even when prices are high and the economy feels increasingly precarious. And yet a monthly Gallup poll showed Americans downsized their holiday gift budgets more than they ever have in the middle of the shopping season: By November they were expecting to spend $778, on average, down from $1,007 in October.

So what can you do to stay true to your budget without going full Grinch? Here are some ground rules that could help:

• Have a holiday heart-to-heart. If you’re facing a cash crunch this season, chances are that some of the people you exchange gifts with are, too. They’ll be relieved when they see your simple group text request: “Santa’s pursestrings are a little tighter this year, so why don’t we try something a little different?”

Be ready with suggestions like a white elephant exchange in which everyone has to buy (and receive) one meaningful price-capped gift rather than presents for everyone. Or set a spending limit for everyone at your celebration to help reduce anxiety and decision fatigue. You could also make it a kids-only gift year.

• Cap it at four gifts. If you have kids and the Santa haul in your house has gotten out of control, adopt the viral “four gift rule.” The idea is simple: Each child gets something they want, something they need, something to wear, and something to read. (You may need it for the adults in your life, too.)

• Set an example. Speaking of kids, it’s easy to think we’re not doing enough for them, and it’s natural to want to take them to a magical theater performance or decorate the house and yard to the nines. But what better way to model living within your means than making your reality a teachable moment.

“Let them know when they’re an adult, some years are going to be better than others,” Mary Clements Evans, a certified financial planner, told Scary Mommy. “Some years, you’re going to have more money than others. If they’re old enough, try to teach them a little bit about inflation. What happens if somebody loses a job? I don’t think you can teach kids those lessons too young.”

• Scale the love. If you have a bunch of relatives or one big friend group on your gift list, consider putting effort into one gift that will make everyone smile — like a digital family greeting, photo collage, or special bread. (According to a recent Deloitte survey, Gen Zs and Millennials are the most likely to make their own gifts this season, including food gifts like baked goods, sauces, and charcuterie.)

• Let tradition trump tickets. Stage shows and fancy New Year’s Eve dinners can get pricey fast. But there are other fun traditions that cost far less (or nothing), and they may end up being more memorable for you and your loved ones. Pile the family in the car with some to-go hot chocolate and look for the coolest light displays. Take everyone ice skating or sledding. Or have a holiday-themed potluck party with karaoke.

• Stock emergency gifts to avoid last-minute expenses. When you need gifts right away, you’re at the mercy of expedited shipping costs or the prices at the only place that’s still open. If you spot a good go-to gift, grab an extra (or two) so you’ll always have something on hand for that person you accidentally left off your list.

• Catch yourself. How did matching family pajamas, elaborate advent calendars, “brrr baskets,” and stocking stuffers pricey enough to be the actual gift infiltrate our holiday gift list? If you’re committed to scaling back, these extras could be a good place to start.

• Ditch the guilt. You don’t have to spend what you spent in the past. If you can get by with $15 gifts for your nieces and nephews, don’t go grabbing something for an additional $10 to make up the difference. This year, take the win.

Learn to Recognize Holiday Spending Triggers (Take Charge America)

30 Amazing Gift Ideas That Cost Next to Nothing (Real Simple)

Are the Discounts Worth Getting That Store Credit Card? (SoFi)

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

SoFi isn't recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

OTM20251215SW

Read more

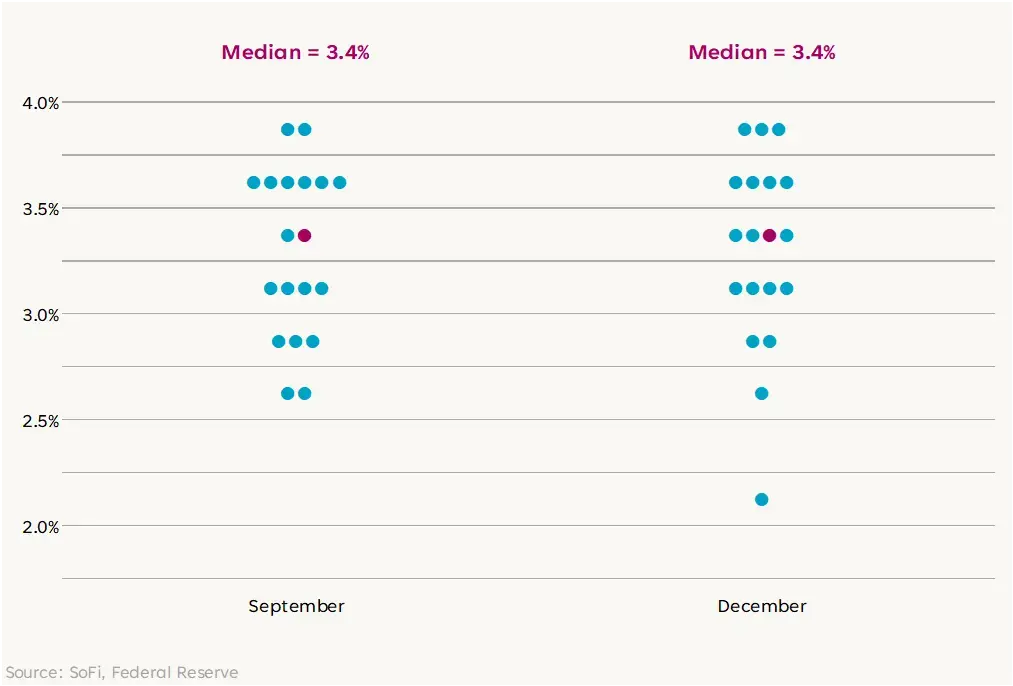

In a typical year, the week following the final Federal Reserve meeting of the year would mark the beginning of the holiday drift. Trading volumes would start drying up, news flow would slow to a trickle, and investors would essentially pack it in for the year.

This week, like so much of 2025, won’t be typical, though. Investors are still playing a game of catch-up with economic data, and the government will release jobs numbers and key inflation metrics for November.

Plus, now that the Fed meeting is behind us, the communications blackout period is over and Fed officials are free to publicly speak about monetary policy and their economic outlooks. We expect a meaningful amount of discussion given the range of views underlying the Fed’s latest decision to lower its benchmark interest rate. (It was a 9-3 vote, and committee members disagreed about where rates could go in 2026).

The temptation might be to tune out and look toward the holidays, but the market has a few more hurdles to clear. Between the flood of delayed data and the slate of speeches from Fed officials, this week promises to be an eventful one.

• December Empire State Manufacturing Activity: The New York Fed’s survey of manufacturing executives in the region on business conditions and their outlook.

• December NAHB Housing Market Index: This index tracks how homebuilders feel about the current and future state of the single-family housing market.

• Fedspeak: Fed Governor Stephen Miran will participate in a moderated conversation with former Fed Vice Chair Richard Clarida at Columbia University’s Institute of Global Politics. New York Fed President John Williams will deliver keynote remarks at a New Jersey Bankers Association event.

• November Employment Situation Summary: This monthly blockbuster release from the Labor Department gives a comprehensive look at employment, wages, and hours worked in the previous month.

• October Retail Sales: This measures spending at retail stores and is a key indicator of consumer demand.

• December New York Services Activity: The New York Fed’s survey of manufacturing executives in the region on business conditions and their outlook.

• December S&P Global US PMIs: These indexes track how purchasing managers across different industries feel about the business environment.

• Earnings: Lennar (LEN)

• Weekly Mortgage Applications: Mortgage activity gives insight on demand conditions in the housing market.

• Fedspeak: Williams will deliver opening remarks at the regional Fed’s FX Market Structure conference. Atlanta Fed President Raphael Bostic will participate in a moderated discussion at the Gwinnett County Chamber of Commerce.

• Earnings: General Mills (GIS), Jabil (JBL), Micron Technology (MU)

• November Consumer Price Index: The CPI is one of the most popular indicators for tracking consumer price trends and is a marquee release for market watchers.

• December Philadelphia Fed Manufacturing Activity: The Philadelphia Fed’s survey of manufacturing executives in the region on business conditions and their outlook.

• December Kansas City Fed Manufacturing Activity: The Kansas City Fed’s survey of manufacturing executives in the region on business conditions and their outlook.

• November Existing Home Sales: Most home transactions in any given month tend to come from the existing market, and as a result set the tone for the broader housing market.

• December University of Michigan Consumer Sentiment: How consumers feel about economic conditions affect their spending habits. This survey places a particular focus on inflation and its trajectory.

• December Kansas City Fed Non-Manufacturing Activity: The Kansas City Fed’s survey of services executives in the region on business conditions and their outlook.

• Earnings: Conagra Brands (CAG), Lamb Weston (LW), Paychex (PAYX)

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

SoFi isn't recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Read more

By SoFi Editors | Updated December 2, 2025

Before deciding to refinance your home loan, you must understand the potential benefits and the costs. Use our Massachusetts mortgage refinance calculator to estimate your new monthly payment, total interest paid, and the break-even point — which determines when your savings will surpass the initial costs. Review this guide to better understand if refinancing makes sense for you.

Key Points

• Our Massachusetts refinance calculator helps estimate monthly payments, total interest costs, and the break-even point, all key elements to making an informed refinancing decision.

• A small reduction in your interest rate — even a quarter percentage point — can lead to significant savings over the life of the loan, making refinancing a potentially advantageous move.

• Extending the loan term can lower monthly payments, but will likely increase total interest paid.

• Refinancing costs, like origination, appraisal, and attorney fees, can range from 2% to 5% of the loan amount.

• Remaining loan balance: The remaining loan balance is what you owe on your existing mortgage. This affects how soon you can refinance a mortgage. In general, you need to have at least 20% equity in your home.

• Current/New interest rate: Interest is the percentage of the total loan amount that the lender charges. The difference between your current and new interest rates will determine potential savings from refinancing.

• Remaining/New loan term: The remaining loan term represents the amount of time over which you are expected to repay your mortgage after completing the refinancing process. A shorter term can save you a significant amount of money in interest payments over the life of the loan, but will also lead to an increase in your monthly payments.

• Points: Points, or discount points, are optional upfront fees you pay a lender to lower your interest rate. Each point costs 1% of the total loan amount and reduces the interest rate by 0.25%.

• Other costs and fees: Other costs associated with refinancing include origination, appraisal, and attorney fees. These expenses typically range from 2% to 5% of the new loan amount.

• Monthly payment: Your monthly mortgage payment typically includes both principal and interest. A refinance mortgage calculator can help you compare your current monthly payment with the estimated payment after refinancing to potentially secure better terms. Lower monthly payments alone don’t indicate whether a mortgage refinance will save you money over the long term.

• Total interest: Total interest is the cost you pay — excluding the principal — to the lender over the duration of the loan. The home refi calculator lets you compare the total interest you will pay on your current and proposed loans, helping you estimate potential savings.

The Massachusetts mortgage refinance calculator helps you assess the financial impact of mortgage refinancing. Here’s how to use the calculator effectively:

Enter your remaining loan balance, which is the principal amount you owe on your current home loan.

Input your current interest rate. This helps estimate your total interest costs, which can be compared to potential new rates and terms. Your interest rate depends on market conditions, your credit history, and the type of mortgage loan you choose.

Estimate what your new interest rate would be by comparing offers from different lenders or checking online for current mortgage rates. A lower rate can reduce your monthly payments and total interest paid.

Select the number of years left on your current mortgage. This allows the calculator to estimate how much you’re likely to pay in interest without refinancing.

Choose a new loan term, anywhere from 10 to 30 years. A shorter term can save on interest, while a longer term can lower monthly payments.

Enter discount points you intend to purchase. Each point costs 1% of the loan amount and reduces the interest rate by 0.25%. Using the mortgage refinance calculator can help you determine whether purchasing points is beneficial to your financial situation.

Estimate other costs and fees, such as origination, home appraisal, credit report, and attorney fees, which can range from 2% to 5% of the loan amount.

Your break-even point is when the savings from refinancing will cover the initial costs. The calculator shows you this figure, which helps you assess whether refinancing is worth pursuing.

Recommended: How to Refinance a Mortgage

Using our Massachusetts refinance calculator can help you figure out whether refinancing is possible and beneficial at this time. This tool provides insight into potential savings, allowing you to see if refinancing could free up money to put toward your other financial goals. Even a small interest rate change — such as a quarter percentage point — could result in significant savings, especially for larger home loans.

The calculator can also help you consider the purpose of your refinance, whether it’s to lower your interest rate, switch to a different type of mortgage loan (such as a fixed-rate loan), or access home equity with a cash-out refinance.

You can calculate your break-even point by subtracting your estimated monthly payment after a refinance from your current mortgage payment. Now divide the total closing costs by the amount you are saving each month. This figure helps you determine whether the savings from refinancing outweighs the initial costs within a reasonable time frame.

Let’s say refinancing saves you $100 each month and the total closing costs amount to $5,000, then it would take 50 months to break even. This is the amount of time needed for you to cover those upfront costs and start seeing actual savings. If you plan to sell before reaching this break-even point, then refinancing might not be beneficial for you right now. The calculator will compute your break-even point for you.

Recommended: How Soon Can You Refinance a Mortgage?

Compare current home interest rates by state and find a mortgage rate that suits your financial goals.

Select a state to view current rates:

You should have a clear understanding of all the potential costs and fees before refinancing. Refinancing a home loan in Massachusetts can cost anywhere between 2% to 5% of the new loan amount. There are a variety of fixed costs such as loan application fees (up to $500), credit report fees ($25-$75), home appraisal fees ($600-$2,000), recording fees ($25-$250), and don’t forget attorney fees ($500-$1,000+). Take into account percentage-based costs too, such as loan origination fees (0.5%-1% of the purchase price) and title search and insurance (0.5%-1% of the purchase price).

Another avenue some people consider is a no-closing-cost refinance, which allows borrowers to roll the closing costs into the mortgage in exchange for a higher interest rate. This move may allow you to keep cash on hand to use for other purposes, however it will increase the principal and total interest paid so you’d have to consider whether it’s worth doing.

Recommended: How and When to Refinance a Jumbo Loan

Reducing your monthly mortgage payment before starting the refinancing process can help lower your mortgage refinance payment. Here are some tips:

• Assess your coverage periodically and see if you can increase your deductible, bundle your home and auto policies from the same insurer, or look into whether a home upgrade (like a better security system) might qualify you for a lower rate.

• Look into extending the term of your loan, which could reduce monthly payments (this could increase your total interest paid too, however).

• Get a loan modification from your lender. This changes the terms of a loan to make monthly payments more affordable.

• Appeal your property tax assessment to potentially reduce your tax bill.

• Consider recasting your mortgage. Your lender will re-amortize the mortgage but retain the interest rate and term. The new, smaller balance equates to lower monthly payments.

A home loan refinance is a major financial decision that requires a full grasp of both the costs and the benefits. Our Massachusetts mortgage refinance calculator is designed to provide you with a clear estimate of your monthly and long-term savings. By calculating your break-even point, you can get clarity on whether refinancing is the right move for your budget.

SoFi can help you save money when you refinance your mortgage. Plus, we make sure the process is as stress-free and transparent as possible. SoFi offers competitive fixed rates on a traditional mortgage refinance or cash-out refinance.

A mortgage refinance could be a game changer for your finances.

There is no one best month, mainly because the best time to refinance can vary based on prevailing mortgage rates and your financial goals. Historically, rates tend to be lower during the fall and winter months. Monitor and track current rates and ensure you’re financially stable before applying.

You aren’t required to put down 20% to refinance. However, having at least 20% equity in your home can help you avoid private mortgage insurance (PMI).

The best bank for refinancing depends on your specific financial needs and the rates and terms it offers. Compare offers from different lenders to find the institution that provides the most competitive interest rates, favorable repayment terms, and best customer service for your needs.

Closing costs in Massachusetts range from 2% to 5% of the new loan amount. Costs may include application fees, credit report fees, appraisal fees, and title insurance. To minimize expenses, shop around and compare rates.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOHL-Q425-085

By SoFi Editors | Updated December 2, 2025

When you take the step to refinance your mortgage, it’s important to fully understand both the potential benefits and possible costs involved before making any decisions about your home loan. A Kentucky mortgage refi calculator can be a great resource during this process. The tool helps provide estimates for your monthly payments, shows you the total interest you might pay over the life of the loan, and calculates the break-even point, an important figure that lets you know when the savings from refinancing will outweigh the initial costs.

Key Points

• The refinance calculator helps estimate monthly payments, total interest costs, and the break-even point, all key elements to making an informed refinancing decision.

• Even a small reduction in your interest rate can lead to substantial savings over the life of the loan, making refinancing a potentially advantageous move.

• Extending the term of your loan can lower monthly payments but increase total interest paid. Shortening the term can do the opposite, so consider your financial goals carefully.

• Factor in refinancing costs, like origination, appraisal, and attorney fees, which can range from 2% to 5% of the loan amount.

• Remaining loan balance: The remaining loan balance is what you owe on your existing mortgage. This affects how soon you can refinance a mortgage, as you usually need to have at least 20% equity in your home.

• Current/New interest rate: Interest is the percentage of the total loan amount that the lender charges you for the privilege of borrowing. The difference between your current interest rate and a potential new rate, even a small amount, can significantly impact both your monthly payments and your overall savings over the duration of the loan.

• Remaining/New loan term: The remaining loan term represents the duration you are expected to repay your mortgage after completing the refinancing process. A shorter term can save you a significant amount of money in interest payments over the life of the loan, but will also lead to an increase in your monthly payments.

• Points: Mortgage points, also known as discount points, allow you to prepay a portion of the interest due on a home loan at closing. Each point typically costs 1% of the total loan amount and can reduce your interest rate by 0.25%.

• Other costs and fees: Refinancing your mortgage comes with various costs and fees, including those for the lender, credit report, home appraisal, and attorney. Mortgage refinancing costs typically range from 2% to 5% of the total loan amount being refinanced.

• Monthly payment: Your monthly mortgage payment typically covers the principal and interest. A refi mortgage calculator can help you compare your current monthly payment with the estimated payment after refinancing to potentially secure better terms.

• Total interest: Total interest represents the cost you will pay to the lender over the life of the loan. Compare the total interest paid before refinance with the projected total interest on a mortgage refinance to determine your potential savings.

Here’s how to use the Kentucky mortgage refinance calculator effectively.

Enter your remaining loan balance. This figure represents the principal amount you owe on your current home loan.

Input your current interest rate. This helps estimate your current monthly payment and total interest costs, which can be compared with potential new rates and terms. Your interest rate depends on market conditions, your credit history, and the type of mortgage loan you choose.

Estimate your new interest rate based on current mortgage rates offered by lenders. Enter this rate into the refinance calculator to see how it could affect your monthly payments and total interest.

Enter the number of years that remain on your current mortgage. This estimates the total interest you’d pay if you kept your current mortgage.

Choose a new loan term that aligns with your financial goals. A longer term can lower monthly payments, while a shorter term can reduce total interest paid over the life of the loan.

Select the number of discount points, if any, you plan to purchase. Points can lower your interest rate, but they come with an upfront cost.

Input the amount of other potential costs and fees, such as origination, credit report, home appraisal, and attorney fees. These costs can range from 2% to 5% of the loan amount.

The calculator divides the total closing costs by the amount of your monthly savings to determine your break-even point. This figure helps you assess whether refinancing is worth pursuing. If you plan to stay in your home longer than this point, refinancing can be beneficial.

Recommended: How to Refinance a Mortgage

You will see that using our Kentucky mortgage refinance payment calculator has many benefits. It can help you evaluate whether refinancing is a viable option to lower your monthly payment or interest rate. The tool provides insight into potential savings, allowing you to see if refinancing could free up money for other financial goals. Even a small reduction in your interest rate, such as a quarter percentage point, can result in significant savings, especially for larger home loans.

Lastly, the refi calculator can help you consider the purpose of your refinance: whether it’s to lower your interest rate, switch to a different type of mortgage loan (such as a fixed-rate loan), or access home equity with a cash-out refinance.

The break-even point represents the amount of time required to recoup all closing costs through the resulting monthly savings. Having a good understanding of the figure helps you decide whether a mortgage refinance is right for you.

The refi mortgage calculator shows your break-even point — by subtracting your new estimated monthly payment from your current mortgage payment, then dividing the closing costs by the monthly savings.

Let’s say refinancing saves you $100 each month, and the total closing costs amount to $2,500. It would take 25 months to cover those upfront costs and begin seeing actual savings. If you plan to sell your home before reaching this point, refinancing might not be the best option.

Recommended: How Soon Can You Refinance a Mortgage?

Compare current home interest rates by state and find a mortgage rate that suits your financial goals.

Select a state to view current rates:

Refinancing a home loan in Kentucky can cost anywhere between 2% to 5% of the new loan amount. There are a variety of fixed costs such as loan application fees (up to $500), credit report fees ($25-$75), home appraisal fees ($600-$2,000), recording fees ($25-$250), and don’t forget attorney fees ($500-$1,000+). Take into account percentage-based costs too, such as loan origination fees (0.5%-1% of the purchase price) and title search and insurance (0.5%-1% of the purchase price).

Another avenue some people consider is a no-closing-cost refinance, which allows borrowers to roll the closing costs into the mortgage in exchange for a higher interest rate. This move may allow you to keep cash on hand to use for other purposes, however it will increase the principal and total interest paid so you’d have to consider whether it’s worth doing.

Recommended: How and When to Refinance a Jumbo Loan

Here are strategies to help you reduce your mortgage refinance payment:

• Work on improving your credit score to secure a lower interest rate.

• Shop around with different lenders and negotiate to get competitive rates and terms.

• Look into extending the term of your loan to reduce monthly payments (this will likely increase your total interest paid).

• Homeowners insurance premiums are often included in mortgage payments, so shop for a lower homeowners insurance rate by increasing your deductible or bundling policies.

Refinancing your home loan can be a strategic financial move, but it’s important to assess the costs before making a decision. Use our Kentucky mortgage refinance calculator to help you estimate potential savings, both monthly and over the life of the loan, and determine whether refinancing aligns with your long-term financial goals.

SoFi can help you save money when you refinance your mortgage. Plus, we make sure the process is as stress-free and transparent as possible. SoFi offers competitive fixed rates on a traditional mortgage refinance or cash-out refinance.

A mortgage refinance could be a game changer for your finances.

Refinancing a $300,000 home loan comes with costs that can range from 2% to 5% of the loan amount, translating to approximately $6,000 to $15,000. Common fixed costs include loan application, credit report, and attorney fees. A mortgage refinance calculator can help you estimate your break-even point and assess the financial viability of refinancing.

A credit score of at least 620 is typically required for conventional loans, and a higher score, such as 700 or above, can help you secure more competitive interest rates and terms. Monitor your credit report, and see what you can do to improve it.

Because refinancing triggers a hard credit pull, it can have a temporary impact on your credit score. The impact is usually temporary, and if you manage the new loan responsibly making on-time payments, your credit score can recover.

To help you determine if it’s not worth refinancing, calculate your break-even point. This is the number of months required for the cumulative savings from a lower interest rate to outweigh all associated refinancing costs. For example, if it will take 50 months to recoup refinancing costs, and you plan to move within 30 months, refinancing may not offer financial benefits.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOHL-Q425-081

Stay up to date on the latest business news and stock market happenings.