If so, you are in the right place! Get started by entering your personal confirmation number below.

Received an offer from us?

If so, you are in the right place! Get started by entering your personal confirmation number below.

Leaving SoFi Website

You are now leaving the SoFi website and entering a third-party website. SoFi has no control over the content, products or services offered nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. SoFi does not guarantee or endorse the products, information or recommendations provided in any third party website.

By Mario Ismailanji |

|

Comments Off on Week Ahead on Wall Street: Economic Menu

A fresh serving of economic data is on the menu for investors this week, offering insights into the health and direction of the economy that have the potential to influence sentiment and investment decisions. While several key releases are scheduled, the main course is sure to be the Friday jobs report.

Before we get to that pivotal report on Friday, however, other important indicators will provide an early taste of economic conditions. The Job Openings and Labor Turnover Survey (JOLTS) release will give us a nuanced look at labor demand, while the ISM Manufacturing and Services Purchasing Managers’ Indexes (PMIs) will offer a timely read on the health of these crucial sectors by tracking activity like new orders, price pressure, and employment. Complementing these figures, the Federal Reserve’s Beige Book will provide a qualitative snapshot of economic conditions across the nation, offering on-the-ground perspectives that can highlight emerging trends.

Finally, the week culminates with the highly anticipated jobs report on Friday. This comprehensive report includes key figures such as jobs added, the unemployment rate, and wage growth. The Fed pays close attention to this report when making decisions about monetary policy, and in uncertain times like these, its importance is greater than ever.

Economic and Earnings Calendar

Monday

• May ISM Manufacturing PMI: This index from the Institute for Supply Management tracks how purchasing managers across the manufacturing sector feel about the business environment.

• April Construction Spending: Construction data is a leading indicator of business activity.

• Fedspeak: Dallas Fed President Lorie Logan will participate in a moderated conversation followed by Q&A. Chicago Fed President Austan Goolsbee will participate in Q&A as part of the Quad Cities Business Journal Mid-Year Economic Review. Fed Chair Jerome Powell will give opening remarks at a conference celebrating the 75th Anniversary of the Board of Governors’ International Finance division.

• Earnings: Campbell Soup (CPB)

Tuesday

• April Factory and Durable Goods Orders: These metrics give insight into underlying trends for leading cyclical indicators.

• April Job Openings: A key measure of business demand for labor is the number of job openings, since reducing openings is easier and preferable to layoffs.

• May Wards Total Vehicle Sales: Cars are a big ticket item for consumers, so underlying vehicle sales trends can help shine a light on demand for durable goods.

• Fedspeak: Chicago Fed President Austan Goolsbee will participate in Q&A as part of the Corridor Business Journal Mid-Year Economic Review. Dallas Fed President Lorie Logan will give opening remarks at a Fed Listens event.

• Earnings: CrowdStrike (CRWD), Dollar General (DG), Hewlett Packard Enterprise (HPE)

Wednesday

• May ADP Employment Report: This survey, usually released a day or two before the official government jobs report, offers insight into private sector employment trends.

• May S&P Global US PMIs: These indexes track how purchasing managers across different industries feel about the business environment.

• May ISM Services PMI: This index from the Institute for Supply Management tracks how purchasing managers across different services industries feel about the business environment.

• Fed Beige Book: This report is released eight times per year and tracks the state of the economy based on qualitative information.

• Weekly Mortgage Applications: Mortgage activity gives insight on demand conditions in the housing market.

• Fedspeak: Atlanta Fed President Raphael Bostic and Fed Governor Lisa Cook will moderate a roundtable discussion at a Fed Listens event.

• Earnings: Dollar Tree (DLTR)

Thursday

• May Challenger Job Cuts: The firm Challenger, Gray & Christmas tracks the number of layoff announcements each month by sector.

• April Trade Balance: Trade, made up of exports and imports, is an important driver of economic activity.

• 1Q Productivity and Unit Labor Costs: These measures provide a breakdown of how productive workers were per hour of work and at what cost.

• Weekly Jobless Claims: This high frequency labor market data gives insight into filings for unemployment benefits. Jobless claims have continued to show a labor market that remains strong despite having cooled.

• Fedspeak: Fed Governor Adriana Kugler will speak at the Economic Club of New York. Philadelphia Fed President Patrick Harker will discuss the economic outlook at an event at the regional Fed bank.

• May Employment Situation Summary: This monthly blockbuster release from the Labor Department gives a comprehensive look at employment, wages, and hours worked in the previous month.

• April Consumer Credit: Borrowing activity gives insight into broader economic activity.

Want to see more stories like this? On the Money is SoFi’s flagship newsletter

for all things personal finance.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

SoFi isn't recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Owning a home in Hawaii is a dream shared by many islanders (and would-be islanders). But it can be a struggle for some to make that dream come true.

It’s no secret that buying a home in a place most people consider to be paradise can be expensive. And it’s been that way for decades. According to Redfin, the median sale price of a home in Hawaii was $767,300 in June 2025, down a wee bit (1.8%) year-over-year. East Honolulu experienced a 5.2% increase in sale price, while all other areas saw prices decline.

Coming up with enough money for a down payment and closing costs can be difficult in the best of times. But in Hawaii, where the cost of living in general is higher than on the mainland, inflation can make home buying especially challenging. You can start by looking in one of the more affordable places in Hawaii.

First-time homebuyers may also be able to get financial help through the state, programs affiliated with the state, and in some cities and counties. There also are longstanding federal programs that could improve a buyer’s chances of success.

Who Is Considered a First-Time Homebuyer in Hawaii?

First, a point of clarity as you start your search for a home loan. For most programs offered in Hawaii, applicants are considered first-time homebuyers if they haven’t owned a home for the past three years. The definition jibes with that of the U.S. Department of Housing and Urban Development (HUD).

3 Hawaii Programs for First-Time Homebuyers

In Hawaii, first-time buyers can find programs that offer down payment assistance, help locating an affordable home, and a mortgage credit certificate that can reduce a homeowner’s income taxes.

These programs were established to assist low- to moderate-income buyers. There also may be a limit on how much the purchased home can cost. Here’s a look at what’s available statewide.

1. HHOC Mortgage Down Payment Assistance Loan Program

HHOC Mortgage, a nonprofit affiliate of the Hawaii HomeOwnership Center (HHOC), was created to help low- to moderate-income families obtain financing.

The lender’s DPAL Program offers qualifying first-time buyers a first mortgage with a 3% minimum down payment paired with a deferred second mortgage of up to $125,000 for down payment or closing cost assistance (including rate buydown), subject to the availability of funds.

Qualifications include:

• Home must be a single-family dwelling, condominium, or townhouse

• HHOC mortgage must originate the first mortgage, and will do so at the same time the 15-year down payment assistance loan (second mortgage) is originated

• Must complete in-class or online homebuyer education with a HUD-approved counseling agency

• Must complete one counseling session with Hawaii HomeOwnership Center

To determine your eligibility, you can contact an HHOC Mortgage loan officer at [email protected], or by calling 808-523-9500 (Oahu). If you qualify, DPAL funds will be reserved once you’ve entered into a purchase contract.

The Hawaii Housing Finance and Development Corporation is a government agency that provides affordable housing opportunities to residents of Hawaii. Its Affordable Resale Program offers previously owned condos repurchased by the agency for sale to qualified residents through a public drawing or lottery process.

Qualifications Include:

• Must be a first-time homebuyer who does not own any unit anywhere in the world

• Must be a U.S. citizen or permanent resident alien and a Hawaii resident

• Must reside in the unit through the time of ownership

• Must meet area median income requirements

• Must agree to the agency’s 10-year buyback and shared profit clauses

The mortgage credit certificate program offered by the HHFDC is a different kind of statewide assistance program designed to help low-income homebuyers. Borrowers can use the certificate to claim 20% of their annual mortgage interest, dollar for dollar, as a federal tax credit every year for the life of their loan.

The tax credit is available to homebuyers who meet specific household income and home purchase price limits.

Check out the program brochure to find out more about the benefits and requirements

You can apply for the credit certificate when you take out a home loan through a participating lender . There may be a fee to participate.

Get matched with a local

real estate agent and earn up to

$9,500‡ cash back when you close.

Pair up with a local real estate agent through HomeStory and unlock up to $9,500 cash back at closing.‡ Average cash back received is $1,700.

If you’ve already chosen the island or county you hope to make your home in Hawaii, you also may want to research the local buyer assistance programs available there.

If you can’t find assistance in your chosen location, check back occasionally for new offers. Some first-time homebuyer programs base their opportunities (and deadlines) on the funds they expect to become available. When their money runs out, they may press pause.

Programs that are currently available include:

Kaua’i County Housing Agency Home Buyer Loan Program

The Kaua’i County Housing Agency Home Buyer Loan Program provides low-cost primary and gap mortgages to income-qualified first-time homebuyers on the island of Kaua’i. For information on benefits and requirements, you can check out the program brochure or call 808-241-4444.

City and County of Honolulu Down Payment Loan Program

The City and County of Honolulu’s Department of Community Services administers a down payment assistance program using HOME Investment Partnership Act funds from HUD. The program provides income-qualifying families with a 0% interest second loan to help with their down payment.

This brochure offers information on the program’s benefits, requirements, and how to apply. Or call the Department of Community Services at 808-768-7762.

How to Apply to Hawaii Programs for First-Time Homebuyers

The way to get more information about each program, and apply, is described above. Often an approved lender is the go-to for assistance programs. Before you take steps to apply, make sure you have a copy of your most recent tax return at hand, because you’ll be asked about your household income.

Several federal government programs are designed for people who have low credit scores or limited cash for a down payment. Although most of these programs are available to repeat homeowners, like state programs, they can be especially helpful to people who are buying a first home or who haven’t owned a home in several years.

The mortgages are generally for single-family homes, two- to four-unit properties that will be owner occupied, approved condos, townhomes, planned unit developments, and some manufactured homes.

Federal Housing Administration (FHA) Loans

The FHA, which is part of the U.S. Department of Housing and Urban Development (HUD), insures mortgages for borrowers with lower credit scores. Homebuyers choose from a list of approved lenders that participate in the FHA loan program. Loans have competitive interest rates and require a down payment of 3.5% of the purchase price for borrowers, who typically need FICO® credit scores of 580 or higher. Those with scores as low as 500 must put at least 10% down.

In addition to examining your credit score, lenders will look at your debt-to-income ratio (DTI, your monthly debt payments compared with your monthly gross income). FHA loans allow a DTI ratio of up to 50% in some cases, vs. a typical 57% maximum for a conventional loan.

Gift money for the down payment is allowed from certain donors. A gift letter for the mortgage will be needed to document the source of the funds.

FHA loans always require mortgage insurance: a 1.75% upfront fee and annual premiums for the life of the loan, unless you make a down payment of at least 10%, which allows the removal of mortgage insurance after 11 years. For a $300,000 mortgage balance, upfront MIP would be around $5,250, and monthly MIP, at a rate of 0.55%, would be around $137. You can learn more about these loans, including FHA loans for refinance and rehab of properties, by reading up on FHA requirements, loan limits, and rates.

Freddie Mac Home Possible Mortgages

Very low- and low-income borrowers may make a 3% down payment on a Home Possible® mortgage. These loans allow various sources for down payments, including co-borrowers, family gifts, employer assistance, secondary financing, and sweat equity.

The Home Possible mortgage is for buyers who have a credit score of at least 660.

Once you pay 20% of your loan, the Home Possible mortgage insurance will be canceled, which will lower your mortgage payments.

Fannie Mae HomeReady Mortgages

Fannie Mae HomeReady® Mortgages allow down payments as low as 3% for low-income borrowers. Applicants generally need a credit score of at least 620; pricing may be better for credit scores of 680 and above. Like the Freddie Mac program, HomeReady loans allow flexibility for down payment financing, such as gifts and grants.

For income limits, a comparison to an FHA loan, and other information, go to this Fannie Mae site .

Fannie Mae Standard 97 LTV Loan

The conventional 97 LTV loan is for first-time homebuyers of any income level who have a credit score of at least 620 and meet debt-to-income criteria. The 97% loan-to-value mortgage requires 3% down. Borrowers can get down payment and closing cost assistance from third-party sources.

Department of Veterans Affairs (VA) Loans

Eligible active-duty members of the military, veterans, reservists, and surviving spouses may apply for loans backed by the Department of Veterans Affairs. VA loans, which can be used to buy, build, or improve homes, have lower interest rates than most other mortgages and don’t require a down payment. Most borrowers pay a one-time funding fee that can be rolled into the mortgage.

Another benefit of VA loans is that they do not require private mortgage insurance (PMI) for borrowers who make a down payment of less than 20%. And they have more flexible credit score requirements. In some cases, even those who have previously been in foreclosure or bankruptcy can qualify.

Borrowers applying for a VA loan will need a Certificate of Eligibility from the VA so make sure to review a guide to qualifying for a VA loan as a first step in the process.

Native American Veteran Direct Loans (NADLs)

Eligible Native American veterans and their spouses may use these no-down-payment loans to buy, improve, or build a home on federal trust land. Unlike VA loans listed above, the Department of Veterans Affairs is the mortgage lender on NADLs. The VA requires no mortgage insurance, but it does charge a funding fee.

US Department of Agriculture (USDA) Loans

No down payment is required on these loans to moderate-income borrowers that are guaranteed by the USDA in specified rural areas. Borrowers pay an upfront guarantee fee and an annual fee that serves as mortgage insurance.

The USDA also directly issues loans to low- and very low-income people. For loan basics and income and property eligibility, head to this USDA site .

HUD Good Neighbor Next Door Program

This program helps police officers, firefighters, emergency medical technicians, and teachers qualify for mortgages in the areas they serve. Borrowers can receive 50% off a home in what HUD calls a “revitalization area.” They must live in the home for at least three years. For more information, visit the HUD program page .

First-Time Homebuyer Stats for 2025

Here are some stats on homebuyers and the homebuying process.

• Percentage of buyers nationwide who are first-time buyers: 24%

• Median age of first-time homebuyers nationally: 38

• Median home price in Hawaii: $767,000

• Median rent in Hawaii: $1,93

• 62.4% of Hawaii housing units were owner-occupied

• Average credit score in Hawaii: 732

Additional Financing Tips for First-Time Homebuyers

In addition to federal and state government-sponsored lending programs, there are other financial strategies that may help you become a homeowner. Some examples:

• Traditional IRA withdrawals. The IRS allows qualifying first-time homebuyers a one-time, penalty-free withdrawal of up to $10,000 from their IRA if the money is used to buy, build, or rebuild a home. The IRS considers anyone who has not owned a primary residence in the past two years a first-time homebuyer. You will still owe income tax on the IRA withdrawal. If you’re married and your spouse has an IRA, they may also make a penalty-free withdrawal of $10,000 to purchase a home. The downside, of course, is that large withdrawals may jeopardize your retirement savings.

• Roth IRA withdrawals. Because Roth IRA contributions are made with after-tax money, the IRS allows tax- and penalty-free withdrawals of contributions for any reason as long as you’ve held the account for five years. You may also withdraw up to $10,000 in earnings from your Roth IRA without paying taxes or penalties if you are a qualifying first-time homebuyer and you have had the account for five years. With accounts held for less than five years, homebuyers will pay income tax on earnings withdrawn.

• 401(k) loans. If your employer allows borrowing from the 401(k) plan that it sponsors, you may consider taking a loan against the 401(k) account to help finance your home purchase. With most plans, you can borrow up to 50% of your 401(k) balance, up to $50,000, within a 12-month period, without incurring taxes or penalties. You pay interest on the loan, which is paid into your 401(k) account. You usually have to pay back the loan within five years, but if you’re using the money to buy a house, you may have up to 15 years to repay.

• State and local down payment assistance programs. Usually offered at the regional or county level, these programs provide flexible second mortgages for first-time buyers looking into how to afford a down payment.

• The mortgage credit certificate program. First-time homeowners and those who buy in targeted areas can claim a portion of their mortgage interest as a tax credit, up to $2,000. Any additional interest paid can still be used as an itemized deduction. To qualify for the credit, you must be a first-time homebuyer, live in the home, and meet income and purchase price requirements, which vary by state. If you refinance, the credit disappears, and if you sell the house before nine years, you may have to pay some of the tax credit back. There are fees associated with applying for and receiving the mortgage credit certificate that vary by state. Often the savings from the lifetime of the credit can outweigh these fees.

• Your employer. Your employer may offer access to lower-cost lenders and real estate agents in your area, as well as home buying education courses.

• Your lender. Always ask your lender about any first-time homebuyer grant or down payment assistance programs available from government, nonprofit, and community organizations in your area.

The Takeaway

Being a first-time homebuyer in Hawaii can be especially challenging, but if you can qualify for one of the mortgage and assistance programs, you may be able to reduce costs. Other first-time buyers can look for advantages among the world of mortgages on their own.

Looking for an affordable option for a home mortgage loan? SoFi can help: We offer low down payments (as little as 3% - 5%*) with our competitive and flexible home mortgage loans. Plus, applying is extra convenient: It's online, with access to one-on-one help.

Yes! Good information is key to a successful purchase process for anyone, but especially for newcomers, who can easily be overwhelmed by purchasing a home. First-time homebuyer classes can help. Indeed they are required for many government-sponsored loan programs.

Do first-time homebuyers with bad credit qualify for homeownership assistance?

Often they do. Many government and nonprofit homeowner assistance programs are available to people with low credit scores. And often, interest rates and other loan pricing are competitive with those of loans available to borrowers with higher credit scores. That said, almost any lending program has credit qualifications.

Is there a first-time homebuyer tax credit in Hawaii?

There is not currently a mortgage credit certificate (MCC) program offered through the Hawaii Housing Finance and Development Corporation, although there has been one in the past. However, reissuance applications for existing MCC holders are still being processed through participating lenders. Homebuyers should check with their lender or tax advisor as tax policies change periodically.

Is there a first-time veteran homebuyer assistance program in Hawaii?

HHOC Mortgage offers a special VA loan, paired with a deferred second mortgage if needed, for veterans who meet income guidelines. VA-backed home loans are available nationwide to eligible service members, veterans, and surviving spouses.

What credit score do I need for first-time homebuyer assistance in Hawaii?

Credit score minimums may vary from one program to the next, and some programs use criteria other than credit scores to determine a borrower’s eligibility. You can check with the organization or lender offering first-time homebuyer assistance to get specific financial requirements.

What is the average age of first-time homebuyers?

The median age of first-time buyers was 38 as of late 2024, an all-time high.

Photo credit: iStock/JamesBrey

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

†Veterans, Service members, and members of the National Guard or Reserve may be eligible for a loan guaranteed by the U.S. Department of Veterans Affairs. VA loans are subject to unique terms and conditions established by VA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. VA loans typically require a one-time funding fee except as may be exempted by VA guidelines. The fee may be financed or paid at closing. The amount of the fee depends on the type of loan, the total amount of the loan, and, depending on loan type, prior use of VA eligibility and down payment amount. The VA funding fee is typically non-refundable. SoFi is not affiliated with any government agency.

Checking Your Rates: To check the rates and terms you may qualify for, SoFi conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, we will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

‡Up to $9,500 cash back: HomeStory Rewards is offered by HomeStory Real Estate Services, a licensed real estate broker. HomeStory Real Estate Services is not affiliated with SoFi Bank, N.A. (SoFi). SoFi is not responsible for the program provided by HomeStory Real Estate Services. Obtaining a mortgage from SoFi is optional and not required to participate in the program offered by HomeStory Real Estate Services. The borrower may arrange for financing with any lender. Rebate amount based on home sale price, see table for details.

Qualifying for the reward requires using a real estate agent that participates in HomeStory’s broker to broker agreement to complete the real estate buy and/or sell transaction. You retain the right to negotiate buyer and or seller representation agreements. Upon successful close of the transaction, the Real Estate Agent pays a fee to HomeStory Real Estate Services. All Agents have been independently vetted by HomeStory to meet performance expectations required to participate in the program. If you are currently working with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®. A reward is not available where prohibited by state law, including Alaska, Iowa, Louisiana and Missouri. A reduced agent commission may be available for sellers in lieu of the reward in Mississippi, New Jersey, Oklahoma, and Oregon and should be discussed with the agent upon enrollment. No reward will be available for buyers in Mississippi, Oklahoma, and Oregon. A commission credit may be available for buyers in lieu of the reward in New Jersey and must be discussed with the agent upon enrollment and included in a Buyer Agency Agreement with Rebate Provision. Rewards in Kansas and Tennessee are required to be delivered by gift card.

HomeStory will issue the reward using the payment option you select and will be sent to the client enrolled in the program within 45 days of HomeStory Real Estate Services receipt of settlement statements and any other documentation reasonably required to calculate the applicable reward amount. Real estate agent fees and commissions still apply. Short sale transactions do not qualify for the reward. Depending on state regulations highlighted above, reward amount is based on sale price of the home purchased and/or sold and cannot exceed $9,500 per buy or sell transaction. Employer-sponsored relocations may preclude participation in the reward program offering. SoFi is not responsible for the reward.

SoFi Bank, N.A. (NMLS #696891) does not perform any activity that is or could be construed as unlicensed real estate activity, and SoFi is not licensed as a real estate broker. Agents of SoFi are not authorized to perform real estate activity.

If your property is currently listed with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®.

Reward is valid for 18 months from date of enrollment. After 18 months, you must re-enroll to be eligible for a reward.

SoFi loans subject to credit approval. Offer subject to change or cancellation without notice.

The trademarks, logos and names of other companies, products and services are the property of their respective owners.

By Erik Nilson |

Uncategorized |

Comments Off on Homeowners Insurance Guide

Homeowners Insurance Guide

Homeowners Insurance Resources: A Comprehensive Guide to Homeowners Insurance

Understanding your homeowners insurance needs can be challenging. This resource hub brings together helpful articles on topics like coverage types, common insurance terms, and costs. Whether you’re looking for ways to lower your premium or just want to learn the basics, these resources can help.

Terms to know:

Blanket Insurance

Blanket insurance enables a property owner to cover multiple pieces of property with one policy. For example, a landlord who has many rental units might take out a blanket policy to insure them all.

Flood Insurance

A standard homeowners policy typically offers some coverage for unexpected water damage due to a plumbing malfunction or broken water pipe. But most standard homeowners policies do not cover damage caused by an overflowing body of water, like a creek, bay, or river. That kind of protection usually requires a separate flood insurance policy.

Hazard Insurance

When you hear the term “hazard insurance,” it’s typically referring to the portion of a homeowners policy that kicks in when someone suffers a loss caused by certain hazards or “perils,” such as fire, hail, theft, a falling tree, or a broken pipe.

Homeowners Insurance

A typical homeowners policy covers the physical structure of an insured home and other structures on the property, personal belongings in the home, and additional living expenses if the owner can’t stay in the home after damage.

Mortgage Insurance

Mortgage insurance protects lenders against the possibility that a borrower might fail to make the payments on a home loan.

Title Insurance

When you buy title insurance, the title company searches for any ownership issues that might cause legal problems after you close on the property. It will look for any liens that might remain on the property, for example, or clerical problems that weren’t caught and fixed in the past.

Homeowners Insurance Basics

Homeowners insurance can be confusing, but understanding the basics can help. These articles cover key topics like how to buy homeowners insurance, how much it can cost, and popular terms to give you a solid foundation.

By Erik Nilson |

Uncategorized |

Comments Off on Auto Insurance Guide

Auto Insurance Guide

Auto Insurance Resources: A Comprehensive Guide to Car Insurance

Understanding your auto insurance needs can be challenging. This resource hub brings together helpful articles on topics like coverage types, common insurance terms, and costs. Whether you’re looking for ways to lower your premium or just want to learn the basics, these resources can help.

Terms to know:

Agent

An agent represents an insurance company (or companies) and sells insurance to and performs services for policyholders.

Claim

When an insured person asks their insurance company to cover a loss, it’s called a claim.

Deductible

This is the predetermined amount the policyholder will pay for repairs before insurance coverage kicks in.

Exclusion

Exclusions are things that aren’t covered by an auto insurance policy.

Premium

A premium is the amount a person pays for auto insurance. Premiums may be paid monthly, quarterly, twice a year, or annually.

Total Loss or ‘Totaled’

If a car is severely damaged, the insurer may determine that it is a total loss. That usually means the car is so badly damaged that it either can’t be safely repaired or its market value is less than the price of putting it back together.

Auto Insurance can be confusing, but understanding the basics can help. These articles cover key topics like how to get car insurance, how much insurance you may need, and how it works to give you a solid foundation.

By Mario Ismailanji |

|

Comments Off on Decoding Markets: Grinding Higher

Unbelievable Rally

The stock market rally we’ve seen since April 8 has been astonishing, and while sputtering a bit, it looks to be hanging in there. Fears of a breakdown intensified last week, as the S&P 500 briefly fell below the 78.6% retracement level of 5896. Despite that brief hiccup, the index was able to bounce off of the 200-day moving average and get back above 5900 on May 27.

The fact that support held suggests that while there isn’t enough buying demand at the moment to take stock indices back to their all-time highs, there are enough investors willing to buy the dip to prevent any major drawdowns.

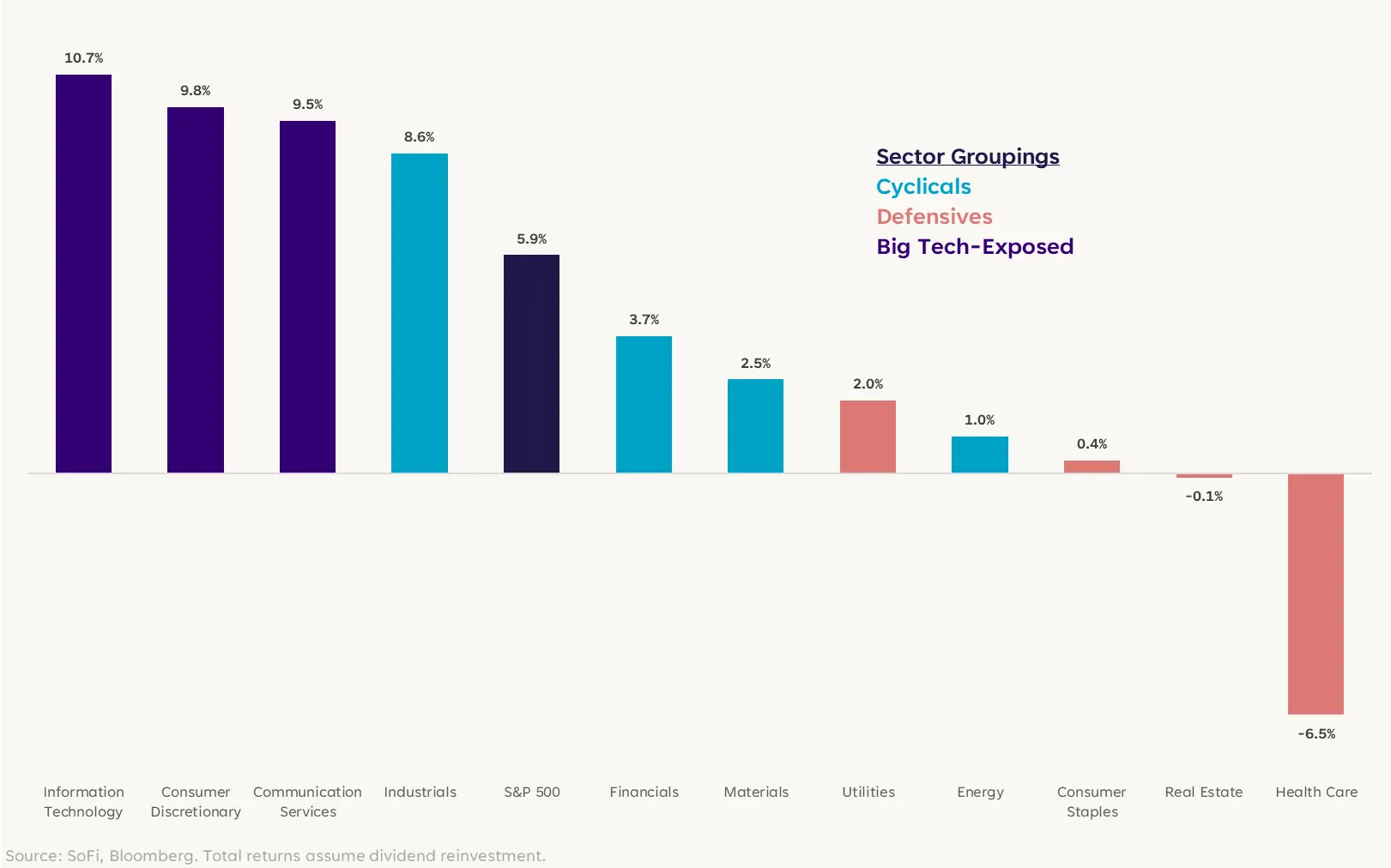

Of course, certain parts of the market have performed differently in this recovery: While the broad market is +5.9% in May thus far, the Information Technology and Consumer Discretionary sectors are +10.7% and +9.8%, respectively. Drilling down further, the automobiles (+24.3%, Consumer Discretionary) and semiconductors (+20.7%, Information Technology) industry groups have been leading the pack. Renewed enthusiasm for artificial intelligence has also been a boon for these high-growth parts of the market.

May S&P 500 Sector Total Returns

Beneath the surface, however, trading volumes have been generally muted. While a rally on low volume isn’t inherently negative, it does suggest a lack of broad conviction in the durability of the rally. In these environments, systematic traders and algorithms can play a bigger role in market direction, especially when specific technical levels are breached or momentum signals are triggered.

For investors who were (or still are) underinvested after the upheaval of the last two months, that could make the “pain trade” still higher, potentially forcing sidelined capital back into the market and adding more fuel, even if conviction isn’t widespread. Still, a foundation built on concentrated leadership and low-volume trading leaves the market susceptible to sharp reversals.

Elephant in the Room

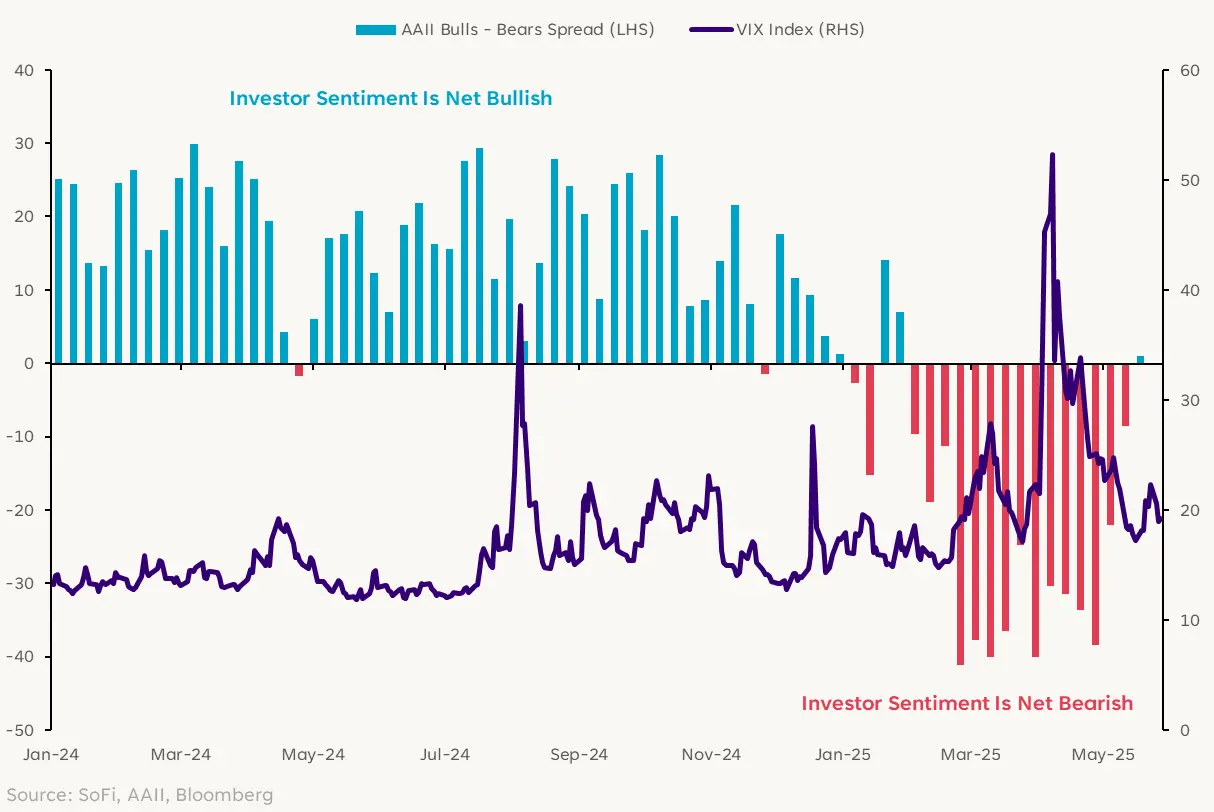

It’s not an exaggeration to say that investor sentiment and stock prices aren’t fully in tune with each other at the moment. Despite the major rally since the April 8 bottom, and the fact that the S&P 500 is now just 3.8% off its highs, investors remain cautious.

For instance, the latest AAII Sentiment Survey showed bullish sentiment at 37.7% versus bearish sentiment at 36.7% — the first time the bulls outnumbered the bears since the end of January. While the bullish investor reading was in-line with its historical average, bearish sentiment remained above average.

The CBOE Volatility Index (VIX), often referred to as the “fear gauge,” tells a similar story. It’s below the panic highs in April when it surged to 52.33, but the current value of 19.23 remains above 2023-24 levels — and well above the low of 11.86 set last year.

Fear Is Receding

For the contrarians, the rapid improvement in sentiment could be a negative signal. Has uncertainty ebbed or are investors too complacent? If negative catalysts were to emerge, the snap back from somewhat positive to pessimistic could be swift.

Known Unknowns

Geopolitical tensions and broader economic uncertainties are casting a long shadow, and it’s not like investors aren’t aware of it.

Tariffs have gotten the bulk of investor attention, and while they’ve been delayed for 90 days, how this eventually plays out is unclear. There’s the persistent threat of re-escalation or new trade disputes (for example, with the European Union, given President Trump’s comments last week about a possible 50% tariff), but market price action suggests investors are pretty confident these issues will be resolved without much economic consequence.

This dynamic effectively makes tariff policy a primary short-term volatility switch for markets. Headlines can trigger immediate and amplified reactions, potentially creating a “headline risk premium.” It also can affect the economy, since businesses and consumers will buy things ahead of tariffs to front-run higher prices as we’ve seen this year:

• Front-running in March to get ahead of April tariffs

• Less buying in April and early May as tariffs on Chinese goods surged

• Recent delay on Chinese tariffs likely leading to another surge of buying activity

It seems probable that there could be another slowdown in spending once the front-running ends, especially if tariffs eventually move higher again.

Beyond tariffs, Russia, Iran and Venezuela loom large. The countries are important players in global oil markets, and discussions have swirled around the possibility of sanctions being lessened or intensified on them. Sanctions relief could lead to more oil supply and lower prices, while tougher sanctions could have the opposite effect.

WTI Oil Prices

Market timing is already exceptionally challenging, but in a highly fluid and event-driven environment where markets can swing dramatically based on a single headline, it’s basically impossible.

Maintaining a well-diversified portfolio that is aligned with your own risk tolerance and long-term financial goals — and resisting the powerful urge to make reactive decisions based on the daily news flow — is crucial. Having that strategic, long-term mindset will help filter out the inevitable market noise and better weather periods of volatility.

Want more insights from SoFi’s Investment Strategy team? The Important Part: Investing With Liz Thomas, a podcast from SoFi, takes listeners through today’s top-of-mind themes in investing and breaks them down into digestible and actionable pieces.

SoFi can’t guarantee future financial performance, and past performance is no indication of future success. This information isn’t financial advice. Investment decisions should be based on specific financial needs, goals and risk appetite.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Mario Ismailanji is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Form ADV 2A is available at www.sofi.com/legal/adv.