If so, you are in the right place! Get started by entering your personal confirmation number below.

Received an offer from us?

If so, you are in the right place! Get started by entering your personal confirmation number below.

Leaving SoFi Website

You are now leaving the SoFi website and entering a third-party website. SoFi has no control over the content, products or services offered nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. SoFi does not guarantee or endorse the products, information or recommendations provided in any third party website.

By Derek Stratton |

Uncategorized |

Comments Off on Routing Number

SoFi Routing Number

Your SoFi routing number, when you need it: 031101334

Need to set up a direct deposit or transfer funds fast? Your SoFi routing number (031101334) makes it easy. We’ll show you where to find it, how it’s different from your account number, and why it matters.

What is a routing number?

A routing number is a nine-digit code that identifies your bank or financial institution in the U.S. banking system. It’s used to route money accurately during transactions like direct deposits, wire transfers, and automatic bill payments. Think of it as your bank’s address. Paired with your checking or savings account number, it ensures your funds end up in the right place.

How to find your SoFi routing and account number.

You can access your SoFi routing and account numbers in a few easy ways:

Online.

Log in to your SoFi account on a desktop browser, go to the Banking section, and select either your Checking or Savings account. Your routing and account numbers appear on both accounts.

In app.

Open the SoFi app, tap on Banking, and then tap the ellipsis icon at the top right. Your routing and account numbers appear at the top of the page.

On a check.

Your routing number is the first nine digits on the bottom left, followed by your account number.

{/* Horizon */}

{/* why choose*/}

What your routing number is used for.

Your SoFi routing number plays a key role in many banking tasks. You’ll need it to do things like:

Set up direct deposit.

Use your routing and account number to have your paycheck, tax refund, or government benefits added straight into your account via direct deposit.

Set up recurring payments and subscriptions.

Use your routing and account numbers to pay bills online or enroll in autopay for subscriptions.

Send and receive wire transfers.

When you’re moving money domestically, routing numbers help ensure wire transfers reach the right destination.

Pay for online products and services.

Some merchants allow direct bank transfers. Your routing number ensures the payment goes through correctly.

Transfer money.

You’ll need your routing number to transfer funds between various bank accounts.

Pay taxes.

Whether you’re receiving a refund or making a payment, the IRS may ask for your routing and account numbers.

{/* Why set up direct deposit */}

Why set up direct deposit with SoFi?

Setting up direct deposit with SoFi is convenient and comes with perks.

Earn up to a $300 bonus with direct deposit.

When you set up eligible direct deposit of $1,000 or more, you can unlock a checking account bonus of $50 or $300.1

Checking account resources and education:

FAQs

What if my employer doesn’t recognize the routing number?

Double-check that you’ve entered your routing number correctly. If issues persist, contact SoFi customer support to confirm your direct deposit details.

Can I use the same routing number for wire transfers?

Yes, SoFi uses the same routing number (031101334) for both ACH and domestic wire transfers.

Is the routing number the same for all SoFi accounts (invest, credit card)?

No, the routing number only applies to SoFi Checking and Savings accounts. Investment and credit card accounts have separate identifiers.

What is the difference between a routing number and an account number?

A routing number identifies your bank, while your account number identifies your individual account. Be sure to keep your routing and account number combo secure to avoid fraudulent activity. Learn more about routing numbers vs. account numbers.

What is an ABA number?

An ABA number is another term for a routing number—a nine-digit code used to identify U.S. financial institutions.

Is it safe to share my routing number?

Yes, routing numbers are safe to share because they are publicly available and specific to your bank. They’re used for deposits and payments, not for withdrawing money from your account.

What is SoFi’s full bank name and address?

SoFi Bank, N.A., 2750 E. Cottonwood Parkway, Suite 300, Cottonwood Heights, UT 84121.

Can my routing number change?

It’s rare, but routing numbers can change if your bank merges or restructures. SoFi will notify you if any changes occur.

{/* Closing CTA */}

Access your SoFi routing number anytime.

Don’t have an account yet? Sign up for a SoFi bank account today for smart banking with big benefits.

Indiana University of Pennsylvania (IUP) is a research-focused university located in, you guessed it, Indiana, Pennsylvania. Its rural campus was founded in 1875 and now spans 374 acres, serving 7,432 undergraduate students, according to US News & World Report.

Total Cost of Attendance

Indiana University of Pennsylvania (IUP) tuition for 2024-25 was $11,380 for in-state students and $16,297 for out-of-state students. The national average for public four-year schools is $11,260 for in-state students and $29,150 for out-of-state students. In the chart below, you’ll learn the full cost of an IUP education.

Costs for 2024-25

Student Type

In-State

Out-of-State

Tuition & Fees

$11,380

$16,297

Books & Supplies

$1,100

$1,100

Room & Board

$13,286

$13,286

Other Expenses

$2,080

$2,080

Total Cost of Attendance

$27,846

$32,763

Financial Aid

At IUP, nearly all students (99%) use some sort of financial aid to pay for school. This includes student loans, scholarships, and grants.

Generally, financial aid is monetary assistance awarded to students based on personal need or merit. Students that qualify for financial aid can use it to pay for college costs like tuition, books, and living expenses.

The federal government is the largest provider of student financial aid. However, aid can also be given by state governments, colleges and universities, private companies, and nonprofits. The different types include:

• Scholarships: These can be awarded by schools and other organizations based on students’ academic excellence, athletic achievement, community involvement, job experience, field of study, and/or financial need.

• Grants: Generally based on financial need, these can come from federal, state, private, and nonprofit organizations.

• Work-study: This federal program provides qualifying students with part-time employment to earn money for expenses while in school.

• Federal student loans: This is money borrowed directly from the U.S. Department of Education. It comes with fixed interest rates that are typically lower than private loans.

Colleges, universities, and state agencies use the Free Application for Federal Student Aid (FAFSA) to determine financial aid eligibility. The FAFSA can be completed online, but note that state, federal, and school deadlines may differ.

You can find other financial aid opportunities on databases such as:

At Indiana University of Pennsylvania, 73% of students secure federal student loans and 17% obtain private loans. The average amount for private student loans is $11,496.

Private loans are funded by private organizations such as banks, online lenders, credit unions, some schools, and state-based or state-affiliated organizations. While Federal student loans have interest rates that are regulated by Congress, private lenders follow a different set of regulations so their qualifications and interest rates can vary widely.

What’s more, private loans have variable or fixed interest rates that may be higher than federal loan interest rates, which are always fixed. Private lenders may (but don’t always) require you to make payments on your loans while you are still in school, compared to federal student loans which you don’t have to start paying back until after you graduate, leave school, or change your enrollment status to less than half-time.

Private loans are funded by private organizations such as banks, online lenders, credit unions, some schools, and state-based or -affiliated organizations. While federal student loans have interest rates that are regulated by Congress, private lenders follow a different set of regulations so their qualifications and interest rates can vary widely.

If you’ve missed the FAFSA deadline or you’re struggling to pay for school during the year, private loans can potentially help you make your tuition payments. Just keep in mind that you will need enough lead time for your student loan to process and for your lender to send money to your school.

For an in-state student to attend Indiana University of Pennsylvania for four years, the cost would be $111,384, based on 2024-25 numbers. The total cost of in-state attendance for four years at a public university in the U.S. averages $115,360 for four years, slightly higher than IUP.

For out-of-state students, the cost would be $131,052 at IUP, significantly lower than the national average of $186,920.

In 2024-25, the cost for IUP tuition and fees, as well as books, was $12,480 for in-state students and $17,397 for out-of-state students.

Graduate Tuition and Fees

Costs for 2024-25

Student Type

In-State

Out-of-State

Tuition

$9,288

$13,932

Fees

$3,384

$4,329

Total

$12,672

$18,261

At Indiana University of Pennsylvania, the average cost of graduate school tuition in 2024-25 was $9,288 for students from Pennsylvania, with an additional $3,384 in fees. For students from another state, the cost was $13,932 for tuition plus $4,329 in fees. There are graduate loans available to help with these costs.

Cost per Credit Hour

Indiana University of Pennsylvania lists its costs per credit. For in-state students, the cost per credit, including fees, is $516. The cost per credit and fees for out-of-state students is $851.

Campus Housing Expenses

Costs for 2022-23

Student Type

On-Campus

Off-Campus

Room & Board

$13,286

$12,832

Other Expenses

$2,080

$2,080

At IUP, most freshmen are required to live on campus. Residential suites include one-, two-, or four-person shared suites, and there are also Living-Learning Communities where students attend classes in a given area of focus as well as live together.

Those who choose to live off-campus can find many options, from studios to shared houses, near campus. This resource can help you find out more about housing at IUP.

Indiana University of Pennsylvania Acceptance Rate

Fall 2023

Number of applications

9,422

Number accepted

8,574

Percentage Accepted

91%

At 91%, the IUP acceptance rate is high. Most students who apply get in.

Admission Requirements

So what does it take to apply at IUP? Here’s what’s required with your application, as well as other documents that you may choose to include.

Required:

• High school transcript

Recommended:

• SAT or ACT scores

• Letter(s) of recommendation

• Personal essay

• Transcripts for college coursework completed in high school

• AP test scores (to receive academic credit at IUP)

You can apply to IUP here . For the fall application season, applications are accepted as of the previous July 1st.

SAT and ACT Scores

Test scores are currently not required with applications. Here are the 25th and 75th percentile SAT and ACT scores at IUP in Fall 2023.

Subject

25th Percentile

75th Percentile

SAT Evidence-Based Reading/Writing

480

600

SAT Math

460

570

ACT Composite

17

24

ACT English

16

24

ACT Math

16

23

Popular Majors at Indiana University of Pennsylvania

IUP offers more than 140 majors. Here are some of the most popular.

1. Nursing

Nursing students at IUP learn how to deliver the best health care while utilizing technology and information that benefits patients. They also learn how to communicate with patients, their families, and medical professionals.

Undergraduate degrees in 2023-24: 115

2. Criminology

Students in this program will study the criminal justice system, policing, juvenile justice and law, white-collar crime, violence and victimology, and environmental crime, among other subjects. Students also have the opportunity to intern in the field.

Undergraduate degrees in 2023-24: 114

3. Sports Kinesiology

Students interested in careers in health, healing, or rehabilitation will study anatomy, exercise physiology, exercise prescription and aging, and more. They will also have the opportunity for hands-on learning in courses like aerobic leadership, as well as the opportunity to intern in the field.

Undergraduate degrees in 2023-24: 78

4. Psychology

The psychology program covers developmental, abnormal, social, and learning and cognition psychology, as well as biopsychology. Students will choose a specialization in either applied psychology or psychological science.

Undergraduate degrees in 2023-24: 69

5. Communications Media

Communications students can opt for a media studies, media production, or media marketing track, and select electives including courses in audio production, photography, global media and communication, women in media, television criticism, public relations, and more.

Undergraduate degrees in 2023-24: 67

6. Biology

At IUP, you can get either a BA or BS in biology. Coursework includes botany, zoology, genetics, ornithology, immunology, limnology (the study of lakes), plant physiology, and more.

Undergraduate degrees in 2023-24: 67

7. Business

IUP offers several undergraduate programs in business, including accounting, business education, finance, human resource management, international business, management, and management information systems.

Undergraduate degrees in 2023-24: 64

8. Marketing

Marketing students have the opportunity to learn about internet marketing, social media marketing, advertising, professional selling, sales management, marketing research, direct marketing, retail management, and services marketing. They also have the opportunity to study abroad at partner business schools.

Students get a strong foundation in the natural sciences, math, and business before gaining real-world experience in labs and through internships.

Undergraduate degrees in 2023-24: 44

10. Finance

After studying accounting principles, fundamentals of finance, business policy, operations management, and statistics (among other subjects), students are well-prepared for careers in finance.

Undergraduate degrees in 2023-24: 38

Graduation Rate

Here is the graduation rate for students who started their studies at IUP in 2017:

• 4 years: 37%

• 6 years: 53%

Post-Graduation Median Earnings

The median salary of graduates of IUP is $51,019 a year, below the national average of $68,516.

Bottom Line

If you’re looking for a smaller, close-knit campus where you can pursue your studies and prepare for life after graduation, Indiana University of Pennsylvania may be a good match. And there are both federal and private student loans that can help with the cost of IUP tuition.

SoFi private student loans offer competitive interest rates for qualifying borrowers, flexible repayment plans, and no origination fees.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loans are subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, the student's at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change. This information is current as of 4/22/2025 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Bank, N.A. and its lending products are not endorsed by or directly affiliated with any college or university unless otherwise disclosed.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

By Mario Ismailanji |

|

Comments Off on Decoding Markets: May Inflation

Downside Surprise

Representing a pillar of the Federal Reserve’s dual mandate, inflation reports have always been something professional investors took note of. However, these releases have taken on greater importance in the post-pandemic period.

At first it was to track what was thought to be a “transitory” increase in inflation as the global economy emerged from Covid lockdowns. But that transitioned to monitoring the impact of stubborn supply problems related to goods, labor, and energy.

We’re in the midst of another transition. The concerns about pandemic-related supply chain distortions have been replaced by concerns about tariffs. Judging the impact of trade policy on the economy has been like a game of whack-a-mole for investors: Will the economy continue growing while prices rise, or are businesses and consumers going to cut back on their spending due to uncertainty?

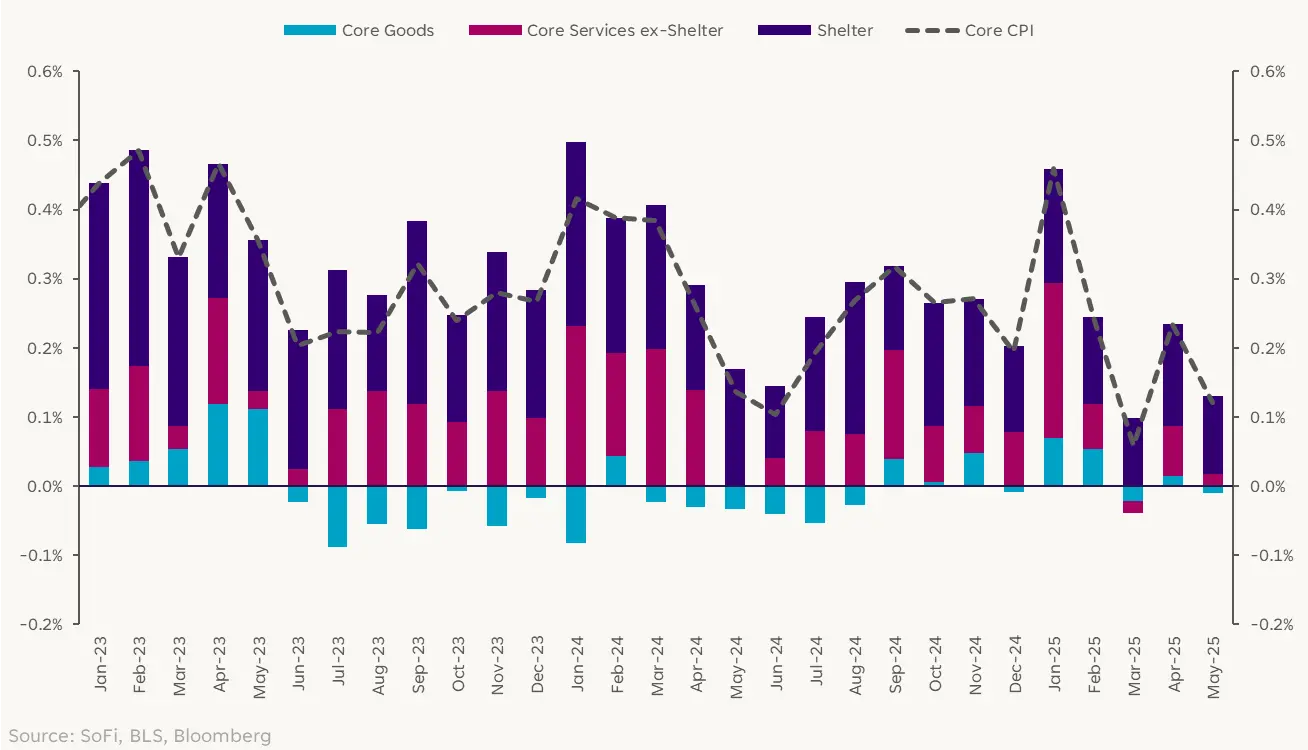

It’s far too early for a definitive answer, but the latest consumer price data suggest no price shock quite yet. May CPI rose 0.1% m/m on both a headline and core (i.e. excluding food and energy) basis.

Core CPI Month-Over-Month

The downside surprise to core inflation was particularly notable, as it was the fourth straight below-consensus print, with this release coming in below all Bloomberg economist estimates. Usually seen as a more stable read into the underlying inflation trend than the headline number, it caught investors off-guard and pushed Treasury yields lower by 5-10 bps across most maturities.

Widespread Disinflation

Because inflation reports often contain so much data, there’s usually something in them for both upside and downside risk viewpoints to hang their hat on. That’s tougher to do in this report, as most components shifted lower with very little in the way of acceleration. Shelter prices rose 0.3%, one of its lowest increases in the last four years, while the prices of energy, cars, and airfares fell 1.0%, 0.3%, and 2.7%, respectively.

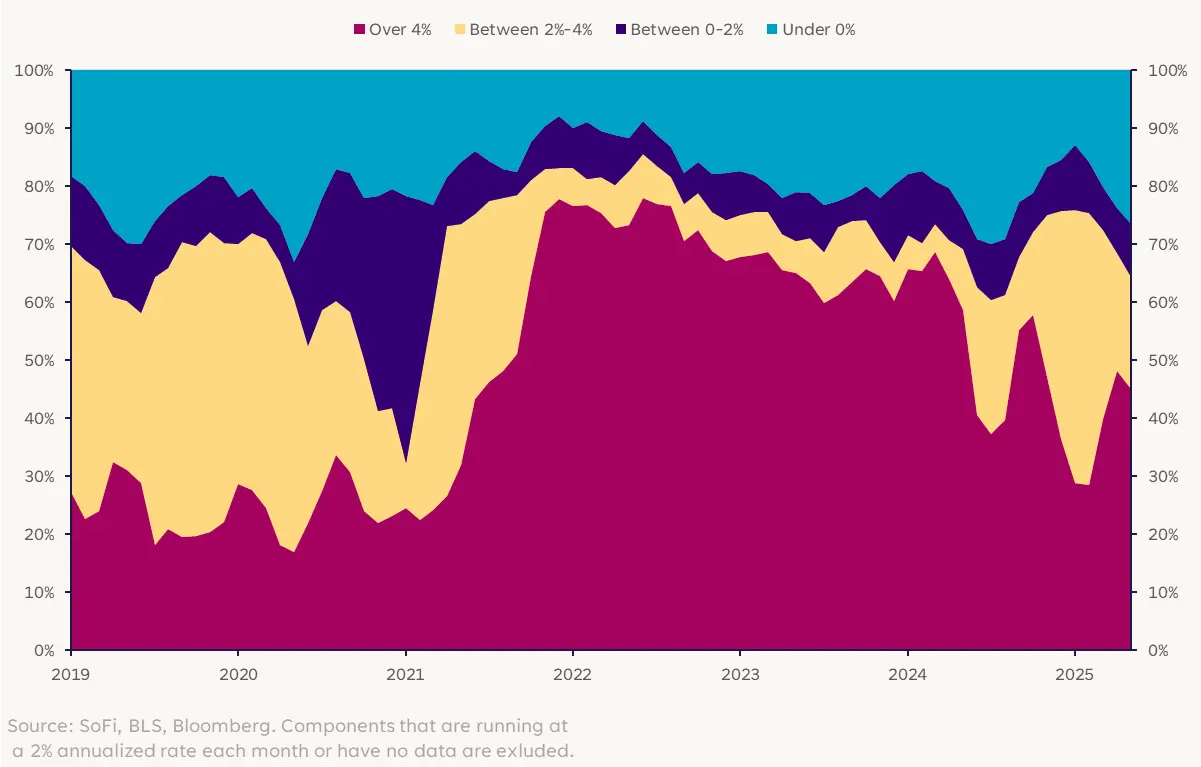

More broadly, putting every component into buckets can help visualize the breadth of inflation in its totality. Here’s what that looks like.

Distribution of CPI Components by M/M Annualized Rates

The major jump in components that were running at an above-4% inflation rate (magenta) a couple of years ago jumps out, but more importantly for investors is the recent increase in the number of components at a below-2% inflation rate (blue and purple).

The slowdown of inflation isn’t being caused by just a few categories. That supports the view that inflation is becoming less and less of a problem.

Now, Later, or Never

Although I said earlier it was too early to have a definitive answer on what impact trade upheaval has been having on the economy, that doesn’t mean we have zero clue.

Broadly speaking, prices are a function of supply and demand. Holding supply constant, more demand usually means higher prices, while less demand usually means lower prices. On the other hand, holding demand constant, more supply means lower prices, and lower supply means higher prices.

Since inflation data has been consistently surprising to the downside, that leaves us with two plausible drivers: Either supply has been better than expected, or demand has been weaker. Even after accounting for over-ordering to get ahead of possible tariffs, it’s hard to imagine that the upheaval of the last few months has improved the overall supply story. That leaves demand deterioration as the most likely driver of lower inflation prints.

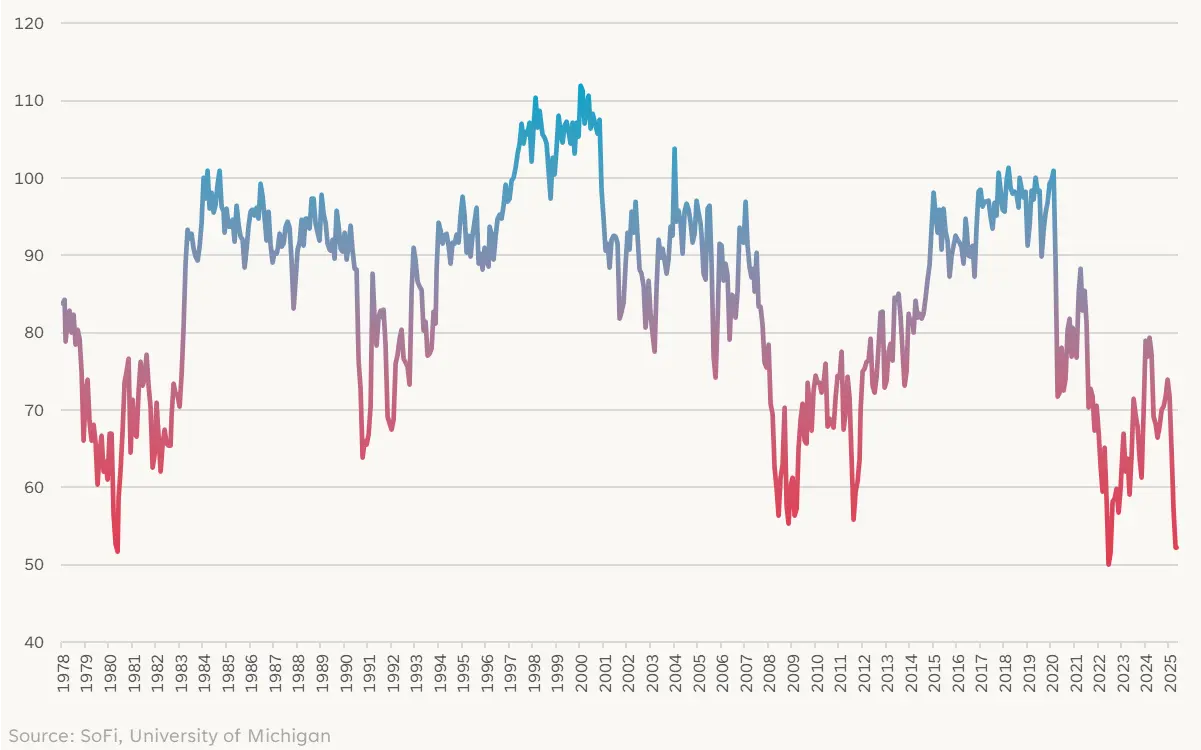

This conclusion makes sense given recent consumer sentiment trends, which according to the University of Michigan, is at its lowest levels outside of 1980 and 2022.

Consumer Sentiment At Historical Lows

Inflation unexpectedly slowing while consumers feel historically bad about the economy suggests businesses are facing margin pressure. If profit margins contract, that would likely weigh on stock prices, especially given an S&P 500 that has rebounded to near all-time highs.

How any of this goes is at the whims of trade policy. If it all gets resolved in an orderly manner, that margin pressure might actually never fully materialize. But outside of a quick resolution, who knows when the margin pressure might become apparent. In that environment, a more defensive posture by investors after a very favorable period for risk assets could be a prudent one.

Want more insights from SoFi’s Investment Strategy team? The Important Part: Investing With Liz Thomas, a podcast from SoFi, takes listeners through today’s top-of-mind themes in investing and breaks them down into digestible and actionable pieces.

SoFi can’t guarantee future financial performance, and past performance is no indication of future success. This information isn’t financial advice. Investment decisions should be based on specific financial needs, goals and risk appetite.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Mario Ismailanji is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Form ADV 2A is available at www.sofi.com/legal/adv.

Located in upstate New York, Syracuse University is known for its heavy emphasis on research and its schools of business, design, engineering, and communications, among others. With consistently high educational rankings, Syracuse has a lot to offer.

Total Cost of Attendance

Syracuse University tuition for the 2024-25 school year was $65,528. This is significantly higher than the national average of $41,540 for tuition at private universities.

Costs for 2024-25

Tuition & Fees

$65,528

Books & Supplies

$1,753

Room & Board

$19,188

Other Expenses

$2,024

Total Cost of Attendance

$88,493

Financial Aid

Generally, financial aid is monetary assistance awarded to students based on personal need or merit. Students who qualify for financial aid can use it to pay for college costs like tuition, books, and living expenses.

Syracuse University is “need blind” during the admissions process, which means a student’s ability to pay for their education will not be a factor when they apply.

For the 2022-23 school year, 84% of first-year Syracuse students used some sort of financial aid. The financial assistance consisted of student loans, grants, scholarships, or a combination.

The federal government is the largest provider of student financial aid. However, aid can also be given by state governments, colleges and universities, private companies, and nonprofits. The different types include:

• Scholarships: These can be awarded by schools and other organizations based on students’ academic excellence, athletic achievement, community involvement, job experience, field of study, or financial need.

• Grants: Generally based on financial need, these can come from federal, state, private, or nonprofit organizations.

• Work-study: This federal program provides qualifying students with part-time employment to earn money for expenses while in school.

• Federal student loans: This is money borrowed directly from the U.S. Department of Education. It comes with fixed interest rates that are typically lower than private loans.

Colleges, universities, and state agencies use the Free Application for Federal Student Aid (FAFSA) to determine financial aid eligibility. The FAFSA can be completed online, but note that state, federal, and school deadlines may differ.

You can find other financial aid opportunities on databases such as:

For the 2022-23 school year, 7% of first-year Syracuse students took out private student loans to cover educational costs, with an average balance of $33,651. By comparison, 29% of first-time students received federal loans.

Private loans are funded by private organizations such as banks, online lenders, credit unions, some schools, and state-based or -affiliated organizations. While federal student loans have interest rates that are regulated by Congress, private lenders follow a different set of regulations so their qualifications and interest rates can vary widely.

What’s more, private loans have variable or fixed interest rates that may be higher than federal loan interest rates, which are always fixed. Private lenders may (but don’t always) require you to make payments on your loans while you are still in school, compared to federal student loans, which you don’t have to start paying back until after you graduate, leave school, or change your enrollment status to less than half-time.

Private loans don’t have a specific application window and can be applied for on an as-needed basis. However, if you think you may need to take out a private loan, it’s a good idea to submit your FAFSA first to see what federal aid you may qualify for, since it generally has better rates and terms.

If you’ve missed the FAFSA deadline or you’re struggling to pay for school during the year, private loans can potentially help you make your tuition payments. Just keep in mind that you will need enough lead time for your loan to process and for your lender to send money to your school.

At Syracuse University, the price for a beginning undergraduate student in 2024-25 was $88,493. If this remains true for all four years, the price would be $353,972. This includes tuition, fees, books, room and board, and other expenses.

The cost at Syracuse is substantially higher than the average four-year cost at U.S. private institutions, which would be $241,680.

The combined cost of Syracuse University tuition, fees, books, and supplies in 2024-25 was $67,281.

Graduate Tuition and Fees

Costs for 2024-25

Tuition

$46,680

Fees

$1,452

Total Cost of Attendance

$48,132

Syracuse tuition for graduate students in 2024-25 was $46,680, plus $1,452 in fees, for a combined cost of $48,132. This is lower than the national average for one year of graduate school at a private, nonprofit university, which comes to $51,770.

There are many options for graduate loans that can help with these costs.

Cost per Credit Hour

For part-time students at Syracuse University, the cost per credit hour is $2,898.

Campus Housing Expenses

Costs for 2024-25

On Campus

Off Campus

Room & Board

$19,188

$1,472/mo*

Other Expenses

$2,024

$2,024

*Average rate based on available one-bedroom apartments on Syracuse University’s off-campus housing website in 2025.

At Syracuse University, students are required to live on campus for their first two years of enrollment. They’ll live in one of 10 residence halls that feature open- and split-double rooms, as well as single rooms and open-triple rooms

For upperclassmen who choose to live off-campus, there are many duplexes, apartments, and houses located within walking distance.

Syracuse University Acceptance Rate

Fall 2023

Number of Applications

Number Accepted

Percentage Accepted

42,089

17,677

42%

The Syracuse University acceptance rate for undergraduates is 42%.

Admission Requirements

Here’s what you’ll need to apply to Syracuse.

Required:

• High school transcript

• Senior year grade report

• Secondary school counselor evaluation

• One academic recommendation

Recommended:

• SAT or ACT scores

The deadline for Early Decision applications is November 15, with admission notifications starting in late December. The deadline for Early Decision II applications is January 5, with admission notifications starting in mid-January. The application deadline for Regular Decision is January 5, with admission notifications by late March.

SAT and ACT Scores

Syracuse University currently does not require standardized test scores. But it still can be helpful to see the scores of other students. Here are the standardized test scores at the 25th and 75th percentile for first-time students who enrolled in 2023.

Subject

25th Percentile

75th Percentile

SAT Evidence-Based Reading/Writing

630

710

SAT Math

630

720

ACT Composite

28

32

ACT English

28

34

ACT Math

26

30

Popular Majors at Syracuse University

With more than 200 majors and 100 minors in 13 different schools, you’ll have a hard time deciding what to study at Syracuse University. Here are the most popular majors.

1. Psychology

Syracuse offers both a Bachelor of Arts and a Bachelor of Science degree in Psychology. Courses include Using Robots to Understand the Mind, Psychology of Childhood, Decision Making, and Social Psychology, to name a few.

Undergraduate degrees in 2023-24: 233

2. Sport Management

In this program, students learn about sport business and finance, athletic event planning, facility management, and sports organization management.

Undergraduate degrees in 2023-24: 165

3. Information Management and Technology

This program combines business and technology to prepare students for careers in cloud computing, cybersecurity, web design and development, and project management.

Undergraduate degrees in 2023-24: 147

4. Architecture

Those pursuing an architecture degree take such classes as Introduction to Building Systems and Architectural History. However, the primary focus of the program is on studio experience, where students get one-on-one attention from faculty to develop their work.

Undergraduate degrees in 2023-24: 145

5. Finance

After taking courses like International Financial Management, New and Emerging Markets, Investments, and Working Capital Management, students go on to be financial analysts, investment bankers, portfolio managers, or sales and trading analysts.

Undergraduate degrees in 2023-24: 123

6. Communication and Rhetorical Studies

In this program, students sharpen their communication skills in courses like Concepts and Perspectives in Rhetorical Studies, Public Advocacy, Foundations of Inquiry in Human Communication, and Critical Research and Writing. They also have the opportunity to study abroad.

Undergraduate degrees in 2023-24: 111

7. Political Science

Political science students will take courses like Comparative Government & Politics, International Relations, Political Theory, Sexuality & the Law, and Politics in the Cyber-Age. After graduating, many work as legislators, diplomats, judges, news correspondents, or political scientists.

Undergraduate degrees in 2023-24: 110

8. Economics

Not only do economics majors learn everything from International Economics to Money and Banking, but they also have the chance to gain real-world experience as interns in local and global companies.

Undergraduate degrees in 2023-24: 109

9. Marketing Management

In addition to taking courses like Marketing Research, Consumer Behavior, Global Marketing Strategy, Brand Management, and Sales Management in B2B Markets, marketing majors also get the chance to get real-world experience and study abroad.

Undergraduate degrees in 2023-24: 107

10. Television, Radio, and Film

Students can take courses like Multimedia Storytelling, Topics in Entertainment Business, and Script Development that can launch them into careers in cinematography, music production, sound design, talent representation, and more. Semester-long coursework in Los Angeles and New York City enables students to get credit for hands-on experience.

Undergraduate degrees in 2023-24: 100

Graduation Rate

These are the graduation rates at Syracuse University:

• 4 years: 71%

• 6 years: 81%

• 8 years: 83%

Post-Graduation Median Earnings

After completing an undergraduate degree at Syracuse University, the median alumni salary is $79,164 per year. This is 16% higher than the national average salary of $68,516 for undergraduates.

Bottom Line

With so many fields of study, as well as a strong emphasis on research, Syracuse University offers students a stellar education. And while Syracuse tuition is expensive, the university is need blind, so you don’t have to worry about your ability to pay for college when you apply. Plus, there are plenty of Syracuse financial aid options to explore that could help you cover the cost.

SoFi private student loans offer competitive interest rates for qualifying borrowers, flexible repayment plans, and no origination fees.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loans are subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, the student's at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change. This information is current as of 4/22/2025 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Bank, N.A. and its lending products are not endorsed by or directly affiliated with any college or university unless otherwise disclosed.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

University of California, Davis (UC Davis) is a public research university and a premier campus located in Davis, California. Known for its top-ranked veterinary medicine program and its expansive, bike-friendly campus, UC Davis offers more than 100 undergraduate majors alongside graduate and professional degrees.

Keep reading to learn detailed information on UC Davis tuition and fees, financial aid opportunities, acceptance rates, admission requirements, and more.

Total Cost of Attendance

UC Davis has several noteworthy programs, including veterinary medicine and agriculture. In 2024-25, UC Davis tuition and fees was $16,774 for in-state students and $50,974 for out-of-state students. The national averages for public four-year schools are $11,260 for in-state students and $29,150 for out-of-state students.

Costs for 2024-2025

Student Type

In-State

Out-of-State

Tuition & Fees

$16,774

$50,974

Books & Supplies

$1,386

$1,386

Food & Housing

$19,426

$19,426

Other Expenses

$6,616

$6,616

Total Cost of Attendance

$44,202

$78,402

Financial Aid

At UC Davis, 58% of students use financial aid to help with UC Davis tuition. They may take out student loans or apply for grants and scholarships.

Generally, financial aid is monetary assistance awarded to students based on personal need and merit. Students who qualify for financial aid can use it to pay for college costs like tuition, books, and living expenses.

The federal government is the largest provider of student financial aid. However, aid can also be given by state governments, colleges and universities, private companies, and nonprofits. The different types include:

• Scholarships:Scholarships can be awarded by schools and other organizations based on students’ academic excellence, athletic achievement, community involvement, job experience, field of study, or financial need.

• Grants: Grants are generally based on financial need. These can come from federal, state, private, or nonprofit organizations.

• Work-study:Federal Work-Study provides qualifying students with part-time employment to earn money for expenses while in school.

• Federal student loans:Federal student loans are money borrowed directly from the U.S. Department of Education. They come with fixed interest rates that are typically lower than private loans.

Colleges, universities, and state agencies use the Free Application for Federal Student Aid (FAFSA®) to determine financial aid eligibility. The FAFSA can be completed online, but note that state, federal, and school deadlines may differ.

You can find other financial aid opportunities on databases such as:

When it comes to student loans, 22% of students at UC Davis take out federal loans, while 9% take out private loans. The average private student loan is $5,153.

Private loans are funded by private organizations such as banks, online lenders, credit unions, some schools, and state-based or -affiliated organizations. While federal student loans have interest rates that are regulated by Congress, private lenders follow a different set of regulations, so their qualifications and interest rates can vary widely.

What’s more, private loans have variable or fixed interest rates that may be higher than federal loan interest rates, which are always fixed. Private lenders may (but don’t always) require you to make payments on your loans while you are still in school, compared to federal student loans, which you don’t have to start paying back until after you graduate, leave school, or change your enrollment status to less than half-time.

Private loans don’t have a specific application window and can be applied for on an as-needed basis. However, if you think you may need to take out a private loan, it’s a good idea to submit your FAFSA first to see what federal aid you may qualify for, as it generally may have better rates and terms.

If you’ve missed the FAFSA deadline or you’re struggling to pay for school during the year, private loans can potentially help you make your payments. Just keep in mind that you will need enough lead time for your loan to process and for your lender to send money to your school.

To attend UC Davis for four years, students from California will pay $176,808, while students from other states will pay $313,608. The average cost for four years at a public university in the U.S. is $115,360 for in-state students, and $186,920 for out-of-state.

UC Davis tuition and fees, books and supplies, room and board, and miscellaneous expenses for the 2024-25 school year totaled $44,202 for in-state students and $78,402 for out-of-state students.

Graduate Tuition and Fees

Costs for 2024-2025

Student Type

In-State

Out-of-State

Tuition & Fees

$15,141

$30,243

University of California, Davis offers many well-respected graduate programs. UC Davis tuition for grad school is $12,762 (in-state) or $27,864 (out-of-state), plus fees totaling $2,379 for each. This is more than the average cost for one year of graduate school at a four-year public institution in the U.S., which is $10,320 per year. There are graduate loans available to help with these costs.

Cost per Credit Hour

UC Davis does not offer the ability to pay per credit hour, even if students attend part-time. Part-time students pay half the full-time tuition.

Campus Housing Expenses

Costs for 2024-25

Student Type

On-Campus

Off-Campus

Food & Housing

$19,426

$14,745

Other Expenses

$6,616

$7,254

Freshmen are not required to live on campus, though more than 90% choose to do so. There are 30 residence halls spread over three areas of campus for students to live in.

There are many options near campus for students who choose to live in apartments or houses, either on their own or with roommates.

University of California – Davis Acceptance Rate

Fall 2023

Number of applications

94,637

Number accepted

39,748

Percentage Accepted

42%

The UC Davis acceptance rate is 42%, which means that nearly half of the students who apply are accepted.

Admission Requirements

Here’s what’s required when applying at UC Davis:

Required:

• High school transcript and GPA

• College preparatory program

• Personal statement or essay

The deadline for applications to UC Davis is December 2. You can apply to UC Davis here .

SAT and ACT Scores

No SAT or ACT scores are considered with applications through the fall of 2024, and scores won’t be considered for scholarships during this period.

Popular Majors at the University of California Davis

UC Davis offers over 100 majors and programs. Here are the most popular majors at UC Davis.

1. Psychology

One of the most popular majors is psychology, which provides a base in research methods and statistics courses, as well as courses in mathematics, chemistry, biology, and psychology. Students have the opportunity to conduct research, help faculty with projects, or intern in the field.

Undergraduate degrees in 2023-24: 866

2. Management Sciences

In this program, students learn how to apply economic theory to business situations, develop problem-solving skills, and improve communication skills. Students can specialize in one of these areas: business economics, international business economics, environmental and resource economics, or agribusiness economics.

Undergraduate degrees in 2023-24: 498

3. Neurobiology and Anatomy

Building on a foundation in biological sciences, chemistry, mathematics, and physics, students can choose courses based on their interests, including animal behavior, physiology of particular organ systems or groups of animals, developmental neurobiology, and endocrinology.

Undergraduate degrees in 2023-24: 394

4. Economics & Quantitative Economics

Economics majors at UC Davis learn about microeconomics and macroeconomics, statistics, and mathematics, as well as economic theory, American or European economic history, and data analysis. Students can also choose courses such as games theory, financial institutions, or international economic development.

Undergraduate degrees in 2023-24: 392

5. Computer Science

Computer science students will learn about programming, networking, and database systems, and can customize their studies with courses on computer graphics, artificial intelligence, data visualization, or advanced mathematics.

Undergraduate degrees in 2023-24: 390

6. Human Development and Family Studies

This program explores the social, emotional, and cognitive development of humans, and provides hands-on learning experiences. Students will learn about nutrition and childhood and adult development. They will also get to participate in a practicum course and may opt for an internship.

Undergraduate degrees in 2023-24: 335

7. Biological Sciences

Biology students are given a solid foundation in biology, chemistry, mathematics, and physics, and can then take courses in molecular biology and genetics, animal behavior, plant growth and development, bioinformatics, marine biology, forensics, and microbiology.

Undergraduate degrees in 2023-24: 334

8. Animal Science

This program provides ample opportunity for hands-on learning with different types of animals. Students will also learn about animal behavior, biochemistry, genetics, nutrition, physiology, animal health, and productivity.

Undergraduate degrees in 2023-24: 294

9. Political Science

Political science students at UC Davis will learn about political concepts, institutions, behavior, and processes. Courses are available on American politics, comparative politics, international relations, public law, and political theory.

Undergraduate degrees in 2023-24: 240

10. Communication

Communications students learn about communications processes at different levels and delve into digital media and cross-cultural communications. They will study communication theory, specific communication processes, and the role and effects of mass media. They will also have the chance to intern in their field.

Undergraduate degrees in 2023-24: 239

Graduation Rate

The graduation rate for students who started at UC Davis in 2017 is 85%.

Post-Graduation Median Earnings

After graduating, students from UC Davis earn, on average, $80,838 per year. This is higher than the national average of $68,680 for the class of 2025.

Bottom Line

University of California, Davis is well-known for many of its programs, and the tuition is reasonable for such a respected institution. If you need help paying for UC Davis tuition, you can apply for scholarships, grants, federal student loans, and private student loans.

If you’ve exhausted all federal student aid options, no-fee private student loans from SoFi can help you pay for school. The online application process is easy, and you can see rates and terms in just minutes. Repayment plans are flexible, so you can find an option that works for your financial plan and budget.

Cover up to 100% of school-certified costs including tuition, books, supplies, room and board, and transportation with a private student loan from SoFi.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loans are subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, the student's at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change. This information is current as of 4/22/2025 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.