If so, you are in the right place! Get started by entering your personal confirmation number below.

Received an offer from us?

If so, you are in the right place! Get started by entering your personal confirmation number below.

Leaving SoFi Website

You are now leaving the SoFi website and entering a third-party website. SoFi has no control over the content, products or services offered nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. SoFi does not guarantee or endorse the products, information or recommendations provided in any third party website.

By Rebecca Moretti |

|

Comments Off on How the Big Budget Bill Could Affect Your Budget

This article appeared in SoFi's On the Money newsletter. Not getting it? Sign up here.

As the national budget bill (aka the “One Big Beautiful Bill”) works its way through Congress, there’s been a lot of debate about the national deficit — and specifically, how the bill’s tax cuts and other provisions could raise it.

But what exactly is a national deficit, and why should we care?

Let’s get into it:

A national budget deficit happens when the federal government spends more money than it takes in with taxes. That’s typical for the U.S., which has only had a budget surplus in four of the last 50 years. But it’s a hot topic right now as the debt-to-GDP ratio nears record levels.

Just as we may lean on a credit card to cover a gap between income and spending, the government also borrows to cover its expenses. The size of the deficit drives how much it must borrow — and pay interest on.

The latest budget bill, which Senate GOP leaders are trying to get passed before July 4th, includes many additions and subtractions to the government’s bottom line.

On the expense side of the equation, the bill would cut spending on programs like Medicaid and SNAP but boost spending in areas like defense and border security. On the income side, it would extend President Trump’s 2017 tax cuts and make at least some tips exempt from taxes, reducing tax revenue.

All told, the Congressional Budget Office estimates that the version that passed in the House last month would raise the national deficit by $2.8 trillion over the next decade. The Trump administration disputes this figure — and notes that the CBO also forecast that new tariffs would reduce the deficit. But again, the topic is hotly debated on the Hill and beyond.

Whenever the government spends more than it has, it borrows money by selling Treasury securities like T-bonds to investors.

But much like carrying a credit card balance, deficit spending can be a vicious cycle, especially when interest rates are high: The U.S. has racked up $36.2 trillion (yes, trillion) in outstanding national debt, and last year spent $1.1 trillion just on interest payments — more than it spent on the military.

So what? While it’s still TBD how (and if) the House and Senate versions of the budget bill will come together, a growing deficit can have financial consequences for Americans and the broader economy:

• Interest rates could go up… even more. As debt concerns grow, investors in Treasury securities tend to demand higher interest rates to compensate for the added risk. (Moody’s recently downgraded the U.S.’s credit rating from the highest Aaa.) That tends to drive up interest rates for Americans, particularly for loans like mortgages, which are heavily influenced by Treasury bond yields.

• It could trigger a recession. High interest rates can depress spending, investment, and wages — especially if the government eventually hikes taxes to offset deficit spending.

• Bond investments could suffer: If Treasury yields go up, prices for existing bonds would likely fall because newly-issued bonds would pay a higher interest rate. That would lower the value of investors’ older bonds.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

SoFi isn't recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

By Mario Ismailanji |

|

Comments Off on Decoding Markets: Geopolitical Fear

Energy Jitters

“The more things change, the more they stay the same” — that famous saying certainly seems to apply to financial markets of late. Nearly halfway through 2025, investors have weathered significant global trade upheaval, major artificial intelligence developments, and military conflicts, yet the S&P 500 is near its all-time highs while the tech-heavy Nasdaq 100 has already surpassed its prior peak.

The most recent instance of this proverb can be seen in the recent conflict between Israel and Iran. The initial escalation of hostilities began two weeks ago, when Israel launched airstrikes against Iran, targeting military and energy infrastructure, and culminated in the U.S. joining in to bomb nuclear facilities.

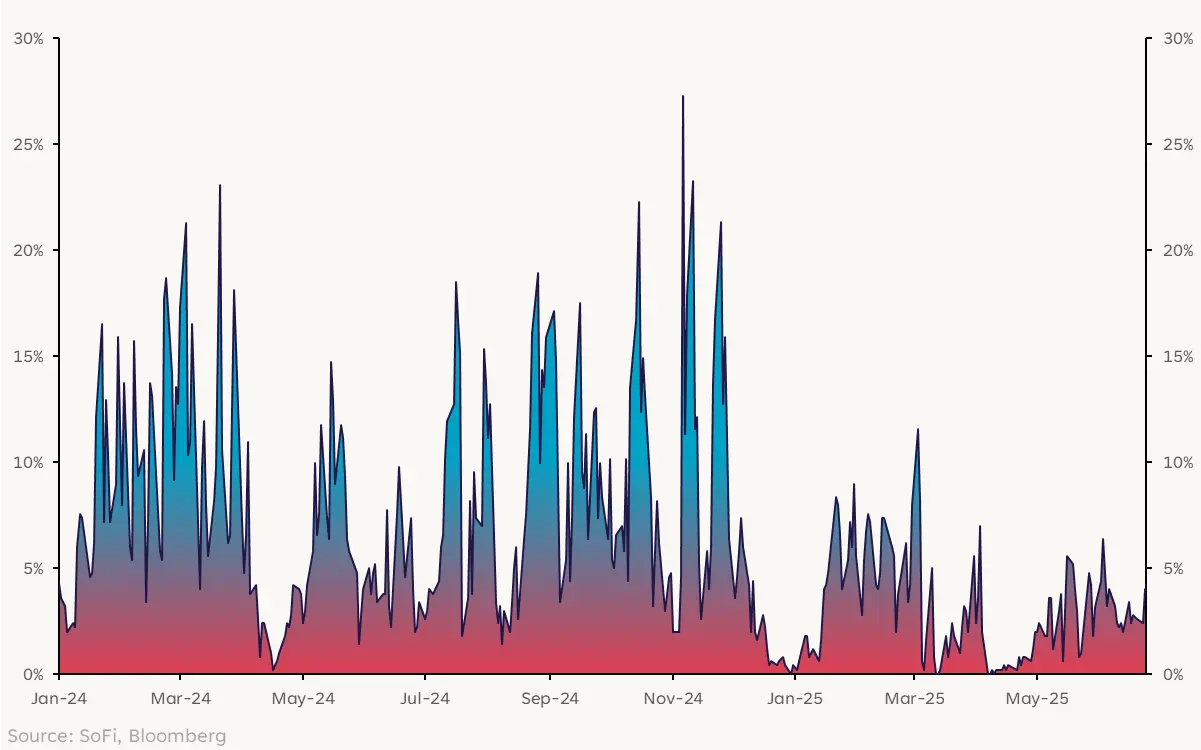

All of this triggered a classic fear-based response in energy markets, with crude oil prices surging over 15% to a five-month high as traders priced in the potential for a severe supply disruption. But almost just as rapidly as prices spiked, they have declined in the days since.

WTI Oil Prices

By targeting a U.S. military base in Qatar while giving advanced notice of its intent to retaliate, Iran signaled a desire to deescalate. Combined with news of a U.S.-brokered ceasefire and the desire for an end to the conflict from President Trump, fears of further escalation have eased.

Though oil prices are back to where they were earlier in the month, things feel more fragile now. The closure of the Strait of Hormuz remains a major risk for energy markets. While investors see that as unlikely — given Iran’s oil-dependent economy and because such a move could alienate its primary customer, China — estimates suggest any disruption could send prices soaring over $100 per barrel.

Being Greedy When Others Are Fearful

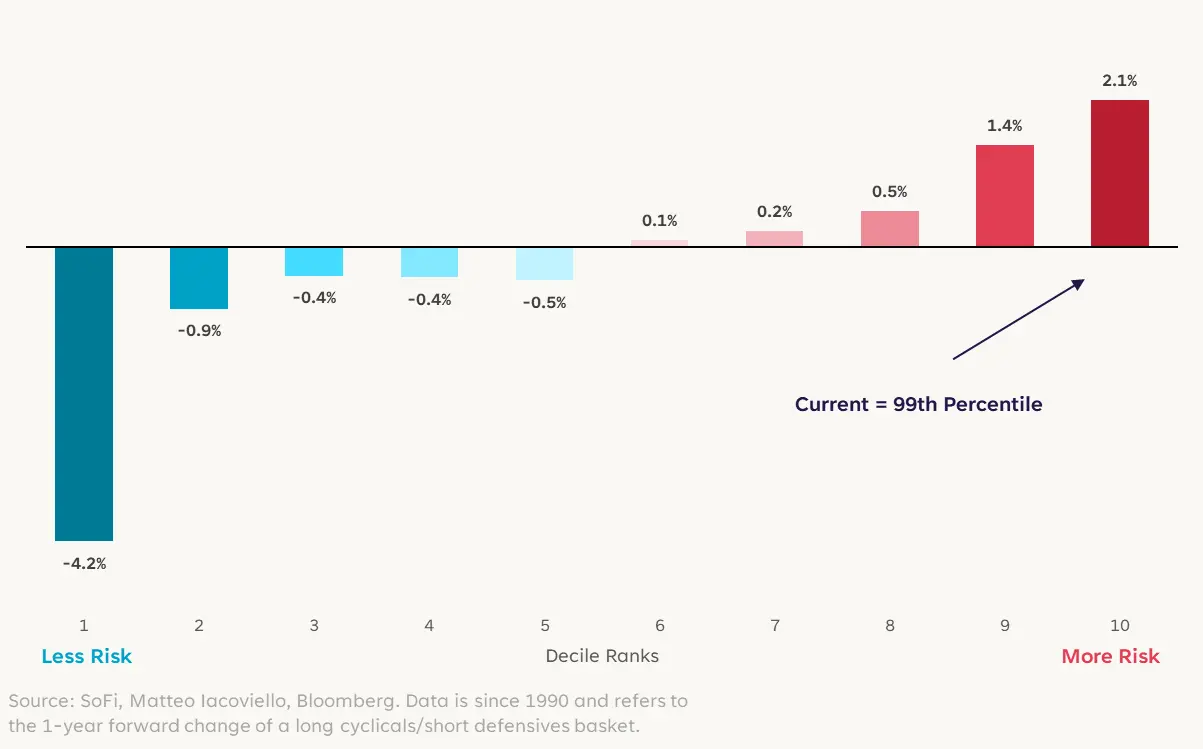

For many investors, the instinctual reaction to rising geopolitical risks is to reduce market exposure, yet history provides a compelling contrarian take. To quantify this, we can use the Geopolitical Risk (GPR) Index, which measures the frequency of news articles mentioning negative geopolitical events.

While overall market returns are varied and don’t have much of a clear pattern, there are notable patterns once we look deeper. In particular, cyclical stocks have historically outperformed defensives after spikes in geopolitical risk.

Relative 1-Year Forward Performance of Cyclicals vs. Defensives

Improves as Geopolitical Risk Increases

The drivers of this phenomenon aren’t exactly the same across history, but the pattern is rooted in market psychology and the economic cycle. The initial reaction to any sort of crisis is often a flight to safety, which can temporarily boost defensive stocks as investors seek stability, and hurt stocks that are more sensitive to economic conditions.

It’s uncommon for geopolitical events to meaningfully affect underlying fundamentals, however, so as the market digests the event and worst-case scenarios fail to materialize, a recovery often takes hold. Historically, this rebound is led by more economically sensitive, and usually oversold, cyclical stocks.

Internal Market Compass

Short-term price action can swing wildly depending on technicals and the news of the day, but fundamentals are what durably drive markets. And the fundamentals are looking a bit iffy right now. How will tariffs affect the economy and inflation? What will the final budget reconciliation bill look like?

For what it’s worth, the Federal Reserve’s recently released projections show lower GDP growth, higher inflation, and higher unemployment through year-end. But given all the macro crosscurrents, things could change quickly. That’s a tough scenario not only for central bank officials — do you prioritize price stability or the labor market? — but for consumers and businesses as well.

Even though the headline stock indices might not show it, the market looks more cautious under the surface. Only 4% of constituent stocks are at 52-week highs. Compare that to last year when the metric was routinely in the 10-20% range, and it becomes clear that investors are still not fully buying the story of a durable bull market.

Percent of S&P 500 Stocks at 52-Week Highs

Where things will go from here is anyone’s guess. We won’t know if the bull market is truly intact for at least another month, when firmer data about tariffs and corporate earnings finally arrives. In the meantime, as another famous saying goes, “anything can happen.”

Want more insights from SoFi’s Investment Strategy team? The Important Part: Investing With Liz Thomas, a podcast from SoFi, takes listeners through today’s top-of-mind themes in investing and breaks them down into digestible and actionable pieces.

SoFi can’t guarantee future financial performance, and past performance is no indication of future success. This information isn’t financial advice. Investment decisions should be based on specific financial needs, goals and risk appetite.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Mario Ismailanji is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Form ADV 2A is available at www.sofi.com/legal/adv.

• The rates for home equity loans in Syracuse are influenced by the prime rate, borrower credit score, and more.

• The higher your credit score and the lower your debt-to-income ratio, the better your rate.

• Home equity loans have fixed interest rates, which give you predictable monthly payments.

• The interest on home equity loans can be tax deductible if used for significant home improvements.

• Closing costs generally fall between 2% and 5% of the loan amount.

Introduction to Home Equity Loan Rates

When you’re thinking about how to get equity out of your home to use for home improvements or other big expenses, the interest rate on a home equity loan is one of the most important factors. Here, we’ll take you through everything you need to know about home equity loan rates in Syracuse, NY. We’ll start by explaining how home equity loan rates are set, then walk you through the different types of home equity loans, detailing their benefits and the risks involved. Armed with this information, you’ll be better equipped to decide whether a home equity loan is right for you and how to get the best rate.

How Do Home Equity Loans Work?

First things first: Make sure you understand what a home equity loan is, exactly. This loan is a second mortgage that uses your home as collateral, and for that reason it will typically have a lower interest rate than an unsecured personal loan. This also means that if you don’t repay a home equity loan, you are at risk of foreclosure.

If approved for a home equity loan, you’ll receive the total loan amount upfront and then immediately begin to repay it, making fixed monthly payments over a set period of time — typically 5 to 30 years. A home equity loan is different from a home equity line of credit (HELOC), though both use your home as collateral. We’ll get into the differences below.

To qualify for a home equity loan, you’ll generally need to have at least 20% equity in your home. (Equity is the difference between your home’s market value and your remaining home loan balance.) Many lenders will allow you to borrow up to 85% of your equity. A home equity loan calculator can help you see what size home equity loan you might be able to qualify for.

The Origin of Home Equity Loan Interest Rates

Home equity loan rates are influenced by a variety of factors, including the state of the economy and your personal financial situation. The Federal Reserve, for example, has a significant impact on the lending market. Lender rates are often tied to the prime rate, which is influenced by the Fed. Your credit score and debt-to-income (DTI) ratio also play a role in determining your interest rate. The amount you borrow and the length of your repayment term can also affect your rate.

How Interest Rates Impact Affordability

Interest rates play a pivotal role in the affordability of your home equity loan. Even a seemingly small variation in rates can add up to substantial savings or costs over the life of your loan. Let’s take a $100,000 home equity loan with a 15-year term as an example. The difference in total interest paid between an 8.50% and a 9.50% rate could be more than $10,000. It’s worth your while to weigh your options — which means getting rates from multiple lenders — and aim for the most cost-effective solution.

Here’s another example, this time for a $75,000 loan repaid over 20 years.

Interest Rate

Monthly Payment

Total Interest Paid

8.00%

$627

$75,559

7.50%

$604

$70,007

7.00%

$581

$64,554

Home Equity Loan Rate Trends

Once you begin to think about borrowing money, you’ll probably find yourself paying more attention to the prime rate. It hit a low of 3.25% in 2020 and a high of 8.50% in 2023. These numbers underscore how advantageous it could be to time your loan application to take advantage of low rates. But it’s not always possible to do so. Maximizing your own personal financial profile is always doable, however, and it can help you obtain the lowest available rate.

Historical Prime Interest Rates

Since 2018, the prime rate has seen its share of ups and downs, ranging from a low of 3.25% in 2020 to a high of 8.50% in 2023. Take a look at the history of the prime rate to get a sense of how high or low it may go this year.

Since 2018, the prime rate has seen its share of ups and downs, ranging from a low of 3.25% in 2020 to a high of 8.50% in 2023. Take a look at the history of the prime rate to get a sense of how high or low it may go this year.

Date

Prime Rate

9/19/2024

8.00%

7/27/2023

8.50%

5/4/2023

8.25%

3/23/2023

8.00%

2/2/2023

7.75%

12/15/2022

7.50%

11/3/2022

7.00%

9/22/2022

6.25%

7/28/2022

5.50%

6/16/2022

4.75%

5/5/2022

4.00%

3/17/2022

3.50%

3/16/2020

3.25%

3/4/2020

4.25%

10/31/2019

4.75%

9/19/2019

5.00%

8/1/2019

5.25%

12/20/2018

5.50%

9/27/2018

5.25%

Source: St. Louis Fed

How to Qualify for the Lowest Rates

To qualify for the best home equity loan rates, you’ll need a good credit score, a manageable DTI ratio, and enough equity in your home. Focusing on these areas before you apply can help you qualify for a home equity loan with the best rates and terms.

Maintain Sufficient Home Equity

To be eligible for a home equity loan, it’s essential to have at least 20% equity in your home. To calculate your equity, deduct your outstanding mortgage balance from your home’s estimated value and then divide the result by the estimated value to arrive at a percentage of equity. For instance, if your mortgage balance is $400,000 and your home’s value is $550,000, then your equity is a solid $150,000 — which is 27%. If you do the math and come up short of 20%, try to hold off on borrowing until you reach that milestone.

Build a Strong Credit Score

When it comes to home equity loans, lenders generally favor credit scores of 680 or higher, with many looking for 700 or more. To bolster your score, make punctual payments, keep credit card balances in check, and steer clear of new debt. Review your credit report for inaccuracies and dispute any errors. By maintaining a solid credit score, you’re setting the stage for a home equity loan with terms that work in your favor and interest rates that are kind to your wallet.

Manage Debt-to-Income Ratio

Your DTI ratio is a critical factor in determining loan eligibility. To learn yours, add all your monthly debts and then divide by your gross monthly income. The DTI requirement for a home equity loan is typically below 50%, and ideally below 36%. A lower DTI ratio indicates a better ability to manage monthly payments. To improve your DTI, consider paying down existing debts, increasing your income, or both.

Obtain Adequate Property Insurance

Property insurance is a must when you borrow against your home because it safeguards the lender’s investment in the event of damage. Make sure your insurance coverage aligns with the lender’s requirements, which may include specific types of coverage and policy limits.

Current home equity loan rates by state.

Compare current home equity loan interest rates by state and find a home equity loan rate that suits your financial goals.

Select a state to view current rates:

Tools & Calculators

By playing around with different scenarios using an online calculator, you get a sense of your borrowing power and what payments might be. Here are three helpful calculators:

Using the free calculators is for informational purposes only, does not constitute an offer to receive a loan, and will not solicit a loan offer. Any payments shown depend on the accuracy of the information provided.

Closing Costs and Fees

When it comes to home equity loan closing costs, you’re looking at paying anywhere from 2% to 5% of the loan amount. Included in the tab are charges for the appraisal, credit report, document preparation, loan origination, notary, title search, and title insurance. You may find no-closing-cost loan options, but they often come with higher rates. Be sure to shop around to compare lenders, as fees can vary.

Tax Deductibility of Home Equity Loan Interest

The interest on your home equity loan could be tax deductible if you’re using it to significantly improve your home. This benefit is currently set to expire in 2025, but there’s talk of extending it. For now, if you’re married and filing jointly, you can deduct interest on loans up to $750,000; for single filers, the loan limit is $375,000. Just remember, you’ll need to itemize your deductions to take advantage of this perk so a talk with a tax advisor may help.

Alternatives to Home Equity Loans

Before you decide whether or not a home equity loan is the right fit, it’s important to understand that there are two other ways to borrow against your home. All three options allow you to tap into the equity you’ve built up, but each has its own features and requirements.

Home Equity Line of Credit (HELOC)

Picture a HELOC as a credit card guaranteed by your home. It’s a flexible way to borrow because during the HELOC’s “draw” period you can borrow in increments and only pay interest on the portion of the credit line that you use. A HELOC interest-only calculator can help you see how much you might owe at any given time based on the portion of the credit line used and your interest rate. After the draw period comes the repayment period. That’s when you’ll pay both interest and principal over a term of up to 30 years. A HELOC repayment calculator is handy at this point. HELOC interest rates are variable, so monthly costs aren’t predictable as they are with a home equity loan. This is one key difference in the HELOC vs. home equity loan equation.

To qualify for a HELOC, you’ll typically need a credit score of 680+ (ideally 700+) and a DTI ratio below 50% (and ideally closer to 36%). HELOCs are a great choice when you’re not sure of the total amount you need or if you want to spread payments over time. You can borrow up to 90% of your home equity with one.

Cash-Out Refinance

A cash-out mortgage refinance is like hitting the reset button on your home loan, but it allows you to borrow extra money as you go. A cash-out refi replaces your existing mortgage with a larger one, pocketing the difference in cash. Most lenders will let you borrow up to 80% of your home’s value. The typical requirements include a credit score of at least 620, a debt-to-income ratio of 43% or less, and you can choose between fixed or variable rates. One big difference between a cash-out refinance vs. a home equity line of credit or a home equity loan: With a refi, you only have one monthly payment to keep track of.

Before committing to a cash-out refinance, you’ll want to have a hard look at current interest rates in Syracuse vs. the rate you already have on your existing home loan to make sure you aren’t sacrificing a sweet rate with a refinance.

The Takeaway

Home equity loans are a powerful financial tool, offering lower interest rates compared to other consumer loans, not to mention the convenience of fixed monthly payments. But they come with the risk of foreclosure if payments are not made. To qualify for the best home equity loan rates, focus on building a strong credit score, a low DTI ratio, and make sure you have adequate property insurance. You’ll be best equipped to obtain a competitive rate with a little preparation.

SoFi now offers home equity loans. Access up to 85%, or $750,000, of your home’s equity. Enjoy lower interest rates than most other types of loans. Cover big purchases, fund home renovations, or consolidate high-interest debt. You can complete an application in minutes.

Unlock your home’s value with a home equity loan from SoFi.

Home equity loans are versatile and can be used for a variety of needs, such as large purchases, home improvements, and debt consolidation. The funds are typically distributed as a lump sum, which can be beneficial if you know how much money you will need and when you will need it. If you aren’t sure, a home equity line of credit might be a better fit.

What’s the monthly payment on a $50,000 home equity loan?

The monthly payment for a $50,000 home equity loan varies based on the loan term and interest rate you obtain. For instance, a 15-year fixed-rate loan at 7.50% would mean a monthly payment of about $464. Opting for a 30-year term at the same rate would lower the monthly payment to around $350. It’s important to note that the total interest paid over the life of the loan is usually higher with a longer term.

What’s the monthly tab for a $100,000 HELOC?

The beauty of a $100,000 HELOC is its flexibility, which also means monthly payments can vary. During the draw period, which is often the first decade, you might only need to pay interest. At an 8.00% interest rate, that could be $667 per month. Once the draw period ends, you’ll start paying both principal and interest. The exact amount will depend on the remaining balance and the interest rate at that time.

What might disqualify you from a home equity loan?

There are a few things that might prevent you from securing a home equity loan. Most lenders look for a credit score of at least 700, although some may be open to lower scores. Your debt-to-income (DTI) ratio should not exceed 50% (and ideally be closer to 36%) to ensure you can comfortably handle the additional financial responsibility. And, you’ll need to have at least 20% equity in your home.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

²SoFi Bank, N.A. NMLS #696891 (Member FDIC), offers loans directly or we may assist you in obtaining a loan from SpringEQ, a state licensed lender, NMLS #1464945. All loan terms, fees, and rates may vary based upon your individual financial and personal circumstances and state.You should consider and discuss with your loan officer whether a Cash Out Refinance, Home Equity Loan or a Home Equity Line of Credit is appropriate. Please note that the SoFi member discount does not apply to Home Equity Loans or Lines of Credit not originated by SoFi Bank. Terms and conditions will apply. Before you apply, please note that not all products are offered in all states, and all loans are subject to eligibility restrictions and limitations, including requirements related to loan applicant’s credit, income, property, and a minimum loan amount. Lowest rates are reserved for the most creditworthy borrowers. Products, rates, benefits, terms, and conditions are subject to change without notice. Learn more at SoFi.com/eligibility-criteria. Information current as of 06/27/24.In the event SoFi serves as broker to Spring EQ for your loan, SoFi will be paid a fee.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Checking Your Rates: To check the rates and terms you may qualify for, SoFi conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, we will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

• Buffalo home equity loan rates are influenced by multiple factors like the prime rate and the individual’s financial profile.

• Even a small difference in interest rates can mean substantial savings or extra costs over the life of your loan.

• Fixed interest rates offer the stability of knowing your monthly payments won’t fluctuate.

• To improve your chances of getting a better home equity loan rate, you can work on your credit score, debt-to-income ratio, and amount of equity in your home.

• Tools and calculators are available online to help you estimate your costs and payments.

Introduction to Home Equity Loan Rates

What is a home equity loan? It’s a way to use the equity you’ve built up in your home to borrow a lump sum of money, usually at a fixed interest rate. And it can be a fantastic financial resource for many homeowners.

In this article, we’ll dive into home equity loan rates in and near Buffalo, NY, explaining how they’re influenced by economic factors and individual financial profiles. You’ll learn how to calculate your home equity, the requirements to qualify for a loan, and the potential risks and benefits of different types of home equity loans, like home equity lines of credit (HELOCs) and cash-out refinances.

Whether you’re planning a home renovation, consolidating debt, or funding a major purchase, this guide will help you make informed decisions about whether a home equity loan is right for you.

Here’s how it works: You take out a new mortgage, pay off your existing home loan, and pocket the difference in cash. You then repay the loan, typically in monthly installments over a period of five to 30 years. Because the loan is secured by your home, the interest rates are generally lower than they are for unsecured loans. Most home equity loans have fixed interest rates, which means your payments stay the same each month throughout the life of your loan.

If you’ve been wondering how to get equity out of your home, home equity loans can be a great option, as long as you have enough equity built up. To qualify for a home equity loan, you’ll typically have to have at least 20% equity in your home.

Where Do Home Equity Loan Interest Rates Originate?

The home equity loan interest rates you’re offered have likely been influenced by a mix of economic and personal factors. The Federal Reserve’s policies, including changes to the federal funds rate, have a big impact on lending. Lenders base their rates on the prime rate, which in June 2025 is 7.50%.

A borrower’s credit score and debt-to-income ratio are also important in determining the rate they’ll be offered. The amount of the loan and the repayment term are factors too; generally, longer repayment terms and larger loan amounts mean higher rates because of the increased risk to the lender.

Understanding these factors can help you anticipate rate changes and make informed decisions about the home equity loan rates you’re likely to be offered.

How Interest Rates Impact Affordability

Your interest rate plays a major role in the affordability of your home equity loan. Even a seemingly small rate variation can have a big impact on your wallet over time.

Let’s break it down by looking at the chart below, which shows a $75,000 home equity loan with a 20-year repayment term.

At 8.00% interest, your monthly payment is $627, and you pay $75,559 in total interest over the entire term of the loan. But if your rate is a percentage point lower, at 7.00%, your monthly payment is $581 and your total interest drops to $64,554. That’s $11,005 in extra interest that could be in your pocket with the lower rate.

Interest Rate

Monthly Payment

Total Interest Paid

8.00%

$627

$75,559

7.50%

$604

$70,007

7.00%

$581

$64,554

Fixed vs Adjustable Interest Rates

Unlike HELOCs, home equity loans usually come with fixed interest rates, which can be helpful when you’re planning your budget. You know exactly what you’ll be paying each month for the entire length of the loan. While fixed rates may often start a bit higher than initial adjustable ones, they can be a solid choice for you if you prefer financial stability.

Adjustable rates, on the other hand, might start at a lower rate, but after the initial period, they can change over time, potentially changing your monthly payments as well.

When you’re deciding between fixed and adjustable rates, think about your financial goals and how comfortable you are with the possibility of variations in your payments.

Home Equity Loan Rate Trends

Predicting the exact movement of interest rates is like trying to guess the weather a year from now. But, by looking at the past, we can see that the prime rate, which is a significant factor in the rates you’ll be offered on a home equity loan, has seen some big swings. As of June 17, 2025, the prime rate is 7.50%. But as you can see in the cart below, it hit a low of 3.25% in 2020 and a high of 8.50% in July, 2023.

Historical Prime Interest Rates

Since 2018, the prime rate has seen its share of ups and downs, ranging from a low of 3.25% in 2020 to a high of 8.50% in 2023. Take a look at the history of the prime rate to get a sense of how high or low it may go this year.

Fluctuations like these in the prime rate have an immediate impact on home equity loan rates in Buffalo. While nobody can predict the future with certainty, understanding past patterns may help you time your application to get a more favorable rate.

Historical Prime Interest Rates

Since 2018, the prime rate has seen its share of ups and downs, ranging from a low of 3.25% in 2020 to a high of 8.50% in 2023. Take a look at the history of the prime rate to get a sense of how high or low it may go this year.

Date

Prime Rate

9/19/2024

8.00%

7/27/2023

8.50%

5/4/2023

8.25%

3/23/2023

8.00%

2/2/2023

7.75%

12/15/2022

7.50%

11/3/2022

7.00%

9/22/2022

6.25%

7/28/2022

5.50%

6/16/2022

4.75%

5/5/2022

4.00%

3/17/2022

3.50%

3/16/2020

3.25%

3/4/2020

4.25%

10/31/2019

4.75%

9/19/2019

5.00%

8/1/2019

5.25%

12/20/2018

5.50%

9/27/2018

5.25%

Source: St. Louis Fed

Taking a longer historical perspective, below, we can see clearly that ups and downs in the prime rate have basically been the norm.

How to Qualify for the Lowest Rates

To qualify for the lowest home equity loan rates, focus on strengthening your credit score, maintaining a healthy debt-to-income ratio, and building enough equity in your home. Lenders may also consider your combined loan-to-value ratio (CLTV), which compares the size of your loan to how much your home is worth. This ratio should ideally be below 80% for the best rates. Even if you haven’t decided yet on a HELOC vs. a home equity loan, the tactics are the same to secure the most competitive interest rates and loan terms.

Maintain Sufficient Home Equity

Here’s the bottom line: You will probably need to have at least 20% equity in your home to be eligible for a home equity loan.

Don’t know how much equity you have? It’s easy to crunch the numbers. Just subtract your mortgage balance from your home’s current value.

For example, let’s say your mortgage balance is $400,000 and your home is now valued at $550,000. That leaves you with $150,000 in equity.

Most lenders allow you to borrow up to 85% or sometimes 90% of your available equity, which means in the example above, you might be able to access up to $135,000. A home equity loan calculator can help you evaluate exactly how large a loan you may be able to access.

Build a Strong Credit Score

To snag the most favorable home equity loan rates, a robust credit score is key. Lenders are often looking for a 680 or higher, but the sweet spot is 700 and up. A higher score demonstrates your history of financial prudence and may therefore open doors to more attractive loan terms.

To work on strengthening your score, make it a habit to pay bills on time, keep credit card balances in check, and steer clear of new debt.

Manage Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is important to qualifying for a home equity loan. Lenders typically favor a DTI below 50%, and 36% or less is ideal.

This ratio is like a financial snapshot, comparing your monthly income to your monthly debt commitments. The lower the ratio, the less debt you’re paying off and the more appealing you are as a borrower.

To enhance your DTI, focus on reducing your debts and, if possible, boosting your income. Not only may this help you secure better home equity loan rates, but it can also fortify your financial foundation.

Obtain Adequate Property Insurance

Property insurance is generally a must-have for securing home equity loans, especially if your home is in an area that tends to experience natural disasters, like floods. This insurance acts as a safety net for both you and your lender, protecting you from loss caused by damage or disasters.

It’s a good idea to make sure your coverage is comprehensive, including protection from floods, fires, and other local risks. Having the right insurance might possibly even sway the terms and rates of your loan in your favor, as lenders tend to look more favorably on borrowers with solid insurance policies.

Current home equity loan rates by state.

Compare current home equity loan interest rates by state and find a home equity loan rate that suits your financial goals.

Select a state to view current rates:

Tools & Calculators

Online tools like calculators can be enormously useful as you try to make the best financial decision for you.

For starters, a mortgage payment calculator can help you estimate what your monthly payments would be, based on the loan’s amount, interest rate, and repayment term. Using one lets you find out easily that, if you were to borrow $100,000 at 9.00% interest for 20 years, you could expect to pay around $900 per month.

Looking at another example, a loan comparison tool can help you compare different lenders and the home equity loan rates they offer so that you can find the best deal for your financial situation.

Using the free calculators is for informational purposes only, does not constitute an offer to receive a loan, and will not solicit a loan offer. Any payments shown depend on the accuracy of the information provided.

Closing Costs and Fees

The closing costs for home equity loans generally fall between 2% and 5% of the loan amount, so it’s important to factor them in to your calculations.

These fees encompass a variety of expenses, such as appraisals, credit reports, document preparation, loan origination fees, notary fees, and the costs associated with title searches and insurance. Some typical prices:

• Appraisal fee: $300-$500

• Credit report fee: $30-$50 or more

• Document preparation: $100-$500 (may also be billed on an hourly basis if an attorney is involved or be included in the origination fee)

• Loan origination fee: 0.5%-1.0% of the loan amount

• Notary fee: $20-$100

• Title insurance fee: 0.5%-1.0% of the loan amount

• Title search fee: $75-$250 or more

While no-closing-cost home equity loans are an option, they often come with higher interest rates.

Tax Deductibility of Home Equity Loan Interest

There’s yet another benefit of home equity loans to consider.

The interest on your home equity loan may be tax deductible if you’re taking out the loan in order to buy, build, or improve your home. For single filers, interest is deductible on the first $375,000 of loan debt. Spouses filing together can deduct the interest on up to $750,000 of debt. Bear in mind, however, that you’ll need to itemize if you want to claim this deduction.

And also note: This tax break currently runs through 2025. It may be extended beyond that, though, so consult your tax advisor to get the most up-to-date information and advice.

Alternatives to Home Equity Loans

Home equity loans are a common choice of homeowners who need a lump sum, but there are other options to explore that also make use of your home equity to get you cash. Home equity lines of credit (HELOCs) and cash-out refinances are two such alternatives.

A HELOC provides a revolving line of credit with a variable interest rate, making it a flexible option for ongoing expenses.

A cash-out refinance is a type of mortgage refinance that replaces your current mortgage with a new one, allowing you to borrow more than you owe and keep the difference.

Each option has its own requirements and potential risks, so it’s worth comparing them with a home equity loan to see what works best for you.

Home Equity Line of Credit (HELOC)

What is a home equity line of credit? A HELOC is somewhat like a credit card because it allows you to borrow up to a set amount and pay interest only on what you actually borrow. You usually have a “draw period” during which you can take money out and pay only the interest for what you borrow. After that comes a repayment period, during which you pay back the principal and interest. Typically, a HELOC’s interest rate is variable, so it may fluctuate with the market. This means your costs could rise if interest rates go up.

To get a HELOC, you typically need a credit score of 680, but 700 is preferable. You’ll also need a debt-to-income (DTI) ratio of less than 50%, but ideally less than 36%. HELOCs can be especially helpful if you have ongoing expenses and can provide access to up to as much as 90% of your home equity.

If you want to figure out how much the monthly payments for a HELOC would cost, you might consider using a HELOC monthly payment calculator.

And if you’d like to calculate how much interest you’d have to pay during the “draw” period of a HELOC, try a HELOC interest-only calculator.

Cash-Out Refinance

A cash-out refinance is a bit like a reset button for your mortgage. You take out a new mortgage, pay off your existing home loan, and pocket the difference in cash. The amount you can receive is based on your home equity: Most lenders permit borrowing up to 80% of your home’s value.

If you’re contemplating the benefits of a cash-out refinance vs. a home equity line of credit, be aware that the requirements for borrowing are generally different. It’s usually easier to qualify for a cash-out refi than for a home equity loan or a HELOC. Cash-out refinances typically require a minimum credit score of 620 and a DTI ratio of 43% or less. They may have either fixed or variable interest rates, with variable rates sometimes offering more equity access.

And, unlike a home equity loan, a cash-out refi results in a single monthly payment, which can make it easier to manage.

The Takeaway

If you’re considering a home equity loan in Buffalo, NY, it’s important to understand the factors that can influence home equity loan rates. Factors like your credit score, debt-to-income ratio, and property insurance can affect the rates you’re offered. Using tools and calculators can help you estimate costs and payments. You may want to consider alternatives like HELOCs and cash-out refinances, which also let you leverage your home equity and can offer different benefits. Fully understanding your options can help you find the best solution for your financial needs.

SoFi now offers home equity loans. Access up to 85%, or $750,000, of your home’s equity. Enjoy lower interest rates than most other types of loans. Cover big purchases, fund home renovations, or consolidate high-interest debt. You can complete an application in minutes.

Unlock your home’s value with a home equity loan from SoFi.

A home equity loan can be useful for many purposes. Common ones are major purchases, home improvements, and consolidating high-interest debt. While these loans are flexible, it’s important to make sure you can afford the monthly payments so that you don’t run the risk of losing your home to foreclosure.

What’s the monthly payment on a $50,000 home equity loan?

It’s not just the total loan amount, but also the interest rate and term of the home equity loan that determine how much your monthly payment will be. For example, if your fixed-rate $50,000 loan has a 6.00% rate and a 15-year term, you pay around $422 each month. If the rate were two percentage points higher, at 8.00%, your monthly payment would be $478. A mortgage payment calculator can help you assess what you’d need to pay for different loans with different terms.

What might disqualify you from getting a home equity loan?

Several factors could prevent you from securing a home equity loan. First, lenders usually want you to have a credit score of at least 680, so a lower one could present an obstacle. A high debt-to-income (DTI) ratio, generally more than 50%, might also be a problem. Having less than 20% equity in your home could be another potential issue. Lenders also look at the stability of your home’s value and the adequacy of your property insurance when they’re considering whether to approve you for a home equity loan.

What are the benefits of a home equity loan?

Home equity loans can provide you with a number of benefits, including a lump sum of cash and payments that typically come with a fixed interest rate, which can ensure that your monthly payments remain predictable. These loans can make sense for large, one-time expenses such as home renovations or high-interest debt consolidation. Additionally, home equity loan rates are generally lower than those of unsecured loans, making them a cost-effective option when you need money. However, it’s important to remember that these loans come with the possibility of foreclosure if you don’t make your payments.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

²SoFi Bank, N.A. NMLS #696891 (Member FDIC), offers loans directly or we may assist you in obtaining a loan from SpringEQ, a state licensed lender, NMLS #1464945. All loan terms, fees, and rates may vary based upon your individual financial and personal circumstances and state.You should consider and discuss with your loan officer whether a Cash Out Refinance, Home Equity Loan or a Home Equity Line of Credit is appropriate. Please note that the SoFi member discount does not apply to Home Equity Loans or Lines of Credit not originated by SoFi Bank. Terms and conditions will apply. Before you apply, please note that not all products are offered in all states, and all loans are subject to eligibility restrictions and limitations, including requirements related to loan applicant’s credit, income, property, and a minimum loan amount. Lowest rates are reserved for the most creditworthy borrowers. Products, rates, benefits, terms, and conditions are subject to change without notice. Learn more at SoFi.com/eligibility-criteria. Information current as of 06/27/24.In the event SoFi serves as broker to Spring EQ for your loan, SoFi will be paid a fee.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Checking Your Rates: To check the rates and terms you may qualify for, SoFi conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, we will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.