Current Mortgage Refinance Rates in Louisiana Today

LOUISIANA MORTGAGE REFINANCE RATES TODAY

Current mortgage refinance rates in

Louisiana.

Apply online or call for a complimentary mortgage consultation.

Compare mortgage refinance rates in Louisiana.

Key Points

• Mortgage refinance rates in Louisiana are influenced by a variety of economic factors, including the bond market, housing inventory, and inflation.

• Over recent years, Louisiana refinance rates have seen a significant shift, from as low as 3.00% in 2020 and to as high as 7.00% in 2023.

• Building a strong credit score, balancing your debt-to-income ratio, and shopping around among multiple lenders are key steps to snagging the most favorable mortgage refinance rates.

• A 1% drop in your mortgage rate in Louisiana could translate to substantial monthly savings — like, $2,000 a year on a $300,000 loan.

• Before you make the switch, it’s important to weigh the potential savings against the fees and closing costs, which typically range from 2% to 5% of the loan amount.

• Making the switch to a 15-year mortgage could be a smart move. This change can mean paying less interest over the loan’s lifetime, although it will likely mean adjusting to a higher monthly payment.

Introduction to Mortgage Refinance Rates

Mortgage refinancing is a process that lets you replace your existing mortgage with a new one. Your new mortgage will have different terms, such as a revised interest rate, term length, and monthly payment amount. People may refinance mortgages to lower monthly payments, access home equity, or change loan type. Understanding how current mortgage refinance rates in Louisiana are set and how to get the best possible rate is key to a successful refinance.

This guide will help you to understand the important steps of the refinance process and to make informed decisions about mortgage refinancing costs.

💡 Quick Tip: Wondering how to refinance a mortgage? The process, which takes about 30 to 45 days, is similar to when you got your original home loan.

Where Do Mortgagee Refi Rates Come From?

Mortgage refinance interest rates rise and fall depending on economic factors, as well as your individual financial profile. The bond market — and particularly the performance of the 10-year U.S. Treasury Note — plays an important role in setting current mortgage rates. When the Treasury Note yield increases, mortgage interest rates tend to rise as well.

Housing market inventory in Louisiana is also significant. If the market slows down and more homes are available than there are buyers, lenders might lower their rates to attract customers. The overall economic environment is another factor: A robust job market and resulting economic growth can push interest rates higher, while a recession typically results in lower rates.

As a borrower or mortgage applicant, a strong credit score and a low debt-to-income ratio can help you secure the best possible rate.

How Interest Rates Affect Home Affordability

Interest rates are super important because they help determine your monthly refinance payment. (Of course, your payment is influenced by your loan amount and the term over which you’ll repay it, too.) Here’s an example of how much your interest rate impacts your payment:

A $200,000 loan with a 6.00% interest rate and a 30-year term translates to a monthly payment of $1,199. If that interest rate jumps to 8.00%, the monthly payment increases to $1,467. Over the life of the loan, you’d pay almost $100,000 less with the lower interest rate. Even a small change can make a big difference in your savings and your home loan’s ultimate affordability, as this chart illustrates.

| Interest Rate | Monthly Payment | Total Interest |

|---|---|---|

| 6.00% | $1,199 | $231,677 |

| 6.50% | $1,264 | $255,085 |

| 7.00% | $1,330 | $279,021 |

| 7.50% | $1,398 | $303,403 |

| 8.00% | $1,467 | $328,309 |

Why Should You Refinance Your Mortgage in Louisiana

Refinancing your mortgage can offer a number of different benefits, depending on your financial goals. If current interest rates are lower than that on your existing mortgage, refinancing can reduce your monthly payments and save you money over the life of the loan. Refinancing can also help you switch from an adjustable-rate mortgage to a fixed-rate loan for long-range savings.

Whatever your reason, you should have at least 20% equity in your home before you embark on a refinance, especially if you want to cash out some equity in the process.

Common Reasons to Refinance a Mortgage

These are common reasons for homeowners to refinance mortgages:

• You qualify for a lower interest rate due to improved credit or market conditions.

• You’re considering adjusting your repayment term so you can lower your monthly payments or pay off the loan more swiftly.

• You want to tap into your home equity to fund a significant expense, like a home remodel.

• Your adjustable-rate mortgage is going to reset soon, and you want to switch to a fixed-rate loan.

• You have an FHA loan and 20% equity, and you want to get mortgage insurance out of your life.

• You’re considering a debt consolidation, or releasing a cosigner.

Recommended: How Soon Can You Refinace a Mortgage?

How to Get the Best Available Refi Interest Rate

Your financial history has an impact on the interest rates that lenders offer you. Homeowners with strong credit and a low debt-to-income ratio may secure lower-than-average rates.

To secure a competitive mortgage refinance rate, here’s what to work on:

• Bolster your credit score by paying your bills on time, and steer clear of new debt.

• Maintain a debt-to-income ratio that is under 36%.

• Look at offers from multiple lenders, focusing on the APR rather than just the interest rate.

• Consider buying mortgage discount points, which can help you lower your interest rate.

• If you can manage the higher payments, go for a shorter mortgage term.

Once you’ve achieved an optimal credit history, it’s time for a deep dive into interest rate trends.

Trends in Louisiana Mortgage Interest Rates

As the national trend shows, the rise and fall of mortgage rates can feel like riding a rollercoaster. In 2021, the average 30-year fixed mortgage rate in Louisiana was 3.15%. Fast-forward to 2023, and rates had soared to 7.00%.

Last year brought an expectation of a dip in mortgage refi rates. But for 2025’s first half, experts predict that rates will remain elevated longer. You don’t need to let those forecasts deter you, though. A mortgage refinance might still be a smart move for you.

Historical U.S. Mortgage Interest Rates

In the chart below, you’ll see that rates were around 6.00% in the early 2000s. They dropped to under 3.00% in 2020 — and cemented the idea that low rates were “normal.” In 2023, they rose again to around 7.00%. While many people today complain about high interest rates, current mortgage refinance rates are below the 50-year average.

Historical Interest Rates in Louisiana

Refinance rates in Louisiana typically follow national trends, but they may be slightly higher or lower, especially in certain regions. In the past, Louisiana has seen some of the country’s lowest refinance rates. Understanding the historical trends in the state’s refinance rates can help you anticipate future rate movements and make more informed refinancing decisions.

| Year | Louisiana Rate | National Rate |

|---|---|---|

| 2000 | 7.89 | 8.14 |

| 2001 | 6.86 | 7.03 |

| 2002 | 6.20 | 6.62 |

| 2003 | 6.43 | 5.83 |

| 2004 | 5.65 | 5.95 |

| 2005 | 5.91 | 6.00 |

| 2006 | 6.54 | 6.60 |

| 2007 | 6.38 | 6.44 |

| 2008 | 6.10 | 6.09 |

| 2009 | 4.99 | 5.06 |

| 2010 | 4.81 | 4.84 |

| 2011 | 4.46 | 4.66 |

| 2012 | 3.67 | 3.74 |

| 2013 | 3.84 | 3.92 |

| 2014 | 4.13 | 4.24 |

| 2015 | 3.89 | 3.91 |

| 2016 | 3.72 | 3.72 |

| 2017 | 4.12 | 4.03 |

| 2018 | 4.55 | 4.57 |

💡 Quick Tip: Some lenders offer a so-called no-closing-cost refinance. However, that usually means either rolling the closing costs into the new mortgage principal or exchanging them for a higher interest rate.

Choose the Right Mortgage Refinance Type

It’s no secret that refinance rates can be higher than purchase mortgage rates. But the actual rate you’ll get may vary a lot depending on the type of refinance you choose. How to refinance your mortgage? Several different refi options are available to consider, each with its own features and potential benefits.

By understanding their differences, you can make an informed decision about which type of refinance is the best fit for your situation, and get the best rate and terms to meet your needs.

Conventional Refi

Referred to as a rate-and-term refi as well as a conventional refi, this option generally has a higher rate than a government-backed loan, including an FHA, VA, or USDA mortgage. This refinance choice can empower you to adjust your interest rate or loan term so you can potentially reduce your monthly payment or the time it takes to pay off the loan.

A conventional refi is a great pick for a homeowner with solid equity and a strong credit history. By securing a lower mortgage refinance rate, you can save money over the term of your loan and reach your financial goals more swiftly. That’s a win-win.

15-Year Mortgage Refi

A type of conventional refi, this choice typically shortens the length of your loan repayment. A 15-year mortgage refinance can lead to significant savings in the long run, even though your monthly payments will go up. For example, if you are carrying a 30-year, $1 million loan at a 7.50% mortgage refinance rate, you’re looking at a monthly payment of $6,992 and can expect to pay a total interest amount of $1,517,167.

Refinance to a 15-year mortgage at a 7.00% rate, and your monthly payment will increase to approximately $8,988. But your total interest paid by the time the loan is finished would drop to $617,891. You would save nearly $900,000 in the end. That’s a lot of cash — and it’s a very nice feeling to be out from under your loan in a mere 15 years. Obviously, your cash flow will play a critical role in whether you can go for something like this.

Adjustable-Rate Mortgage Refi

Another kind of conventional refi, adjustable-rate mortgages (ARMs) start with lower mortgage refinance rates than fixed-rate loans do, but the rates can change over time. If you plan to sell your home before the rate adjusts, refinancing from a fixed-rate mortgage to an ARM will help lower your monthly payment and save you money in the short term. Key words, short term. If your plans may change, think hard on this.

An adjustable-rate mortgage refi can be a good strategy if you have definite plans to move or if you are confident that you will increase your income in the next few years.

Cash-Out Refi

A cash-out refinance is a powerful tool that lets homeowners unlock their property’s value by taking out a new mortgage for more than they owe. It’s like turning your home equity into cash, and you can use it for whatever you need — paying off high-interest debt or making long-desired home improvements.

The amount you can borrow will be based on the equity you have in your home. If your home is worth $500,000 and your mortgage balance is $300,000, for example, you have $200,000 in equity in your property. With a cash-out refi, a lender may approve you to borrow up to 80% of your equity. That would leave you with a chunk of available cash after you pay off your existing mortgage. The lump sum could help you pay off a nagging debt or finance a major expense.

FHA Refi

FHA refinances are backed by the Federal Housing Administration. They often come with more favorable mortgage refinance rates — sometimes a full percentage point lower than conventional loans. The different types of FHA refinance options include FHA Simple Refinance, FHA Streamline Refinance, FHA Cash-Out Refinance, and FHA 203(k) Refinance. The first two are for homeowners with existing FHA loans, and the latter two you can qualify for whether you have an FHA loan or not.

The cash-out refinance can be used to pay off debt or to make a home upgrade. The 203(k) refinance is specifically for home improvements. These FHA refinance options can help you change your current mortgage terms and get a more affordable interest rate, plus lower your monthly payment or access your home’s equity for other financial needs.

VA Refi

VA refinances, backed by the U.S. Department of Veterans Affairs, offer some of the most competitive mortgage refinance rates available. That said, to be eligible for a VA refinance, also known as an Interest Rate Reduction Refinance Loan (IRRRL), you must currently hold a VA loan. This type of refinance may significantly reduce your monthly payments and let you accumulate substantial interest savings over your loan’s life.

Compare Mortgage Refi Interest Rates

To ensure you get the best deal, always compare rates from multiple lenders in your state. Look at more than the interest rate and consider the annual percentage rate (APR) — it incorporates fees and any discount points. Calculate the total loan cost and the point where you’ll break even (that is, when the amount you save cancels out the cost of the refinance). Watch your credit score and your home’s value. The higher they are, the more favorable rates you’ll be eligible for.

Online Refinance Calculators

An online mortgage calculator can be helpful in figuring out your new monthly payment or comparing different refinance options in Louisiana. It can help you understand the potential savings you’ll get from refinancing — you’ll need to plug in your current loan balance, your interest rate, and the terms of the new loan. Using a refinance calculator will help you make an informed decision about whether or not refinancing is the right plan. /p>

Run the numbers on your home loan.

-

Mortgage calculator

Punch in your home loan amount and a new interest rate, and we’ll estimate your payoff date.

-

Down payment calculator

Enter a few details about your home loan and we’ll provide your monthly mortgage payment.

-

Home affordability calculator

Provide us with a few details and see how much you can afford to spend on a home purchase.

Using the free calculators is for informational purposes only, does not constitute an offer to receive a loan, and will not solicit a loan offer. Any payments shown depend on the accuracy of the information provided.

The Takeaway

Refinancing your mortgage in Louisiana can be a smart financial move. It does require thinking about your goals, though, along with research on the costs involved. To make the best decision, be sure to explore different types of refinancing options, including a cash-out, FHA, VA, and adjustable-rate mortgage options.

SoFi can help you save money when you refinance your mortgage. Plus, we make sure the process is as stress-free and transparent as possible. SoFi offers competitive fixed rates on a traditional mortgage refinance or cash-out refinance.

A mortgage refinance could be a game changer for your finances.

FAQ

When is mortgage refinancing a smart idea?

If you can lock in a lower interest rate, consolidate your debt, or meet other important financial goals, a mortgage refi might be a smart financial decision. Do the math to figure out at what point the cash you’ll save by refinancing will exceed the money you’ll spend on the refi. How long will you stay in the home? If you’ll move before you’ve recouped the cost of your refi, it won’t make sense to do it.

Can I get cash out of my house without refinancing?

You can tap into your home’s equity to get money without a refinance by requesting a home equity line of credit (HELOC) or taking out a home equity loan. These options can be great ways to pay for home improvements, consolidate debt, or cover other expenses that come up. Technically, a HELOC or home equity loan is a second mortgage (assuming you still have your first one).

How much are refinancing closing costs?

If you’re just thinking on a mortgage refinance, it’s easiest to look at average closing costs. They tend to fall between 2% and 5% of the loan amount. Different lenders, refinance types, and locations can make these costs fluctuate. A no-closing-cost refinance sounds like an amazing find, but know that those costs don’t disappear — they will get folded into the new mortgage, or exchanged for a higher interest rate.

Can I just request a lower interest rate from my lender?

Any borrower can reach out to a lender and request a lower interest rate on their mortgage. But it’s entirely possible that the lender will decline your request, especially if you don’t have a spotless payment history or top-notch credit. If you’re having trouble making your payment, ask your lender for a mortgage loan modification or loan forbearance, in which payments are temporarily paused. In either case, you may need to demonstrate financial hardship.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

†Veterans, Service members, and members of the National Guard or Reserve may be eligible for a loan guaranteed by the U.S. Department of Veterans Affairs. VA loans are subject to unique terms and conditions established by VA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. VA loans typically require a one-time funding fee except as may be exempted by VA guidelines. The fee may be financed or paid at closing. The amount of the fee depends on the type of loan, the total amount of the loan, and, depending on loan type, prior use of VA eligibility and down payment amount. The VA funding fee is typically non-refundable. SoFi is not affiliated with any government agency.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Qualifying for the reward requires using a real estate agent that participates in HomeStory’s broker to broker agreement to complete the real estate buy and/or sell transaction. You retain the right to negotiate buyer and or seller representation agreements. Upon successful close of the transaction, the Real Estate Agent pays a fee to HomeStory Real Estate Services. All Agents have been independently vetted by HomeStory to meet performance expectations required to participate in the program. If you are currently working with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®. A reward is not available where prohibited by state law, including Alaska, Iowa, Louisiana and Missouri. A reduced agent commission may be available for sellers in lieu of the reward in Mississippi, New Jersey, Oklahoma, and Oregon and should be discussed with the agent upon enrollment. No reward will be available for buyers in Mississippi, Oklahoma, and Oregon. A commission credit may be available for buyers in lieu of the reward in New Jersey and must be discussed with the agent upon enrollment and included in a Buyer Agency Agreement with Rebate Provision. Rewards in Kansas and Tennessee are required to be delivered by gift card.

HomeStory will issue the reward using the payment option you select and will be sent to the client enrolled in the program within 45 days of HomeStory Real Estate Services receipt of settlement statements and any other documentation reasonably required to calculate the applicable reward amount. Real estate agent fees and commissions still apply. Short sale transactions do not qualify for the reward. Depending on state regulations highlighted above, reward amount is based on sale price of the home purchased and/or sold and cannot exceed $9,500 per buy or sell transaction. Employer-sponsored relocations may preclude participation in the reward program offering. SoFi is not responsible for the reward.

SoFi Bank, N.A. (NMLS #696891) does not perform any activity that is or could be construed as unlicensed real estate activity, and SoFi is not licensed as a real estate broker. Agents of SoFi are not authorized to perform real estate activity.

If your property is currently listed with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®.

Reward is valid for 18 months from date of enrollment. After 18 months, you must re-enroll to be eligible for a reward.

SoFi loans subject to credit approval. Offer subject to change or cancellation without notice.

The trademarks, logos and names of other companies, products and services are the property of their respective owners.

SOHL-Q125-173

More refinance resources.

-

How Much Does It Cost to Refinance a Mortgage?

-

How to Refinance a Home Mortgage Loan

-

7 Signs It’s Time for a Mortgage Refinance

Apply online or call for a complimentary mortgage consultation.

Current Mortgage Refinance Rates in Kansas Today

Apply online or call for a complimentary mortgage consultation.

Compare mortgage refinance rates in Kansas.

Key Points

• Mortgage refinance rates are influenced by economic factors such as Federal Reserve policy, inflation, the bond market, and housing inventory, as well as your credit profile.

• Even a 1% drop in the refinance rate can translate to major monthly savings, which could add up to quite the sum over the life of the loan.

• The average 30-year fixed mortgage refinance rate in Kansas has fluctuated from historic lows in 2021 to 7.00% recently. Higher rates may continue through at least 2025.

• There are many different kinds of refi options, such as conventional, government-backed, adjustable-rate, cash-out, and 15-year mortgages.

• FHA and VA refinances often offer more competitive mortgage refinance rates compared to conventional loans, with VA refinances typically providing the lowest rates.

Introduction to Mortgage Refinance Rates

When you’re considering a mortgage refinance in Kansas, the rates you’ll be offered are pivotal. A refinance essentially means trading your current mortgage for a new one, complete with updated terms and a fresh interest rate. This might lower your monthly payments on your home loan, or it could be a way to shift your mortgage term or translate home equity into cash.

The reason behind your refinance will dictate the type you opt for, and this, in turn, influences the interest rate you’ll secure. Here, you’ll delve into how these rates are determined and how you can position yourself to snag the most favorable one.

💡 Quick Tip: Wondering how to refinance a mortgage? The process, which takes about 30 to 45 days, is similar to when you got your original home loan.

Where Do Mortgage Refi Rates Come From?

Refi rates for home loans are a product of a complex interplay of economic factors and your own financial situation. The big economic factors include Federal Reserve policy, inflation, the bond market, and housing inventory levels.

Generally, higher inflation and more frequent federal funds rate hikes lead to higher refi rates. Conversely, when bond prices are rising, interest rates tend to fall. And when there’s a slowdown in home sales, that can also lead to lower rates.

What’s more, your own credit profile — which lenders factor in when deciding whether to approve an applicant and at what rate — counts, too. Your credit score reflects how well you have managed debt in the past. With a higher score, you appear to be a borrower who is likely to repay debt on time, and therefore you qualify for a lower interest rate. With a lower score, which indicates poor handling of debt, you will probably be assessed a higher interest rate since the lender wants to protect itself.

By understanding these factors, you can make a more informed decision about when and how to refinance your mortgage.

How Interest Rates Affect Home Affordability

Interest rates play a pivotal role in the affordability of your refinance. Your monthly mortgage payment amount

hinges on the loan principal, repayment term, and the mortgage refinance rate. Here’s an example:

• If you take out a $200,000 home loan with a 6.00% interest rate and a 30-year repayment term, you would have a monthly payment of $1,199.

• Now, if the interest rate were 8.00%, that same loan would translate to a higher monthly payment of $1,467. That means almost $300 less per month in your bank account — and for three decades.

Qualifying and opting for a lower mortgage refinance rate can lead to significant savings over the life of your loan.

Why Refinance in Kansas

Refinancing your mortgage can be a savvy financial move. If current mortgage interest rates are lower than your existing home loan, it might be a good time to refi. The reason behind your refi will determine the type of refinance to choose, and that will impact your rate.

Common Reasons to Refinance a Mortgage

Each person’s financial path and refi motivations will be unique, but here are some common reasons homeowners refinance their mortgage:

• You qualify for a lower mortgage refinance rate because of market conditions or due to your building your credit profile.

• You’re considering adjusting your repayment term to better suit your financial goals.

• You may want to tap into your home’s equity to cover expenses like education or home improvements.

• Your adjustable rate is about to shift, and you’re considering a switch to a fixed-rate loan.

• You have an FHA loan and have reached 20% equity, and you want to eliminate your FHA mortgage insurance premium.

• You need to remove a cosigner from your loan.

How to Get the Best Available Mortgage Refi Interest Rate

On the topic of mortgage refinance rates, it’s wise to do your research and take steps to snag the best possible percentage for your situation. Here are some moves that can help you do that when thinking about a Kansas refi:

• Build your credit score by managing payments and debt wisely. The single most important facet: Pay your bills on time, every time.

• Strive for a debt-to-income ratio of 36% or less.

• Compare rates and fees from multiple lenders.

• Think about buying mortgage points: These add to your costs but lower your interest rate, saving you money over the life of the loan.

• Think about choosing a shorter loan term to grab a lower rate. While this will typically increase your monthly payments, the overall interest you pay can drop dramatically.

More advice to heed: There are factors to consider when refinancing beyond simply snagging a lower interest rate:

• In terms of how soon you can refinance, you typically need 20% home equity before you can move ahead. If you bought a home a couple of years ago with, say, 5% down, you may have to bide your time.

• Make sure your calculations include mortgage refinancing costs. For instance, closing costs usually total about 2% to 5% of your loan amount. On a $300,000 mortgage, that means you’ll have $6,000 to $18,000 that you are responsible for paying or rolling into the loan.

Understand Trends in Kansas Mortgage Interest Rates

Mortgage rates aren’t static. As you’ve read, they rise and fall due to economic factors and the impact of your own financial profile. Here, take a closer look at how national and Kansas mortgage refinance rates can fluctuate. Staying attuned to these trends can empower you to make shrewd choices about when to pursue mortgage refinancing, potentially netting you more favorable terms.

Historical U.S. Mortgage Interest Rates

Mortgage refinance rates in the U.S. have seen some dramatic ups and downs in recent years. For example, the average 30-year fixed mortgage refinance rate was 3.15% in 2021, but it shot up to 7.00% in 2023. And it’s expected to stay in this higher range through at least 2025.

By knowing what has happened with rates in the past, you can better understand and anticipate what might happen in the future. That can help you make more informed decisions about refinancing, which can help you meet your financial goals. The graph below shows how fixed-rate mortgages have evolved over the last few decades.

Historical Interest Rates in Kansas

The mortgage refinance rates in Kansas have been on a rollercoaster ride in recent years, as have national rates. As noted above, rates soared between 2021 and 2023, and it looks like these higher rates are here to stay for 2025, despite early predictions that an interest rate drop was imminent.

If you’re thinking about refinancing your home, it’s crucial to understand these market trends. Armed with this knowledge, you can make a well-informed decision about when to refinance your mortgage. To help you do that, review the chart below. It chronicles almost two decades of rates in Kansas compared to the national rate, which can help you grasp trends at both levels. You’ll see that Kansas refinance rates have often been a bit under the U.S. rate. (The data points below stop at 2018 since the Federal Housing Finance Agency stopped compiling state by state intel at that time.)

| Year | Kansas Rate | National Rate |

|---|---|---|

| 2000 | 7.90 | 8.14 |

| 2001 | 6.94 | 7.03 |

| 2002 | 6.54 | 6.62 |

| 2003 | 5.69 | 5.83 |

| 2004 | 5.72 | 5.95 |

| 2005 | 5.78 | 6.00 |

| 2006 | 6.27 | 6.60 |

| 2007 | 6.14 | 6.44 |

| 2008 | 5.83 | 6.09 |

| 2009 | 5.03 | 5.06 |

| 2010 | 4.77 | 4.84 |

| 2011 | 4.28 | 4.66 |

| 2012 | 3.58 | 3.74 |

| 2013 | 3.78 | 3.92 |

| 2014 | 4.11 | 4.24 |

| 2015 | 3.77 | 3.91 |

| 2016 | 3.68 | 3.72 |

| 2017 | 4.02 | 4.03 |

| 2018 | 4.64 | 4.57 |

Choose the Right Mortgage Refi Type

There are several different kinds of mortgage refinances available in Kansas, each with their own pros and cons and interest rates. Finding the one that suits you is important, so get set to dive into the details.

Worth noting: When shopping for a mortgage refi: Remember to look at annual percentage rates (APRs) vs. simple interest rates. APRs reflect the true cost of your loan with fees and mortgage points rolled in. Each option comes with its own set of features and benefits:

Conventional Refi

A conventional Kansas refinance, also known as a rate-and-term refinance, typically has higher mortgage refinance rates than government-backed loans. This type of refinance allows you to adjust your interest rate or loan term. It’s best for homeowners who want to lower their interest rate or change their repayment schedule. Keep in mind that conventional refinances require a minimum credit score (usually 620 or higher) and adequate equity in the property (20% or higher is the norm), which can vary by lender and borrower.

Cash-Out Refi

Cash-out refinances can be a smart way for you to leverage your home equity by borrowing more than your current mortgage balance. Say your home is valued at $500,000, and you still owe $300,000. With a cash-out refi, you could borrow up to 80% of your home’s equity, which is $200,000, or the difference between the property’s value and the outstanding amount of your mortgage.

15-Year Mortgage Refi

Refinancing from a 30-year to a 15-year mortgage in Kansas can be a game-changer, slashing your total interest payments. Here’s how it might work: Say you have a 30-year $1 million mortgage at a 7.50% interest rate. That’s a monthly payment of about $6,992 and a jaw-dropping total interest to be paid of $1,517,167.

If you refinanced to a 15-year mortgage at a 7.00% rate, the monthly payment jumps significantly, to roughly $8,988. However, the total interest paid is slashed to around $617,891, leaving you with savings of nearly $900,000. That could make a major difference to your financial profile and reaching long-term money goals.

Adjustable-Rate Mortgage Refi

Adjustable-rate mortgages (ARMs) start with a lower introductory mortgage refinance rate than fixed-rate loans. However, their rates have the potential to increase over time, as market conditions change. If you’re planning to move before the rate adjusts, refinancing with an ARM could be an affordable way to lower your monthly payments and get significant interest savings for the short term.

However, make sure you can handle a potential rate jump. What if life throws you a curveball and you can’t or don’t want to move as originally planned? It’s wise to be prepared for various scenarios relating to your mortgage refi in Kansas.

FHA Refi

FHA refis, backed by the United States Department of Housing and Urban Development, often offer lower mortgage refinance rates. These are sometimes a full percentage point lower than conventional loans, which can mean major savings. If you already have an FHA loan, you might qualify for an FHA Simple Refinance or an FHA Streamline Refinance.

If you don’t have an existing FHA loan, you could consider an FHA cash-out refinance or an FHA 203(k) refinance, which could be a great option if you’re planning home renovations. These FHA refinance options offer a range of benefits, including potentially lower interest rates, flexible credit requirements, and streamlined closing processes.

VA Refi

VA loans help active-duty members of the military, veterans, and some spouses achieve their dreams of homeownership. VA refinances, backed by the U.S. Department of Veterans Affairs, often have some of the most competitive mortgage refinance rates. To be eligible for a VA refinance, also known as an Interest Rate Reduction Refinance Loan (IRRRL), you must have an existing VA loan. This type of refinance can be a great way to lower your monthly payments and save significant interest over the life of the loan.

Compare Mortgage Refi Interest Rates

Snagging a competitive mortgage refinance rate can open up some room in your monthly budget and/or save you significant money over the life of your loan, among other benefits. As you do your research, here are some tips for comparing rates:

• Shop around with different lenders to find the best rate and terms.

• Get prequalified to see how much you can borrow and at what rate without dinging your credit score.

• Compare each loan’s annual percentage rate (APR), which includes the interest rate, fees, and discount points (aka mortgage points; an additional cost that can help you buy down your mortgage rate to lower costs over the life of the loan).

• Use a mortgage refinancing calculator to estimate your new monthly payments and potential savings when comparing offers.

• Evaluate the total cost of the new mortgage and your break-even point. What’s the break-even point? It’s when the cost of refinancing is outweighed by the savings of your new refi rate. If you’re planning on moving before you hit that break-even point, refinancing may not be the best option.

💡 Quick Tip: Some lenders offer a so-called no-closing-cost refinance. However, that usually means either rolling the closing costs into the new mortgage principal or exchanging them for a higher interest rate.

Use an Online Refinance Calculator

Online refinance calculators, mentioned above, can be a great way to get a rough idea of what your monthly payment will be and to compare different refinance options. In addition to being fast and convenient (no punching those calculator keys required), they can help you understand how different mortgage refinance rates and terms can impact your financial situation.

This knowledge can help you decide if refinancing makes sense for you and, if so, which option may suit your unique situation and long-term financial goals best.

Run the numbers on your home loan.

-

Mortgage calculator

Punch in your home loan amount and a new interest rate, and we’ll estimate your payoff date.

-

Down payment calculator

Enter a few details about your home loan and we’ll provide your monthly mortgage payment.

-

Home affordability calculator

Provide us with a few details and see how much you can afford to spend on a home purchase.

Using the free calculators is for informational purposes only, does not constitute an offer to receive a loan, and will not solicit a loan offer. Any payments shown depend on the accuracy of the information provided.

The Takeaway

Refinancing a mortgage can be a smart financial move, but it does require some careful thought and preparation. By understanding your options and comparing mortgage refinance rates, you can potentially save a lot of money in interest payments. It’s important to weigh the benefits against the costs to make sure refinancing makes sense for your situation and your big-picture financial goals.

SoFi can help you save money when you refinance your mortgage. Plus, we make sure the process is as stress-free and transparent as possible. SoFi offers competitive fixed rates on a traditional mortgage refinance or cash-out refinance.

A mortgage refinance could be a game changer for your finances.

FAQ

Will refinancing hurt my credit score?

Refinancing might nudge your credit score down a bit, but it’s usually a small and temporary dip. It’s typically triggered by the hard credit inquiry involved in the approval of your refi application. This can lower your credit score by several points for a number of months.

Do you have to pay closing costs when you refinance?

Yes, you will need to cover closing costs once more when you refinance, which typically total between 2% and 5% of the loan amount. Covering the expenses of securing the new mortgage refinance loan, these costs vary depending on the lender and the type of refinance you choose. You might pay them upfront, or they could be rolled into your loan. Make sure you understand exactly how much they are and how you will pay for them as you move through the refi process.

How many times can you refinance a mortgage?

There isn’t a set number of times you can refinance your home, but it’s important to keep in mind that each refinance comes with closing costs and could affect your credit. It’s wise to consider the potential benefits of securing a new mortgage refinance rate against the costs, and to make sure you’re doing it for the right reasons and at the right time.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

†Veterans, Service members, and members of the National Guard or Reserve may be eligible for a loan guaranteed by the U.S. Department of Veterans Affairs. VA loans are subject to unique terms and conditions established by VA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. VA loans typically require a one-time funding fee except as may be exempted by VA guidelines. The fee may be financed or paid at closing. The amount of the fee depends on the type of loan, the total amount of the loan, and, depending on loan type, prior use of VA eligibility and down payment amount. The VA funding fee is typically non-refundable. SoFi is not affiliated with any government agency.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Qualifying for the reward requires using a real estate agent that participates in HomeStory’s broker to broker agreement to complete the real estate buy and/or sell transaction. You retain the right to negotiate buyer and or seller representation agreements. Upon successful close of the transaction, the Real Estate Agent pays a fee to HomeStory Real Estate Services. All Agents have been independently vetted by HomeStory to meet performance expectations required to participate in the program. If you are currently working with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®. A reward is not available where prohibited by state law, including Alaska, Iowa, Louisiana and Missouri. A reduced agent commission may be available for sellers in lieu of the reward in Mississippi, New Jersey, Oklahoma, and Oregon and should be discussed with the agent upon enrollment. No reward will be available for buyers in Mississippi, Oklahoma, and Oregon. A commission credit may be available for buyers in lieu of the reward in New Jersey and must be discussed with the agent upon enrollment and included in a Buyer Agency Agreement with Rebate Provision. Rewards in Kansas and Tennessee are required to be delivered by gift card.

HomeStory will issue the reward using the payment option you select and will be sent to the client enrolled in the program within 45 days of HomeStory Real Estate Services receipt of settlement statements and any other documentation reasonably required to calculate the applicable reward amount. Real estate agent fees and commissions still apply. Short sale transactions do not qualify for the reward. Depending on state regulations highlighted above, reward amount is based on sale price of the home purchased and/or sold and cannot exceed $9,500 per buy or sell transaction. Employer-sponsored relocations may preclude participation in the reward program offering. SoFi is not responsible for the reward.

SoFi Bank, N.A. (NMLS #696891) does not perform any activity that is or could be construed as unlicensed real estate activity, and SoFi is not licensed as a real estate broker. Agents of SoFi are not authorized to perform real estate activity.

If your property is currently listed with a REALTOR®, please disregard this notice. It is not our intention to solicit the offerings of other REALTORS®.

Reward is valid for 18 months from date of enrollment. After 18 months, you must re-enroll to be eligible for a reward.

SoFi loans subject to credit approval. Offer subject to change or cancellation without notice.

The trademarks, logos and names of other companies, products and services are the property of their respective owners.

SOHL-Q125-171

More refinance resources.

-

How Much Does It Cost to Refinance a Mortgage?

-

How to Refinance a Home Mortgage Loan

-

7 Signs It’s Time for a Mortgage Refinance

Apply online or call for a complimentary mortgage consultation.

Love and Money: How Couples Manage Their Finances in the First Year of Marriage

When couples get married, managing money can be a challenge. Who makes the decisions and pays the bills? Should you merge your money or keep it separate? How do you handle debt? To find out how couples navigate these tricky issues and more, in August/September 2024 SoFi surveyed 600 adults who have been married less than one year about how they approach finances in their relationship.

Our findings suggest that most newlyweds communicate early and often about financial issues, are relatively in sync when it comes to saving and spending, and merge at least some of their money. However, they also prize their independence: The majority maintain separate bank accounts, have pre-nuptial or post-nuptual agreements, and some even keep financial secrets from their partner.

Key Findings

Some highlights of SoFi’s 2024 Love & Money survey of recently married couples include:

• 82% keep at least some of their money separate from their spouses.

• 62% have a joint bank account.

• 36% have a pre-nuptial agreement and 21% have a post-nuptial agreement.

• 72% put one partner in charge of day-to-day money management.

• 22% keep financial secrets from their spouse.

• 40% of couples are still paying off wedding debt.

Managing Money: Yours, Mine, or Ours?

Should you merge your money after marriage or keep at least some of it separate? There’s no one-size-fits-all solution. Any set-up can work as long as the lines of communication stay open. Here’s what today’s newlyweds are doing according to our survey.

42% Have Both Joint and Individual Bank Accounts

As a practical matter, joint bank accounts can make sense after marriage, since it’s typically easier to manage household expenses with a shared account. Joint accounts also enable financial transparency. But most survey respondents also want to maintain their financial autonomy.

While 20% have merged all their funds into one joint account, nearly 40% maintain only individual accounts. The most popular option (chosen by 42%) is a hybrid approach: having both joint and individual accounts.

How does the hybrid approach work? One option is to have income go directly into the joint account for shared expenses, then set up a monthly transfer into each partner’s personal account. Or, you might have income go into your personal accounts then each make a monthly transfer into the joint account, for household bills and shared expenses. Your contribution can be the same or proportional based on income.

72% Put One Partner in Charge of Everyday Money Management

It may not be romantic, but at some point newlyweds need to determine who is going to keep track of and pay all of the household bills. Some divide and conquer, while others elect one partner to deal with the dollars. Either option can work — the key is to have a system in place so bills don’t fall through the cracks.

Most respondents to our survey (72%) have one CFO (chief financial officer) in their marriage, while 28% share money management tasks. More specifically:

57% Have a Prenuptial or Postnuptial Agreement

A growing number of couples are signing legal contracts that spell out how financial assets will be handled in the event of a divorce: Prenups that are signed before marriage, and postnups that are signed after a couple walks down the aisle. Our recent survey of soon-to-be-married couples found that 14% were considering a prenup. In this survey, a full 36% of respondents said they have a prenuptial agreement, while 21% have a postnuptial contract. Another 6% are considering one of these contracts.

Transparency and Communication

Effective communication and trust are the building blocks of any successful partnership. Fortunately, most couples in our survey talk frequently and honestly about money. That said, some partners are holding key financial information back.

91% Talk With Their Spouse About Money at Least Monthly

In general, communicating about finances is a priority for couples in SoFi’s survey. About a third of couples in our poll talk to their partners about money monthly, while 45% discuss money weekly, and 15% converse about financial topics biweekly.

But Some Subjects May Be Off-Limits: 22% Keep Financial Secrets From Their Spouse

While establishing financial boundaries in a marriage is healthy, hiding or lying about financial issues can lead to money fights and breed mistrust over time. The good news is most couples we polled seem to be on the right track — nearly 80% said they rarely or never keep money secrets from their spouse.

However, there is some cause for concern: Roughly 1 in 4 recently married adults report that they sometimes or often keep money secrets from their significant other.

Spending Money After Marriage

Couples today generally know it’s important to be on the same page when it comes to spending vs. saving and wise to set up a household budget. Still, many partners don’t relish the idea of having their mates micromanage their personal spending.

37% of Partners Spend Without Consulting Their Spouse

There are a number of ways to manage discretionary (aka, “fun”) spending in a marriage. Some couples let each partner spend however they want, while keeping an eye on the overall budget. Others choose to consult each other on all nonessential purchases (or purchases above a certain price point). A third option is to allot a set amount of money to each partner that they can spend however they like. You agree on the amount, but not how it’s spent.

When asked how they and their spouse handle discretionary spending, SoFi respondents said:

55% Are Very Comfortable With Their Partner’s Spending

Adults often come into marriage with different money mindsets — for example, you might be a saver, while your spouse loves to spend, spend, spend. These attitudes and habits are often formed during childhood based on how our families handled money and how much financial security we had growing up.

How do our couples align? More than half of respondents (55%) are completely comfortable with their partner’s spending habits, and 36% are somewhat comfortable. However, 10% did admit to some reservations about their spouse’s spending: 7% are somewhat uncomfortable with it, and 3% are very uncomfortable.

43% of Newlyweds Wish They Had Spent More on Their Wedding

Weddings are notoriously expensive (averaging around $33,000). So it’s not surprising most respondents took on debt to pay for their big day. What is: A full 43% said they wish that they had spent more on their big day. Around 30% said they would spend less, and 31% would spend the same.

Dealing With Debt

Managing debt often becomes more complicated — and more expensive — with marriage. Many partners enter into a relationship owing money for things like credit cards, student loans, or car payments. Couples may then take on additional debt together, whether it’s to pay for their wedding or buy a car or a home. Here’s how newlyweds are managing their individual and shared debts.

40% Are Still Paying Off Wedding Debt

Approximately four in 10 survey participants are in the process of repaying the debt they incurred from their wedding. The good news is that many couples pay it all off within the first year of marriage. Among newlyweds polled:

65% Work as a Team to Pay Off Pre-Existing Debt

When it comes to individual debts, SoFi’s Love & Money survey suggests that newlywed couples are generally upfront with each other about what they owe. Three-quarters of respondents said they told their partner about all their debt before they got married, and 19% partially disclosed their debt details. Only 6% kept mum about their outstanding balances.

Here’s how our poll respondents are handling prior debt:

58% Took Out Loans With Their Partner Before Marriage — and Most Plan to Borrow Even More Money

Nearly 60% of respondents had joint loans with their partners before they tied the knot — namely personal loans (28%), car loans (26%), and mortgages (25%). And 84% are planning to take out more together in the near future.

Source: SoFi 2024 Love & Money survey

Planning for a Secure Financial Future

Even though they’ve been married for less than a year, the majority of respondents in SoFi’s Love & Money survey are already looking ahead and working on saving for the future.

65% Have a Shared Emergency Fund

Financial advisors generally advise couples to keep at least six months worth of combined living expenses in a separate bank account, like a high-yield savings account, for unexpected costs. Without any kind of cushion, a financial set-back (like a major home or car repair or loss of income) could force you to run up expensive debt that could take months, even years, to get out from under.

Newlyweds have largely gotten the message: Over half (65%) have already set up a shared emergency savings fund, while 21% are in the process of creating one. Only 14% of the couples in our survey haven’t yet established an emergency fund.

If you’re not sure if you and your partner have enough funds set aside for a rainy day, an online emergency fund calculator to help you crunch the numbers.

37% Have Discussed Planning for Retirement in Detail

According to one guideline called the 80% rule, couples should aim to replace 80% of their income annually when they retire. Considering that retirement can last 30 years or more, this can add up to a significant sum. One way to get there is to start early — this allows your money to grow through compounding (when your returns earn returns of their own).

Fortunately, many couples recognize the value of getting a jumpstart on retirement planning: Forty percent of newly married couples in our poll have had brief discussions about planning for retirement, and 37% have discussed the issue in detail. The remaining 23% say they haven’t discussed it yet.

2 out of 3 Newlyweds Share the Same Risk Investment Risk Tolerance

Many couples invest money for long-term goals (like retirement or a child’s future college education), whether that’s through a 401(k), an individual retirement account (IRA), or a brokerage account. However, they aren’t always on the same page when it comes to balancing risk versus potential reward with their investments.

How aligned were the couples in our survey? Most (67%) believe their risk tolerance is similar to their partner’s, while 27% say their appetite for risk is different than their spouse’s. Six percent aren’t sure.

Talking to your partner about investment goals and the strategies to achieve them can help you determine where each of you stand on risk tolerance. From there, you can figure out a way to bridge any differences.

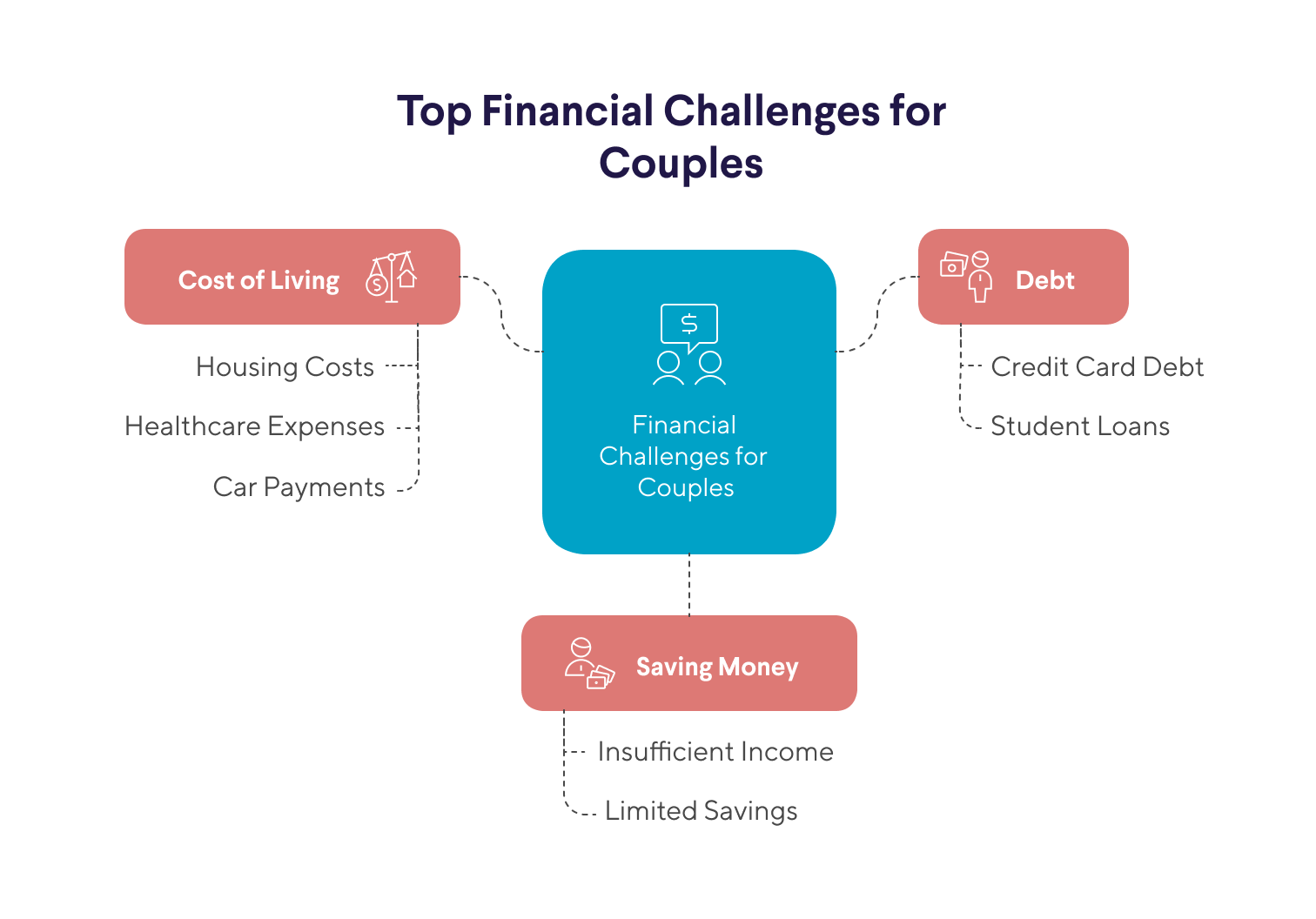

Common Money Challenges Newlyweds Face

When we asked survey respondents to tell us about the largest financial challenge they and their partner are facing, this is what they told us:

• Paying off debt: Credit card debt and loan payments are concerns that came up repeatedly.

• Outstanding student loans: A number of respondents cited student loan debt in particular as a major worry.

• Saving money: There isn’t much left to save after all the bills are paid, survey participants told us. “We just don’t earn enough,” one said, summing up a frustration felt by many.

• Cost of living: High housing costs and the rising cost of living overall are making it hard for couples to get by. We heard similar concerns from our soon-to-be-married couples.

• Affording a car: Trying to make car payments — or earning enough to qualify for a car loan — is challenging, people reported.

• Cost of health care: Medical expenses and paying for health care were problems cited by a number of survey takers. “Rising health care costs are a burden,” a respondent said.

The Takeaway

According to SoFi’s 2024 Love & Money survey, couples who have been married for less than a year typically work as a team to deal with financial issues and work toward their future goals. They tend to talk about money frequently, mostly approve of each other’s spending habits, and many have discussed saving for retirement.

Yet at the same time, they cherish their financial independence. The majority keep at least some of their money separate, have prenuptial or postnuptial agreements with their partners, and section off some of their income to spend as they please.

Couples also face a number of financial challenges, including paying off debt and today’s high cost of living. For many, putting money in the bank for their future goals is a struggle, but also a priority. Choosing the right bank account can be a step in the right direction.

About the Survey

SoFi’s Love & Money Survey was conducted August 16 – September 1, 2024 and included 600 U.S. adults aged 18+ who have been married less than one year.

Percentages were rounded to the nearest whole number so some percentages may not add up to 100%.

Percentages were rounded to the nearest whole number so some percentages may not add up to 100%.

Get better banking with SoFi.

SOBNK-Q125-069

Read more

Love and Money: The Reality of Couples’ Finances Before Marriage

How do couples today handle their finances before getting married? To find out, in August 2024 SoFi surveyed 450 adults who live with their partners (and intend to get married within the next three years) about money, relationships, and plans for the future.

Our results suggest that the majority of committed couples are open with each other about money and debt, are relatively aligned in their financial goals, and plan to talk about money at least monthly after marriage. That said, many have occasional disagreements over money and are worried about expenses, debt, and saving for the future.

Learn how other couples’ financial habits compare to yours, and get tips for dealing with love and money in a relationship.

Key Findings

Some highlights of SoFi’s 2024 Love & Money survey of soon-to-be married couples include:

• More than one-quarter (28%) of survey respondents share a joint bank account with their partner before marriage.

• 75% of partners are very comfortable discussing money matters with their partner.

• 40% of cohabitating couples sometimes disagree about finances.

• Only 14% of those surveyed are considering a prenup.

• Nearly 1 in 5 (18%) of couples have postponed their wedding to save more money.

• 28% of respondents are thinking of postponing their wedding to save money, but they haven’t discussed the idea with their partner.

Financial Transparency Before Marriage

Overall, most couples today aren’t shy about sharing details about their finances. Many have discussed everything from the amount of debt they owe to their credit scores.

75% Are Very Comfortable Discussing Money Before Marriage

Although money issues can be difficult to talk about, discussing finances before marriage can help couples build a solid financial foundation for their future together.

The participants in the SoFi survey seem to be on the right track: Three-quarters said they freely discuss finances with their partner. Another 18% are somewhat comfortable having money talks, while around 6% are either neutral or somewhat uncomfortable. Better yet: Not even one survey respondent said they were very uncomfortable discussing finances with their future fiancé.

About 1 in 3 respondents said they started saving for their golden years between the ages of 25 to 35, while 17% began before age 25. That’s a positive sign, as getting an early start means more time to capitalize on the power of compounding returns. However, roughly 1 in 3 adults said they didn’t start saving until after the age of 36, and 13% said they had yet to put a retirement plan into action.

83% Disclose Their Debt

Transparency about debt is key for couples, particularly if you plan to get married. Being aware of how much combined debt you owe allows you to come up with strategies for paying it down and building financial security. Hiding debt, on the other hand, can lead to distrust in the relationship.

The good news is that the majority of our survey participants (83%) have told their partner about all the debt they owe. Another 14% have partially disclosed their debt, and just 3% haven’t revealed their debt at all.

87% Share Credit Scores

Even credit scores aren’t off limits to SoFi survey respondents. Most (87%) said they’ve told their partner what their credit score is. Only 8% haven’t shared this info, and 5% are planning to bring it up at some point. If you’d like to reveal your score to your partner, but you’re not sure what it is, there are ways to check your credit score for free.

Joint Finances and Future Planning

Many of SoFi’s Love & Money survey respondents are combining their money with their partners’ — even before marriage. Here’s how they’re managing money in their relationship.

28% Have a Joint Bank Account

A joint bank account can make it easier for couples to manage household bills and other shared expenses. That may explain why, even before they tie the knot, nearly 30% of respondents have a joint account with their significant other, and 39% are planning to open an account together.

However, whether to bank together is a highly personal decision, and some couples prefer to keep their money separate. In the SoFi survey, 15% of people said they don’t plan to open a joint account, and 18% said they haven’t talked about the idea yet.

Roughly 1 in 4 committed couples open a joint bank account before marriage.

Recommended: Joint Bank Accounts: What They Are and Pros and Cons

74% Discuss Their Financial Goals

Overwhelmingly, respondents to the survey report that they have discussed their long-term money goals and, in most cases, agree on what those goals are:

Of the 74% who said they’ve discussed long-term goals and are aligned, their top financial objective is buying a home.

85% Plan to Discuss Finances at Least Once a Month After Marriage

When it comes to love and money in a relationship, survey respondents aim to keep the lines of communication open after they get married. Eighty-five percent say they’ll talk about money monthly, while 40% are targeting weekly discussions.

Financial experts agree with this approach: Regular money talks during marriage can help lower financial stress, reinforce that you are both on the same team, and help you work toward — and achieve — shared goals. Together, you may be able to problem-solve your issues, for instance.

76% Want to Learn More About Managing Money Together

It’s one thing to manage finances as a single person, but when you merge money and bills with a partner, the task can become even more complicated. No wonder then that more than three-quarters of SoFi survey respondents said they’re interested in learning more about managing finances as a couple.

Some have already taken the first step: 16% have completed a financial education class with their significant other — even before saying “I do.”

Wedding Finances: How to Pay for the Big Day

A wedding is a huge expense — the average wedding in the U.S. costs $33,000, according to The Knot. For many couples, figuring out how much to spend and how to pay for their wedding day is the one of the first major money issues they may confront together. SoFi’s survey uncovered these intriguing truths about wedding spending.

81% Plan to Use Savings to Pay for Their Wedding

Most couples want to foot at least some of their wedding bill themselves: 81% are aiming to put their savings toward it. But many couples also need financial help from family or plan to borrow the funds to help cover the cost of their big day.

This is how SoFi respondents’ answers break down (they selected all that apply to their situation):

79% Agree About Wedding Spending

Although you might think that wedding expenses could be a source of friction, our survey found that most couples are completely or mostly in agreement about how much money to spend and what to spend it on: 79% of respondents report being in sync about this, with 37% saying they completely agree.

Another 18% are somewhat aligned on wedding spending, while 2% mostly disagree about it and less than 1% completely disagree.

41% Prioritize Saving for Their Future Over Wedding Spending

While a wedding is a milestone day in a couple’s relationship, saving for the future is also very important to respondents of SoFi’s Love & Money survey: A full 41% said putting money away for their future together is a bigger priority than paying for their wedding.

A slightly larger group of respondents (48%) want to balance both wedding expenses and saving for the future. Just 6% prioritize saving for their wedding over saving for their future.

Savings strategies for couples who want to build a nest egg for their future could include opening a high-yield savings account, contributing to a 401(k) at work, and setting up an IRA.

71% Have Discussed How Wedding Debt Might Impact Their Financial Goals

Considering that the cost of a wedding can run well into the tens of thousands of dollars, as noted above, our survey respondents are confronting the issue by talking about it. And almost one in five said they don’t plan to take on wedding debt.

28% Are Considering Postponing Their Wedding to Save More Money

When finances are tight, many respondents to our survey are willing to take action to avoid overspending and running up debt, even if it means putting off their big day. Almost one in five (18%) have already postponed their wedding day after discussing it with their partner. Another 28% report that they’re considering postponing their wedding, though they haven’t talked about the idea with their partner.

For 33% of respondents, postponing is not an option, and 20% have discussed the idea but decided not to put off their wedding.

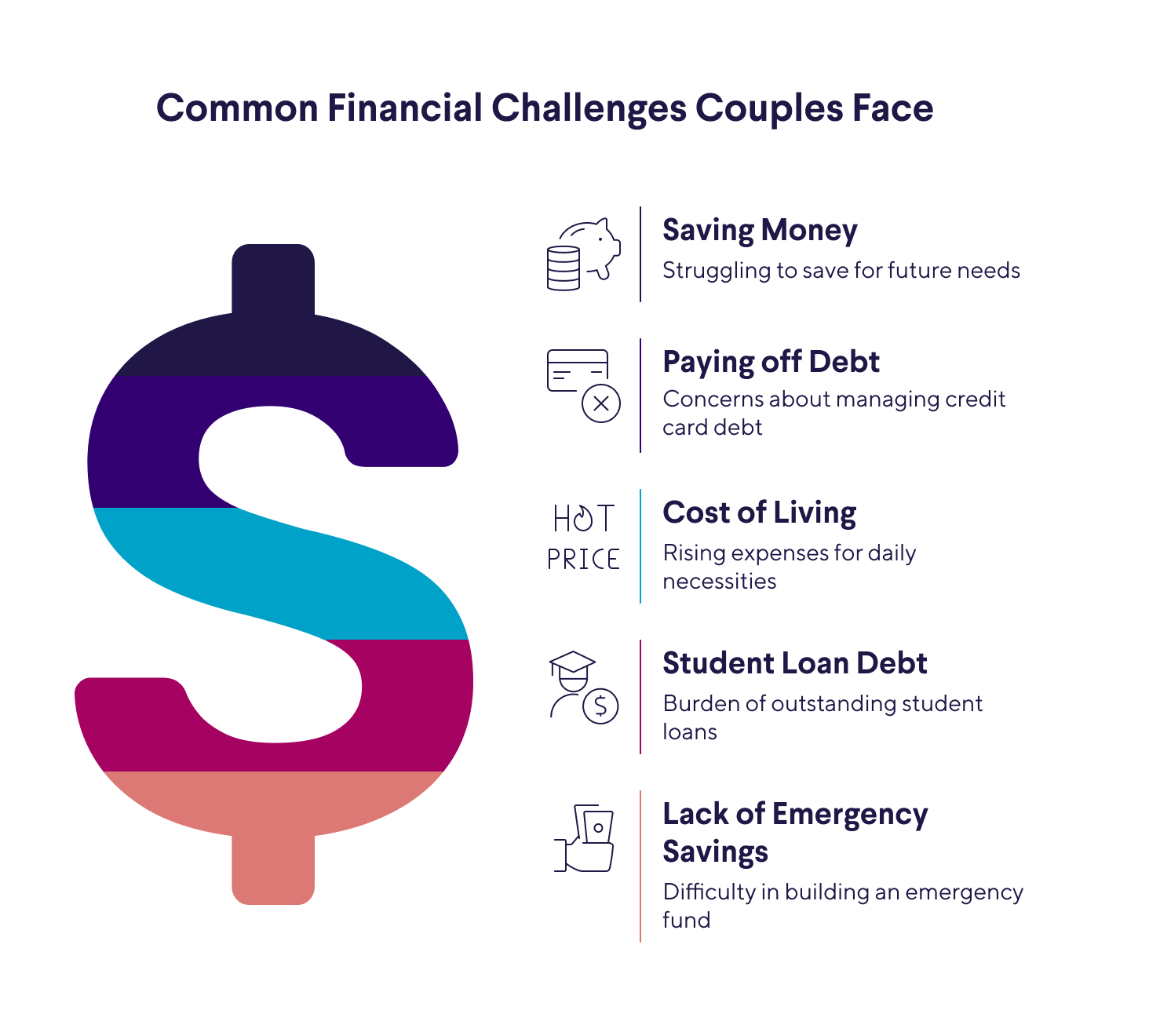

Common Money Challenges Couples Face

When we asked survey respondents to tell us about the largest financial challenge they and their partner are facing, this is what they told us:

• Saving money: Whether it’s for a house, kids, or retirement, putting away money for the future is a struggle for many survey respondents.

• Paying off debt: Tackling credit card debt is a major concern many survey participants voiced.

• Cost of living: From housing to groceries to being able to pay the monthly utility bills, respondents say the cost of everything has gone up. “We live paycheck to paycheck,” several told us.

• Student loan debt: Paying off outstanding student loans weighs heavily on the minds of a number of respondents.

• Lack of emergency savings: Trying to scrape together enough to create an emergency fund came up over and over with respondents.

Conflict and Communication

Numerous studies over the years have found that money is a common reason couples fight. But in SoFi’s 2024 Love & Money survey, just 10% of respondents said they often or very often argue about finances. Let’s call that progress!

41% Rarely Disagree About Money

When asked how often they disagree about financial matters, the top answer was “rarely.”

14% Are Considering a Prenuptial Agreement

Prenups are no longer just for the wealthy. Indeed, research suggests these legal contracts are growing in popularity, particularly among millennials and Gen Zs. Nevertheless, our survey suggests that only a minority of couples are on board with the idea. Among our respondents:

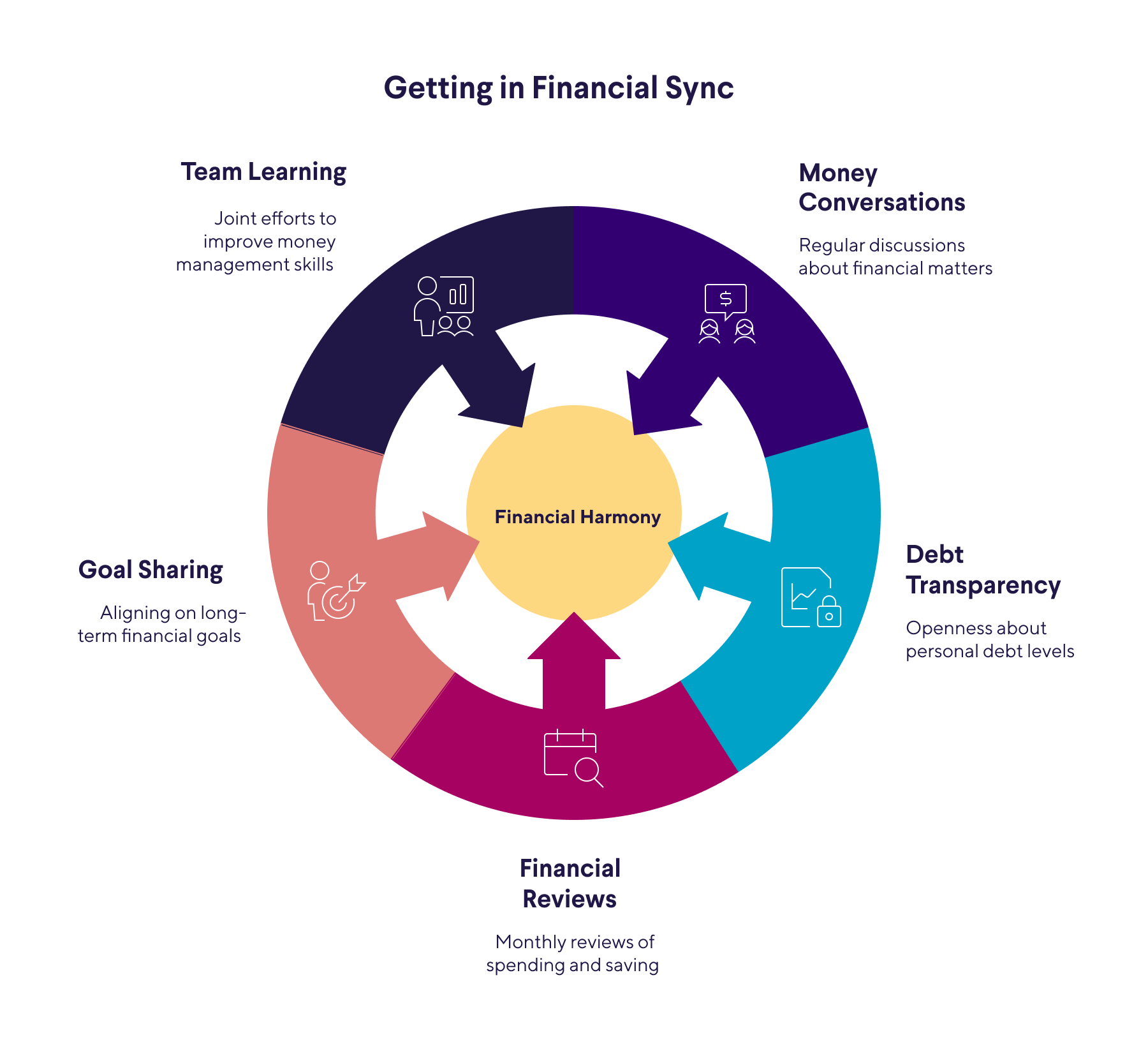

Couples Are Working on Communication

A large share of SoFi survey respondents are practicing helpful techniques to get in sync financially and work toward their goals together. These strategies include:

• Having money conversations. In our research, couples made it clear that they talk about money issues, from credit scores to spending and saving. Three-quarters said they are very comfortable discussing money issues.

• Coming clean about the uncomfortable stuff. 83% of participants have been completely transparent with their partner about the amount of debt they owe.

• Staying on top of spending and saving. Fully 85% plan to review their finances together at least monthly.

• Sharing their goals. Talking about long-term goals and being aligned on them is something 74% of respondents do.

• Working as a team to improve their money skills. 76% percent are eager to learn more about managing money as a couple.

The Takeaway

Overall, couples who live together and plan on getting married are surprisingly in sync about their finances and their savings goals, according to findings from SoFi’s 2024 Love & Money survey.

Three-quarters of respondents are comfortable discussing money matters with their partner, and nearly as many are aligned about their financial goals for the future. The majority of survey participants share the details about the debt they owe and their credit scores. And 41% said they rarely disagree about finances.

However, respondents also acknowledge that they don’t always agree on money issues and struggle with a number of financial challenges, including saving for the future. Opening a joint bank account to save for emergencies and other goals is one way couples can take charge of their finances.

About the Survey

SoFi’s Love & Money Survey was conducted on August 22-23, 2024 and included 450 U.S. adults aged 18+ who were living with their partner, had discussed marriage with their partner, and were likely to get married within the next three years.

Percentages were rounded to the nearest whole number so some percentages may not add up to 100%.

Get better banking with SoFi.

SOBNK-Q125-068

Read moreIs 677 a Good Credit Score?

Is 677 a Good Credit Score?

By Rebecca Lake

Your credit scores tell lenders how likely you are to repay your debts on time. A higher score can make it easier to qualify for loans and credit cards with favorable rates. But what exactly is “good” credit? Is a 677 score good — or bad?

According to the FICO® scoring model, which is the one most commonly used by lenders, a 677 credit score lands in the “good” credit tier (670 to 739). This means you fall right around the middle — below “very good” and “exceptional” credit but above “poor” and “fair” credit.

What can a 677 credit score get you? Here’s a closer look at what it means for your finances.

Key Points

• A 677 credit score is considered “good” in the FICO scoring model but is below average.

• With a 677 score, you can qualify for various credit products but may not get the best interest rates or offers.

• You may qualify for credit cards with limited rewards and no annual fee.

• A 677 score is sufficient to get an auto loan, but you’ll likely pay an above-average interest rate.

• Your score is high enough to qualify for most types of mortgages, including conventional home loans (though not jumbo loans).

What Does a 677 Credit Score Mean?

FICO credit scores are calculated based on information in your credit reports. This information is grouped into five categories and each is weighted differently. Here’s how it breaks down:

• Payment history (how often you pay your bills on time): 35%

• Amounts owed (how much of your available credit you’re using): 30%

• Length of credit history (how long you’ve had credit and the average age of your credit accounts): 10%

• Credit mix (having different types of debt, such as revolving credit and installment loans): 10%

• Credit inquiries (recent applications for new credit): 10%

FICO scores range from 300 to 850 and are grouped into five different tiers:

• 300-579: Poor

• 580-669: Fair

• 670-739: Good

• 740-799: Very Good

• 800-850: Exceptional

Your 677 credit score falls in the “good” credit tier. However, it just makes it, and it’s lower than the average FICO credit score in the U.S., which is 715.

With a 677 score, many lenders will consider you to be an “acceptable” borrower and eligible for a wide range of credit products. However, they likely won’t offer you their lowest-available rates or premium product offers.

What Else Can You Get with a 677 Credit Score?

So is 677 a bad credit score when you need to borrow? Not at all. Here’s what you can expect with different types of lending products, including credit cards, auto loans, mortgages, and personal loans.

Can I Get a Credit Card with a 677 Credit Score?

Yes, a 677 credit score should put you in the path for many unsecured credit cards (which don’t require a deposit to open). However, your “good” credit may not be good enough for a premium credit card that offers generous rewards, travel benefits, or cash-back incentives. You may also be offered a higher-than-average annual percentage rate (APR).

With a 677 score, your credit card options might include:

• 0% APR balance transfer credit cards

• Cards that earn a limited amount of cash back on purchases

• Cards with no annual fee

• Basic travel credit cards that earn points or miles

• Cards that offer a sign-up bonus

• Retail store credit cards

Keep in mind that your credit score isn’t the only thing a lender will look at when you apply for a credit card. They typically also pay close attention to your debt-to-income ratio (DTI), which is the percentage of your gross monthly income that goes toward paying your debts, to make sure you have enough income (and room in your budget) to manage the card’s standard credit line.

Recommended: Personal Lines of Credit vs Credit Cards

Can I Get an Auto Loan with a 677 Credit Score?

Yes, a 677 credit score is generally sufficient to qualify for a car loan. While there’s no set minimum credit score required to get a car loan, your score can have a significant impact on the rate you get. This is generally true for all loans but particularly so with auto loans.

With a 677 score, you’ll probably won’t qualify for the best-available rates. According to a four-quarter 2024 report from Experian®, borrowers with high credit scores (over 780) paid, on average, 4.77% for new cars and 7.67% for used cars. Car buyers with scores between 661 to 780, on the other hand, paid (on average) 6.40% for new car loans and 9.95% for used car loans.

To get the best deal possible on a car loan with a 677 score, it’s a good idea to shop rates with multiple lenders, even before you shop for the vehicle, and compare. Many lenders offer prequalification with a soft credit check, which can give you an idea of the rate you might qualify for without impacting your credit score.

If the rates you’re seeing are higher than you’d like, consider putting down a larger down payment or adding a cosigner. Alternatively, you might wait to purchase a car and take time to build your credit profile before applying for a loan. Steps like paying down existing debt, making timely payments on credit cards, and not submitting any other credit applications, may help you qualify for better rates and terms in the future.

Can I Get a Mortgage with a 677 Credit Score?

A credit score of 677 should be more than enough to qualify for a mortgage loan. A score in this range gives you numerous borrowing options, including:

• Conventional mortgages

• USDA loans (insured by the U.S. Department of Agriculture)

• FHA loans (insured by the Federal Housing Administration)

• VA loans (offered by the U.S. Department of Veterans Affairs to eligible veterans, service members, and surviving spouses)