The current median annual salary for a radiology tech is $67,180 or $32.30 per hour, according to the Bureau of Labor Statistics. This career can be a good option for those who want to work in the medical field but don’t want to attend medical school. This role typically only requires an associate’s degree, so it can be easy to pursue this career without taking on a ton of student loan debt.

For those who wonder how much a radiology tech makes, read on for details and what else you should know about this career and its earning potential.

Check your score with SoFi

Track your credit score for free. Sign up and get $10.*

What Are Radiology Techs?

A radiology technologist, also known as a radiographer, is a healthcare professional responsible for conducting X-rays and other diagnostic imaging procedures on patients. It typically offers a medical career path without a college degree or graduate-level degrees. It therefore can sidestep many additional years of training and the expense of that education.

The key duties of radiology techs include:

• Adjusting and maintaining imaging equipment

• Adhering to precise instructions from physicians regarding the targeted areas of the body for imaging

• Preparing patients for procedures by collecting medical histories and shielding unnecessary exposed areas

• Positioning both the patient and equipment to obtain accurate images

• Operating computerized equipment for image capture

• Collaborating with physicians to assess the images

• Deciding if further imaging is necessary

• Helping to maintain patient records.

If you’re a “people person” who enjoys interacting with patients and colleagues daily, this position could be a good fit. However, as a job for introverts, it may not be enjoyable due to the social aspect.

💡 Quick Tip: We love a good spreadsheet, but not everyone feels the same. An online budget planner can give you the same insight into your budgeting and spending at a glance, without the extra effort.

How Much Do Starting Radiology Techs Make a Year?

When someone is working as an entry-level radiology tech, they can expect to earn less than their more experienced coworkers. The median annual wage for the lowest 10% of earners in this role is less than $47,760.

In terms of how much an experienced radiology tech could make, the highest 10% earn more than $97,940. Being able to earn close to $100,000 is a good salary for a role that only requires an associate’s degree.

What is the Average Salary for a Radiology Tech?

While the median annual wage for a radiology tech is $67,180, where someone lives can greatly impact how much they stand to earn. For example:

• Florida radiology techs can expect to earn an average salary of $66,051.

• Those working in Oregon earn an annual salary of $108,714.

It will give you a detailed look at how earnings vary by state.

What is the Average Radiology Tech Salary by State for 2023

State

Annual Salary

Monthly Pay

Weekly Pay

Hourly Wage

Oregon

$108,714

$9,059

$2,090

$52.27

Alaska

$108,369

$9,030

$2,084

$52.10

North Dakota

$108,210

$9,017

$2,080

$52.02

Massachusetts

$107,274

$8,939

$2,062

$51.57

Hawaii

$105,948

$8,829

$2,037

$50.94

Washington

$104,410

$8,700

$2,007

$50.20

Nevada

$102,464

$8,538

$1,970

$49.26

South Dakota

$102,270

$8,522

$1,966

$49.17

Colorado

$101,476

$8,456

$1,951

$48.79

Rhode Island

$100,695

$8,391

$1,936

$48.41

Mississippi

$98,260

$8,188

$1,889

$47.24

New York

$97,174

$8,097

$1,868

$46.72

Delaware

$95,485

$7,957

$1,836

$45.91

Vermont

$94,853

$7,904

$1,824

$45.60

Virginia

$94,142

$7,845

$1,810

$45.26

Illinois

$93,946

$7,828

$1,806

$45.17

Maryland

$92,483

$7,706

$1,778

$44.46

Kansas

$92,447

$7,703

$1,777

$44.45

Nebraska

$90,537

$7,544

$1,741

$43.53

California

$90,046

$7,503

$1,731

$43.29

Missouri

$89,904

$7,492

$1,728

$43.22

South Carolina

$89,113

$7,426

$1,713

$42.84

Pennsylvania

$89,020

$7,418

$1,711

$42.80

New Jersey

$88,951

$7,412

$1,710

$42.77

Wisconsin

$88,122

$7,343

$1,694

$42.37

Maine

$87,977

$7,331

$1,691

$42.30

Oklahoma

$87,678

$7,306

$1,686

$42.15

North Carolina

$87,273

$7,272

$1,678

$41.96

New Hampshire

$86,552

$7,212

$1,664

$41.61

Idaho

$86,116

$7,176

$1,656

$41.40

Texas

$85,514

$7,126

$1,644

$41.11

Wyoming

$85,210

$7,100

$1,638

$40.97

Minnesota

$85,148

$7,095

$1,637

$40.94

Kentucky

$84,779

$7,064

$1,630

$40.76

New Mexico

$84,632

$7,052

$1,627

$40.69

Indiana

$84,108

$7,009

$1,617

$40.44

Michigan

$84,014

$7,001

$1,615

$40.39

Ohio

$82,756

$6,896

$1,591

$39.79

Arizona

$82,368

$6,864

$1,584

$39.60

Connecticut

$82,133

$6,844

$1,579

$39.49

Iowa

$81,424

$6,785

$1,565

$39.15

Montana

$81,128

$6,760

$1,560

$39.00

Arkansas

$80,164

$6,680

$1,541

$38.54

Alabama

$80,115

$6,676

$1,540

$38.52

Utah

$79,081

$6,590

$1,520

$38.02

Tennessee

$79,008

$6,584

$1,519

$37.98

Georgia

$74,633

$6,219

$1,435

$35.88

Louisiana

$74,343

$6,195

$1,429

$35.74

West Virginia

$68,751

$5,729

$1,322

$33.05

Florida

$66,051

$5,504

$1,270

$31.76

Source: ZipRecruiter

Radiology Tech Job Considerations for Pay & Benefits

Most radiologic and MRI technologists work full time. Because imaging is sometimes needed in emergency situations, some technologists work evenings, weekends, or overnight.

Almost six out of 10 radiology techs work in hospitals; about 20% work in medical offices. One thing to note is that, as you would expect, the job involves working with potentially dangerous radiation, so appropriate protective clothing may be worn and safety practices followed.

Because radiology techs stand to earn a solid income without having to pursue higher education, there aren’t any real disadvantages to their salary. The main disadvantage of the job though is being exposed to infectious diseases through patient interaction and equipment that uses radiation. Safety procedures are in place to help offset these risks, but some people may not find the salary worth it in light of the risks.

Benefits will of course vary depending on where a radiology tech works. Packages may include health insurance, paid sick days and vacations, retirement account matching contributions, and more.

Working as a radiology tech can be a great way to earn a living in the medical field without having to commit to the major time and expense that comes with pursuing careers like nursing or becoming a doctor. It can offer a solid salary, benefits, and the satisfying work of helping people with their health care.

With SoFi, you can keep tabs on how your money comes and goes.

FAQ

Can you make 100k a year as a radiology tech?

It is possible to earn $100,000 a year as a radiology tech but being able to do so depends on what state someone works in, as well as other factors like experience. For example, the average annual salary of a radiologist tech in Oregon, Alaska, and North Dakota is well over $100,000.

Do people like being a radiology tech?

Being a radiology tech can be very enjoyable if someone finds the work interesting and if they enjoy interacting with patients. However, for those who don’t like being in a health care setting, repeating procedures, or working with potentially dangerous radiation, it may not be a good fit.

Is it hard to get hired as a radiology tech?

Those who want to work as a radiology tech and who have the required credentials should have no problem doing so. The job outlook for radiology techs is positive with a projected 6% growth from 2022 to 2032, which is faster than the average for all occupations. Each year, approximately 15,700 job openings for this role are expected to be available.

About the author

Jacqueline DeMarco

Jacqueline DeMarco is a freelance writer who specializes in financial topics. Her first job out of college was in the financial industry, and it was there she gained a passion for helping others understand tricky financial topics. Read full bio.

Photo credit: iStock/monkeybusinessimages

SoFi Relay offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. Based on your consent SoFi will also automatically provide some financial data received from the credit bureau for your visibility, without the need of you connecting additional accounts. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

*Terms and conditions apply. This offer is only available to new SoFi users without existing SoFi accounts. It is non-transferable. One offer per person. To receive the rewards points offer, you must successfully complete setting up Credit Score Monitoring. Rewards points may only be redeemed towards active SoFi accounts, such as your SoFi Checking or Savings account, subject to program terms that may be found here: SoFi Member Rewards Terms and Conditions. SoFi reserves the right to modify or discontinue this offer at any time without notice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Bank reserves refer to the amount of funds a financial institution must have on-hand at any given time. These reserves are a percentage of its total deposits set aside to fulfill withdrawal requests, and comply with regulations and can also provide a layer of trust for account holders.

Bank reserves act as assurance to depositors that there is always a certain amount of cash on deposit, so the scenario mentioned above doesn’t happen. No one wants to ever withdraw some cash and be left empty-handed. As a consumer with a bank account, it can be important to understand the role bank reserves play in the financial system and the economy.

What Are Bank Reserves?

Bank reserves are the minimum deposits held by a financial institution. The central bank of each country decides what these minimum amounts must be. For example, in the United States, the Federal Reserve determines all bank reserve requirements for U.S. financial institutions. In India, as you might guess, the Reserve Bank of India determines the bank reserves for that country’s financial institutions.

The bank reserve requirements are in place to ensure the financial institution has enough cash to meet financial obligations such as consumer withdrawals. It also ensures that financial institutions can weather historical market volatility (that is, economic ups and downs).

Bank reserve requirements are typically a percentage of the total bank deposit amounts determined by the Federal Reserve Board of Governors. Financial institutions can hold their cash reserves in a vault on their property, with the regional Federal Reserve Bank, or a combination of both. This way, the financial insulation will have enough accessible funds to support their operational needs while letting the remaining reserves earn interest at a Federal Reserve Bank.

💡 Quick Tip: Most savings accounts only earn a fraction of a percentage in interest. Not at SoFi. Our high-yield savings account can help you make meaningful progress towards your financial goals.

How Do Bank Reserves Work?

Bank reserves work to ensure that a certain amount of cash, or percentage of overall deposits, is kept in a financial institution’s vault.

Suppose you need to withdraw $5,000 to purchase a new car. You understand savings account withdrawal limits at your bank and the amount you need is within the guidelines, so you head to your local branch. When you arrive, you’re told they don’t have enough money in their vault to meet your request.

This is what life could be like without bank reserves. The thought of not being able to withdraw your own money might be upsetting, worrisome, and deeply inconvenient. To prevent this kind of situation is exactly why banks must have a certain percentage of cash on hand.

In addition to ensuring consumers have access to their money, bank reserves may also aid in keeping the economy functioning efficiently. For example, suppose a bank has $10 million in deposits, and the Federal Reserve requires 3% liquidity. In this case, the bank will need to keep $300,000 in its vault, but it can lend the remaining $9.7 million to other consumers via loans or mortgages. Consumers can use this money to buy homes and cars or even send their children to college. The interest on those loans is a way that the bank earns money and stays in business.

Bank reserves are vital in helping the economy control money supply, interest rates, and the implementation of what is known as monetary policy. When the reserve requirements change, it says a lot about the economy’s direction. For example, when reserve requirements are low, banks have more opportunity to lend since more capital is at their disposal. Thus, when the money supply is plentiful, interest rates decrease. Conversely, when reserve requirements are high, less money circulates, and interest rates rise.

During inflationary periods, the Federal Reserve may increase reserved requirements to ensure the economy doesn’t combust. Essentially, by decreasing the money supply and increasing interest rates, it can slow down the rate of investments.

There are two types of bank reserves: required reserves and excess reserves. The required reserves are the percentage of deposits the institution must have in cash holdings and deposit balances to abide by the regulations of the Federal Reserve. Excess reserves are the amount over the required reserve amount that the institution holds.

Excess reserves can provide a larger safety net for the financial institution and enhance liquidity. It can also contribute to a higher credit rating for institutions. On the other hand, excess reserves can also result in losing the opportunity to invest the funds to yield higher returns. In other words, since the extra money is sitting in cash, it will not generate the same returns it might yield by lending or investing in the market.

Increase your savings with a limited-time APY boost.*

*Earn up to 4.00% Annual Percentage Yield (APY) on SoFi Savings with a 0.70% APY Boost (added to the 3.30% APY as of 12/23/25) for up to 6 months. Open a new SoFi Checking and Savings account and pay the $10 SoFi Plus subscription every 30 days OR receive eligible direct deposits OR qualifying deposits of $5,000 every 31 days by 3/30/26. Rates variable, subject to change. Terms apply here. SoFi Bank, N.A. Member FDIC.

History of Bank Reserves

Reserve requirements first came about in 1863 during the passing of the National Bank Act. This act intended to create a national banking system and currency so money could flow easily throughout the country. At this time, banks had to hold at least 25% reserves of both loans and deposits. Bank reserves were necessary to ensure financial institutions had liquidity and money could continue circulating freely throughout the nation.

But despite the efforts to establish a robust banking system, banking troubles continued. After the panic of 1907, the government intervened, and in 1913, Congress passed the Federal Reserve Act to address banking turmoil. The central bank was created to balance competing interests and foster a healthy banking system.

Initially, the Federal Reserve acted as a last resort and a liquidity grantor when the banks faced trouble. During the 1920s, the Federal Reserve’s role expanded to playing a proactive role in the economy by influencing the credit conditions of the nation.

After the Great Depression, a landmark in the history of U.S. recessions and depressions, the Banking Act of 1935 was passed to reform the structure of the Federal Reserve once again. As part of this act, the Federal Open Market Committee (FOMC) was born to oversee all monetary policy.

💡 Quick Tip: Don’t think too hard about your money. Automate your budgeting, saving, and spending with SoFi’s seamless and secure mobile banking app.

How the 2008 Crisis Impacted Bank Reserves

Prior to the global financial crisis of 2008, financial institutions didn’t earn interest on excess reserves held at a Federal Reserve Bank. However, after October 2008, the Federal Reserve was granted the right to pay interest to banks with excess reserves. This encourages banks to keep more of their reserves. The Board of Governors establishes the interest on reserve balances (IORB rate). As of July 2024, the IORB was 5.4%.

Then, after the recession subsided in 2009, the Federal Reserve turned its attention to reform to avoid similar economic disasters in the future.

Reserve requirements vary depending on the size of the financial institution. As of July 2024, reserve requirements are 0%, where they’ve been since early 2020 and the onset of the COVID-19 pandemic.

Prior to this revision, banks with between $16.9 to $127.5 million in deposits were required to have 3% in reserves, whereas banks over this amount had to have at least 10% in bank reserves.

Bank reserve requirements aside, financial institutions want to ensure they have enough liquidity to satisfy the short-term financial obligations if an economic crisis occurs. This way, they know they will be able to weather a crisis and not face complete bankruptcy. Therefore, financial institutions use the Liquidity Coverage Ratio (LCR) to prevent financial devastation resulting from a crisis.

The LCR helps financial institutions decide how much money they should have based on their assets and liabilities. To calculate the LCR, banks use the following formula:

(Liquid Assets / Total Cash Outflows) X 100 = LCR

Liquid assets can include cash and liquid assets that convert to cash within five business days. Cash flows include interbank loans, deposits, and 90-day maturity bonds.

The minimum LCR should be 100% or 1:1, though this can be hard to achieve. If the LCR is noticeably lower than this amount, the bank may have liquidity concerns and put the bank’s assets at risk.

The Takeaway

Financial institutions must have a certain amount of cash on hand, referred to as bank reserves. These assets are usually kept in a vault on the bank’s property or with a regional Federal Reserve Bank. These cash reserves ensure financial institutions can support consumer withdrawals and withstand a financial crisis.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with eligible direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with SoFi, NerdWallet’s 2024 winner for Best Checking Account Overall.* Enjoy 3.30% APY on SoFi Checking and Savings with eligible direct deposit.

FAQ

Are bank reserves assets or liabilities?

Bank reserves are considered an asset since they’re an item the bank owns. Other bank assets can include loans and securities.

How are bank reserves calculated?

Bank reserve requirements are calculated as a percentage of the institution’s deposits. So, if the reserve requirement is 3% for banks with $10 million in deposits, the bank would have to hold $300,000 in its reserves.

Where do banks keep their reserves?

Financial institutions usually keep a certain amount of their cash reserves in a vault to meet operational needs. The remaining amount may be kept at Federal Reserve Banks so the balance can generate interest.

About the author

Ashley Kilroy

Ashley Kilroy is a seasoned personal finance writer with 15 years of experience simplifying complex concepts for individuals seeking financial security. Her expertise has shined through in well-known publications like Rolling Stone, Forbes, SmartAsset, and Money Talks News. Read full bio.

Photo credit: iStock/Diy13

Annual percentage yield (APY) is variable and subject to change at any time. Rates are current as of 12/23/25. There is no minimum balance requirement. Fees may reduce earnings. Additional rates and information can be found at https://www.sofi.com/legal/banking-rate-sheet

Eligible Direct Deposit means a recurring deposit of regular income to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government benefit payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Eligible Direct Deposit”) via the Automated Clearing House (“ACH”) Network every 31 calendar days.

Although we do our best to recognize all Eligible Direct Deposits, a small number of employers, payroll providers, benefits providers, or government agencies do not designate payments as direct deposit. To ensure you're earning the APY for account holders with Eligible Direct Deposit, we encourage you to check your APY Details page the day after your Eligible Direct Deposit posts to your SoFi account. If your APY is not showing as the APY for account holders with Eligible Direct Deposit, contact us at 855-456-7634 with the details of your Eligible Direct Deposit. As long as SoFi Bank can validate those details, you will start earning the APY for account holders with Eligible Direct Deposit from the date you contact SoFi for the next 31 calendar days. You will also be eligible for the APY for account holders with Eligible Direct Deposit on future Eligible Direct Deposits, as long as SoFi Bank can validate them.

Deposits that are not from an employer, payroll, or benefits provider or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, Wise, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, or are non-recurring in nature (e.g., IRS tax refunds), do not constitute Eligible Direct Deposit activity. There is no minimum Eligible Direct Deposit amount required to qualify for the stated interest rate. SoFi Bank shall, in its sole discretion, assess each account holder's Eligible Direct Deposit activity to determine the applicability of rates and may request additional documentation for verification of eligibility.

See additional details at https://www.sofi.com/legal/banking-rate-sheet.

SoFi Checking and Savings is offered through SoFi Bank, N.A. Member FDIC. The SoFi® Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

*Awards or rankings from NerdWallet are not indicative of future success or results. This award and its ratings are independently determined and awarded by their respective publications.

Student loans, like any loans, have an interest rate. While interest rate accrual on existing federal student loans was paused for more than three years due to the Covid-19 forbearance, interest accrual resumed on September 1, 2023, and payments resumed in October 2023. And of course, any new student loans — federal or private — will have an interest rate that impacts the total cost of the loan.

So what is the average student loan interest rate? In this guide, we’ll look at the interest rates of new federal student loans, as well as the range of rates for private student loans.

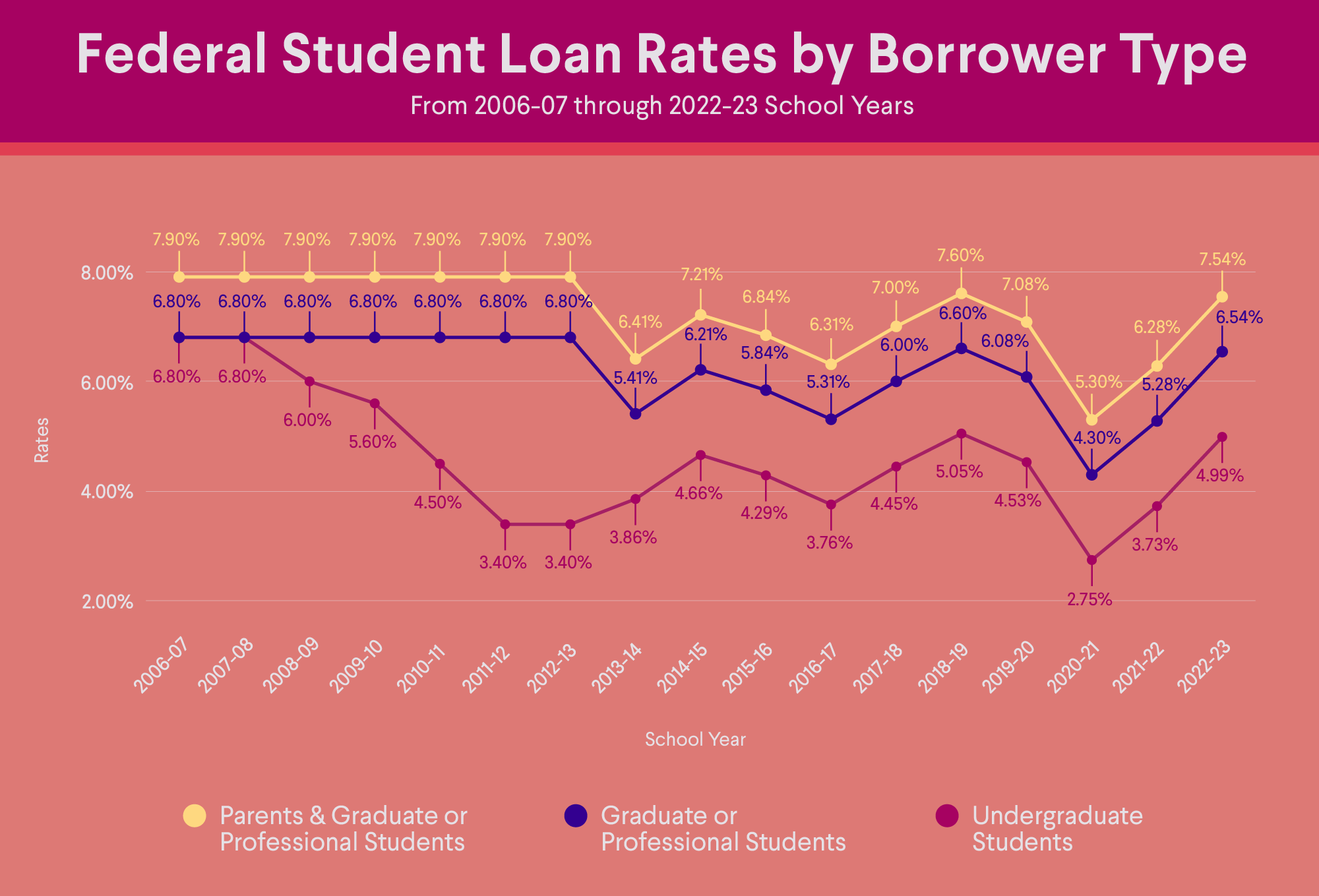

• Federal student loan interest rates for 2024-25 are 6.53% for undergraduates, 8.08% for graduate students, and 9.08% for PLUS loans.

• Private student loan interest rates range from 3.50% to 17.00% as of March 2025.

• Federal interest rates are fixed rates that are set annually using formulas tied to the 10-year Treasury note and a statutory add-on percentage.

• Lenders set their own rates for private student loans. The interest rate on these loans may be fixed or variable.

• Interest rates for federal loans have increased from the previous year, while private loans have a wide range of rates influenced by market conditions.

What Is The Average Student Loan Interest Rate?

The interest rate on a student loan varies based on the type of student loan. Federal student loans issued after July 1, 2006, have a fixed interest rate. The rates on newly disbursed federal student loans are determined annually by formulas specified in the Higher Education Act of 1965 (HEA).

These are the federal student loan interest rates for the 2024–25 school year:

• 6.53% for Direct Subsidized or Unsubsidized loans for undergraduates

• 8.08% for Direct Unsubsidized loans for graduate and professional students

• 9.08% for Direct PLUS loans for graduate students, professional students, and parents

All three of those rates have risen from the 2023-2024 school year, and the undergraduate rate has more than doubled since the 2020-2021 school year.

Source: Studentaid.gov

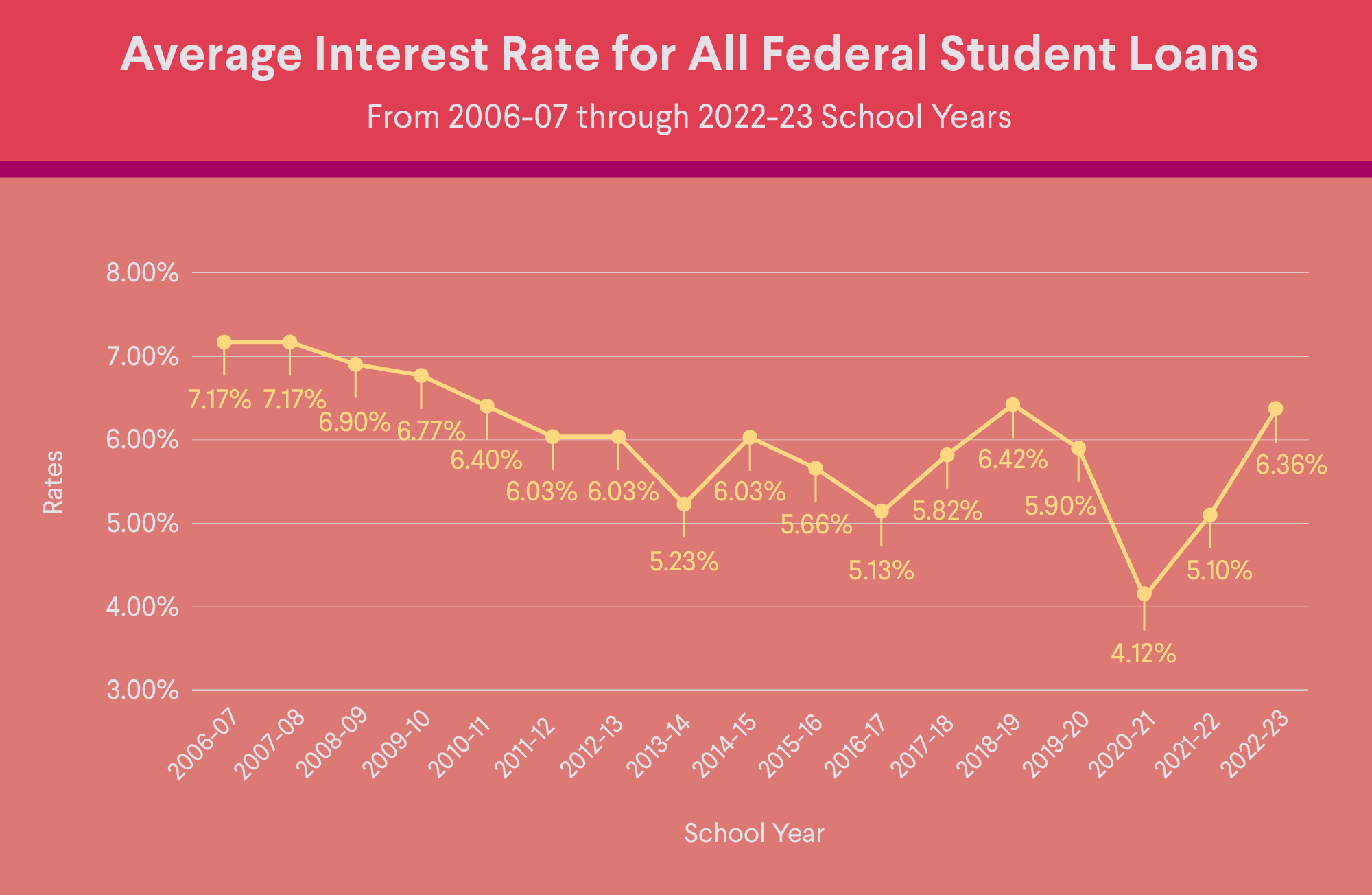

This means that the average student loan interest rate for the three main types of federal student loans is 7.89%.

Source: Studentaid.gov

Private student loan interest rates vary by lender and each has its own criteria for which rates borrowers qualify for. Private student loans can have either fixed interest rates that remain the same over the life of the loan, or variable rates that may start lower than a fixed interest rate but then go up over time, based on market changes.

Private loans require a credit check, and lenders may offer different interest rates if you have strong credit or a cosigner on your student loan. The interest rates on private student loans can vary anywhere from 3.50% to 17.00% (as of March 2025), depending on the lender, the type of loan, and on individual financial factors including the borrower’s credit history.

As mentioned, the interest rates on federal student loans are set annually by formulas specified in the HEA. The rates are tied to the financial markets — federal law sets them based on the 10-year Treasury note and a statutory add-on percentage with a maximum rate cap.

Since July 2006, all federal student loans have fixed interest rates. Although federal student loans are serviced by private companies or nonprofits selected by the federal government, these loan servicers have no say in the federal interest rate offered.

For private student loans, the lenders set their own rates, though they often take cues from federal rates. The rates quoted for student loans vary based on each applicant’s individual situation — though generally the better a potential borrower’s credit history is, the better rate they may be able to qualify for.

How Student Loan Interest is Calculated and Applied

Interest on federal student loans typically accrues daily. To calculate the interest as it accrues, the following formula can be used:

Interest amount = (outstanding student loan principal balance × interest rate factor) × days since last payment

In other words, you will multiply your outstanding loan balance by the interest rate factor, which is used to calculate the amount of interest that accrues on a student loan. Then, multiply that result by the days since you last made a payment.

To calculate the interest rate factor you can divide the interest rate by the number of days of the year (365). For example, let’s say you have an outstanding student loan balance of $10,000, an interest rate of 4.75%, and it’s been 30 days since your last payment. Here’s how to calculate your interest:

$10,000 x (4.75%/365) = $1.30 daily interest charge

$1.30 x 30 days = $39

Interest amount $39

Many private student loans will also accrue interest on a daily basis; however, the terms will ultimately be determined by the lender. Review the lending agreement to confirm.

When you take out a federal student loan, you’ll receive a fixed interest rate. This means that you’ll pay a set amount for the term of the student loan. In addition, all of the terms, conditions, and benefits are determined by the government. Federal student loans also provide some additional perks that you may not find with private lenders, like deferment.

Private student loans can have higher interest rates and potentially fewer perks than federal student loans. You may want to take advantage of all federal student loans you qualify for before comparing private loan options.

One thing to keep in mind is that interest you pay on student loans may allow you to take the student loan interest deduction on your taxes.

What Is a Good Fixed Interest Rate for Student Loans?

The lower the interest rate, the less a borrower will owe over the life of the loan, which could help individuals as they work on other financial goals. If you’re taking out federal loans, the student loan interest rate is set by federal law, so you don’t have a choice for what is and isn’t a reasonable interest rate.

When it comes to private student loans, it’s wise to shop around and compare your options to find the most suitable financing solution. Since every lender offers different terms, rates, and fees, getting quotes from multiple lenders may help you select the best option for your personal needs. Keep in mind that the rate you receive on a private student loan is largely dependent on your credit score and other factors, whereas federal student loan interest rates are based on HEA formulas.

Also keep in mind that private student loans do not have the same borrower protections as federal student loans, including deferment options, and should be considered only after all federal aid options have been exhausted.

Ways to Lower Your Student Loan Interest Rate

The interest rate on federal student loans, while fixed for the life of the loan, does fluctuate over time. For example, the rates for Direct Subsidized and Unsubsidized loans for undergraduates more than doubled from 2.75% in 2020–21 to 6.53% in 2024–25.

To adjust the rate on an existing student loan, borrowers generally have two options. They can refinance student loans or consolidate them with hopes of qualifying for a lower interest rate.

Refinancing a federal loan with a private lender eliminates them from federal borrower protections such as federal deferment or Public Service Loan Forgiveness. The federal government does offer a Direct Consolidation Loan, which allows borrowers to consolidate their federal loans into a single loan. This will maintain the federal borrower protections but won’t necessarily lower the interest rate. When federal loans are consolidated into a Direct Consolidation Loan, the new interest rate is a weighted average of your original federal student loans’ rates.

Refinancing student loans with a private lender may allow qualifying borrowers to secure a lower interest rate or preferable loan terms. Note that extending the repayment term will generally result in an increased cost over the life of the loan.

💡 Quick Tip: Refinancing comes with a lot of specific terms. If you want a quick refresher, the Student Loan Refinancing Glossary can help you understand the essentials.

Fixed vs. Variable Interest Rates: Which Is Better?

Whether fixed or variable interest rates are better depends on a borrower’s specific situation. For many borrowers, fixed rates are often a better option because they are stable and predictable. Your payments won’t change, and you won’t have to worry about rate hikes. Borrowers may want to consider a student loan with a fixed interest rate if interest rates are rising overall and they anticipate needing a number of years to repay their loan.

Because variable interest rates fluctuate with the market, they can be unpredictable. That means your payments can potentially change from one month to the next.

The Takeaway

The average student loan interest rate varies depending on the loan type. The interest rate for federal Direct Unsubsidized and Subsidized loans is set annually by federal law and fixed for the life of the loan.

The interest rate on private student loans is determined by a variety of factors including the borrower’s credit history and may range anywhere from 3.50% to to 17%.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

With SoFi, refinancing is fast, easy, and all online. We offer competitive fixed and variable rates.

FAQ

How often do student loan interest rates change?

The rates on federal student loans are determined and set annually by formulas specified in the Higher Education Act of 1965. Private student loan rates vary by lender, and they may be fixed or variable. Private loans with variable rates can change based on market changes.

How do federal student loan interest rates compare to private loans?

The interest rate on federal student loans is often lower than the rates for private student loans. The rate you may qualify for with a private loan depends on your circumstances. If you have strong credit or a loan cosigner who has strong credit, you may be able to get a loan with a lower interest rate.

Keep in mind that federal student loans have fixed interest rates, which means the interest and your monthly payment won’t change. Private student loans may have fixed or variable rates, and variable rates can go up or down with market changes.

Can I negotiate my student loan interest rate?

Federal student loans have fixed rates that are non-negotiable. With a private student loan, it’s possible that you may be able to negotiate the interest rate, especially if you are struggling to make payments or dealing with financial hardship. Call your private lender and explain the situation.

What factors determine my student loan interest rate?

Federal student loans have a fixed interest rate that is determined and set each year based on formulas specified in the Higher Education Act of 1965. With private student loans, each lender sets their own rates. Private loans require a credit check, and the interest rates vary based on an applicant’s credit and other factors. Generally speaking, the stronger a borrower’s credit is (or if they have a loan cosigner with strong credit), the lower the rate they may be able to qualify for.

Is it better to choose a fixed or variable interest rate for student loans?

For many borrowers, fixed rates may be a better option because they are stable and predictable, which means the monthly payments won’t change over the life of the loan. If you are planning to repay your loan over a period of years, you may want to consider a student loan with a fixed interest rate.

Variable interest rates fluctuate with the market, which makes them unpredictable. As a result, your payments can go up (or down), and may be harder to budget for.

About the author

Ashley Kilroy

Ashley Kilroy is a seasoned personal finance writer with 15 years of experience simplifying complex concepts for individuals seeking financial security. Her expertise has shined through in well-known publications like Rolling Stone, Forbes, SmartAsset, and Money Talks News. Read full bio.

SoFi Student Loan Refinance Terms and conditions apply. SoFi Refinance Student Loans are private loans. When you refinance federal loans with a SoFi loan, YOU FORFEIT YOUR ELIGIBILITY FOR ALL FEDERAL LOAN BENEFITS, including all flexible federal repayment and forgiveness options that are or may become available to federal student loan borrowers including, but not limited to: Public Service Loan Forgiveness (PSLF), Income-Based Repayment, Income-Contingent Repayment, extended repayment plans, PAYE or SAVE. Lowest rates reserved for the most creditworthy borrowers. Learn more at SoFi.com/eligibility. SoFi Refinance Student Loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

The average cost of college in the U.S. is $38,270 per year, including books, supplies, and daily living expenses, according to the Education Data Initiative. While grants and scholarships can significantly lower your out-of-pocket expenses, they typically don’t cover the full cost of your college education.

Student loans, both federal and private, can help bridge this gap in financial aid to allow you to attend the college of your choice. Federal student loans are funded by the government. They tend to offer the best rates and terms, but come with borrowing limits. If you still have gaps in funding, you can turn to private student loans.

Private student loans are funded by banks, credit unions, and online lenders. Private lenders set their own eligibility criteria, and interest rates generally depend on a borrower’s creditworthiness. While private student loans don’t offer all the same borrower protections as federal loans, they can still be a smart choice to help you pay for educational expenses, as long as you do your research.

This guide offers private student loan basics, including what they are, how they work, their pros and cons, and how to apply for one.

Key Points

• Private student loans are offered by banks, credit unions, and online lenders. They are a funding option for students after federal student loans have been exhausted.

• Approval for private student loans typically depends on the borrower’s creditworthiness; students may need a cosigner due to limited credit history.

• Private loans may lack flexible repayment plans and protections that federal loans offer.

• Funds are usually sent directly to the educational institution to cover tuition and fees; any remaining amount is disbursed to the student.

• It’s essential to thoroughly research and compare private loan options, considering factors like interest rates, repayment terms, and borrower protections, before making a decision.

What are Private Student Loans?

Often when people talk about student loans, they’re referring to federal student loans, which are provided by the federal government. Private student loans, by contrast, are funded by banks, credit unions, and online lenders. Students typically turn to private student loans when federal loans won’t cover all of their costs.

You can use the money from a private school loan to pay for expenses like tuition, fees, housing, books, and supplies. Interest rates for private student loans may be variable or fixed and are set by the lender. Repayment terms can be anywhere from five to 20 years.

Unlike federal student loans, borrowers must pass a credit check to qualify for private student loans. Since most college students don’t have enough credit history to take out a large loan, a cosigner is often required.

💡 Quick Tip: New to private student loans? Visit the Private Student Loans Glossary to get familiar with key terms you will see during the process.

How Do Private Student Loans Work?

Loan amounts, interest rates, repayment terms, and eligibility requirements for undergraduate private student loans vary by individual lender. If you’re in the market for a private student loan, it’s key to shop around and compare your options to find the best fit.

To get a private student loan, you need to file an application directly with your lender of choice. Based on the information you submit, the lender will determine whether or not you are approved and, if so, what rates and terms you qualify for.

If you’re approved, the loan proceeds will typically be disbursed directly to your university. Your school will apply that money to tuition, fees, room and board, and any other necessary expenses. If there are funds left over, the money will be given to you to use toward other education-related expenses, such as textbooks and supplies.

Repayment policies vary by lender, but typically you aren’t required to make payments while you’re attending school. Some lenders will allow you to defer payments until six months after you graduate. However, interest typically begins accruing as soon as the loan is dispersed. Similar to unsubsidized federal student loans, the interest that accrues while you’re in school is added to your loan balance.

The Pros and Cons of Private Student Loans

Pros of Private Student Loans

Cons of Private Student Loans

Apply any time of the year

May require a cosigner

Higher loan amounts

Less flexible repayment options

Choice of fixed or variable rates

No loan forgiveness programs

Quick application process

Can lead to over-borrowing

Options for international students

No federal subsidy

If federal financial aid — including grants, work-study, and federal student loans — isn’t enough to cover the full cost of college, private student loans can fill in any gaps. Just keep in mind that private student loans don’t offer the same borrower protections that come with federal student loans. Before taking out a private student loan, it’s a good idea to fully understand their pros and cons.

The Benefits of Private Student Loans

Here’s a look at some of the advantages that come with private student loans.

Apply Any Time of the Year

Unlike federal student loans, which have application deadlines, you can apply for private student loans any time of the year. As a result, they can be helpful if you’re facing a mid-year funding shortfall or if your college expenses go up unexpectedly.

Higher Loan Amounts

Federal loans have annual maximums. For example, a first-year, dependent undergraduate can borrow up to $5,500 for that year. The aggregate max a dependent student can borrow from the government for their entire undergraduate education is $31,000. Private student loan limits vary with each lender, but you can typically borrow up to the full cost of attendance, minus any financial aid received.

Choice of Fixed or Variable Interest Rates

Federal loans only offer fixed-rate loans, while private lenders usually give you a choice between fixed or variable interest rates. Fixed rates remain the same over the life of the loans, whereas variable rates can change throughout the loan term, depending on benchmark rates.

Variable-rate loans usually have lower starting interest rates than fixed-rate loans. If you can afford to pay off your student loans quickly, you might pay less interest with a variable-rate loan from a private lender than a fixed-rate federal loan.

Quick Application Process

While federal student loans require borrowers to fill out the Free Application for Federal Student Aid, or FAFSA, private student loans do not. You can apply for most private student loans online in just a few minutes without providing nearly as much information.

In some cases, you can get a lending decision within 72 hours. By comparison, it typically takes one to three days for the government to process the FAFSA if you submit electronically, and seven to 10 days if you mail in the form.

Options for International Students

While you never want to default on your student loans (since it can cause significant damage to your credit), it can be nice to know that private student loans come with a statute of limitations. This is a set period of time that lenders have to take you to court to recoup the debt after you default. The time frame varies by state, but it can range anywhere from three to 10 years. After that period ends, lenders have limited options to collect from you.

However, that’s not the case with federal student loans. You must eventually repay your loans, and the government can even garnish your wages and tax refunds until you do.

Options for International Students

International students typically don’t qualify for federal financial aid, including federal student loans. Some private lenders, however, will provide student loans to non-U.S. citizens who meet specific criteria, such as attending an eligible college on at least a half-time basis, having a valid student visa, and/or adding a U.S. citizen as a cosigner.

When we say no fees required we mean it.

No late fees when you take out a student loan with SoFi.

The Disadvantages of Private Student Loans

Private student loans also have some downsides. Here are some to keep in mind.

May Require a Cosigner

Most high school and college students don’t make enough income or have a strong credit history to qualify for private student loans on their own. Though some lenders will take grades and income potential into consideration, most students need a cosigner to qualify for a private student loan. Your cosigner is legally responsible for your student debt, and any missed payments can negatively affect their credit. If you can’t repay your loans, your cosigner is responsible for the entire amount.

The good news is that some private student loans allow for a cosigner release.That means that after you make a certain number of on-time payments, you can apply to have the cosigner removed from the loan.

Less Flexible Repayment Options

Federal student loans offer several different types of repayment plans, including income-driven repayment (IDR) plans, which calculate your monthly payment as a percentage of your income.

With private student loans, on the other hand, usually the only way to reduce your monthly payment is to refinance the loan to a lower interest rate, a longer repayment term, or both. Keep in mind that by lowering your monthly payment via a longer repayment period, you’ll typically end up paying more in interest over the life of the loan.

No Loan Forgiveness Programs

Federal student loans come with a few different forgiveness programs, including Public Service Loan Forgiveness (PSLF) and Teacher Loan Forgiveness. While these programs have strict eligibility requirements, they can help many low-income borrowers. Private lenders, on the other hand, generally don’t offer programs that forgive your debt after meeting certain requirements.

If you’re experiencing financial hardship, however, the lender may agree to temporarily lower your payments, waive a payment, or shift to interest-only payments.

Can Lead to Over-Borrowing

Private loans typically allow you to borrow up to 100% of your cost of attendance, minus other aid you’ve already received. Just because you can borrow that much, however, doesn’t necessarily mean you should. Borrowing the maximum incurs more interest over the duration of your loans and increases your payments, which can make repayment more difficult.

Subsidized federal student loans, awarded based on financial need, come with an interest subsidy, meaning the government pays your interest while you’re in school and for six months after you graduate. This can add up to a significant savings.

Subsidies don’t exist with private student loans. Interest accrues from Day One, and in some cases, you might need to make interest payments while still in school. If you don’t pay the interest as you go, it’s added to your debt as capitalized interest when you finish school. (This is also the case with federal unsubsidized loans.)

Federal student loans are awarded as a part of a student’s financial aid package. In order to apply for federal student loans, students must fill out the FAFSA each year. No credit check is needed to qualify.

To apply for private student loans, students need to fill out an application directly with their preferred lender. Application requirements vary depending on the lender. A credit check is typically required.

The interest rates on federal student loans are fixed and are set annually by Congress. Once you’ve taken out a federal loan, your interest rate is locked for the life of the loan.

For the 2025-2026 school year, the federal student loan interest rate is 6.39% for Direct Subsidized and Unsubsidized Loans for undergraduates, 7.94% for Direct Unsubsidized Loans for graduate and professional students, and 8.94% for Direct PLUS loans for parents and graduate or professional students.

Private lenders, on the other hand, are free to set interest rates. Rates may be fixed or variable and depend on several factors, including your (or your cosigner’s) credit score, loan amount, and chosen repayment term. Private student loan rates may start as low as 3.47%, according to the Education Data Initiative.

Repayment Plans

Borrowers with federal student loans can select from several different federal repayment plans , including income-driven repayment plans. You can defer payments while enrolled at least half-time and immediately after graduation.

Repayment plans for private loans are set by the individual lender. Many private student loan lenders allow you to defer payments during school and for six months after graduation. They also have a variety of repayment terms, often ranging from five to 20 years.

Keep in mind that for federal student loans, access to all income-based plans is currently cut off for new borrowers while the Trump administration reevaluates.

Options for Deferment or Forbearance

Federal student loan borrowers can apply for deferment or forbearance if they encounter financial difficulties while they are repaying their loans. These options allow borrowers to pause their loan payments (interest, however, will typically continue to accrue).

Some private lenders may offer options for borrowers who are facing financial difficulties, including short periods of deferment or forbearance. Some also offer unemployment protection, which allows qualifying borrowers who have lost their job through no fault of their own to modify payments on their student loans.

Loan Forgiveness

Borrowers with federal student loans might be able to pursue loan forgiveness through federal programs such as PSLF or Teacher Loan Forgiveness, or after paying down their balances on an IDR plan for a certain period of time.

Since private student loans aren’t controlled by the government, they are not eligible for federal loan forgiveness programs. Though private lenders will often work with borrowers to avoid default, private student loans are rarely forgiven. Generally, it only happens if the borrower becomes permanently disabled or dies, but even then it is up to the specific lender.

Should You Consider Private Student Loans?

There are many different types of student loans. It’s generally a good idea to maximize federal student loans before turning to private student loans. That way, you’ll have access to income-driven repayment plans, loan forgiveness programs, and extended deferment and forbearance periods.

If you still need money to cover tuition or other expenses, and you (or your cosigner) have strong credit, a private student loan can make sense.

Private student loans can also be useful if your expenses suddenly go up and you’ve already maxed out federal student loans, since they allow you to access additional funding relatively quickly. You might also consider a private student loan if you don’t qualify for federal loans. If you’re an international student, for example, a private loan may be your only college funding option.

Another scenario where private student loans can make sense is if you only plan to take out the loan short-term. If you’ll be able to repay the loan over a few years, private student loans could end up costing less overall.

Here’s a look at the steps involved in getting a private student loan.

1. Shop around. Your school may have a list of preferred lenders, but you’re not restricted to this list. You can also do your own research to find top lenders. As you evaluate lenders, consider factors like interest rates, how much you can borrow, the loan term, when you must start repayment, any fees, and if the lender offers any hardship programs.

2. See if you can prequalify. Some lenders allow borrowers to get a quote by filling out a prequalification application. This generally involves a soft credit inquiry (which won’t impact your credit score) and tells you what interest rates and terms you may qualify for. Completing this step can help you decide if you need a cosigner.

3. Gather your information. To officially apply for a private student loan, you typically need to provide your Social Security number, birthdate, and home address, as well as proof of employment and income. You may also need to provide other financial information, such as your assets, rent or mortgage, and tax returns. If you have a cosigner, you’ll have to provide their personal and financial details as well.

4. Submit your application. Once you’ve completed your application, the lender will typically contact your school to verify your information and eligibility. They will then process the student loan and notify you about your approval and disbursement of your money.

💡 Quick Tip: Parents and sponsors with strong credit and income may find much lower rates on no-fee private parent student loans than federal parent PLUS loans. Federal PLUS loans also come with an origination fee.

Does Everyone Get Approved for Private Student Loans?

No, not everyone gets approved for private student loans. Lenders assess various factors to determine eligibility, such as credit history and income. Students with limited credit history may need a cosigner to qualify. Here are the key factors lenders consider:

If you don’t meet these qualifications, you can apply with a cosigner who does.

Apply for a Private Student Loan with SoFi

Private student loans are offered by banks, credit unions, and online lenders to help college students cover their educational expenses. They are not part of the federal student loan program, and generally do not feature the flexible repayment terms or borrower protections offered by federal student loans.

However, private student loans come with higher loan limits, and the borrowing costs are sometimes lower compared to their federal counterparts.

If you’ve exhausted all federal student aid options, no-fee private student loans from SoFi can help you pay for school. The online application process is easy, and you can see rates and terms in just minutes. Repayment plans are flexible, so you can find an option that works for your financial plan and budget.

Cover up to 100% of school-certified costs including tuition, books, supplies, room and board, and transportation with a private student loan from SoFi.

FAQ

Why would someone get a private student loan?

Students typically turn to private student loans when federal loans won’t cover all of their costs. Private student loans come with higher borrowing limits than their federal counterparts. The aggregate max dependent students can borrow from the government for their entire undergraduate education is $31,000, which is sometimes not nearly enough to cover the cost of attendance.

With private loans, on the other hand, you can typically borrow up to the total cost of attendance, minus any financial aid received, every year. This gives you more flexibility to get the financing you need. Keep in mind, though, that private student loans do not come with the same federal protections and benefits offered by federal student loans.

Will private student loans be forgiven?

Private student loans aren’t funded by the government, so they don’t offer the same forgiveness programs. In fact, private student loan forgiveness is rare.

If you experience financial hardship, however, many lenders will work with you to stay out of default. They may agree to temporarily lower your payments, waive a payment, or switch to interest-only payments. Or, you might qualify for deferment or forbearance, which temporarily postpones your payments (though interest continues to accrue).

Are private student loans paid to you or the school?

Private student loans are typically disbursed directly to the school to cover tuition, fees, and other educational expenses. Any remaining funds after those costs are covered are then refunded to the student, which can be used for additional expenses like housing, textbooks, and personal living costs.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loans are subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, the student's at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change. This information is current as of 4/22/2025 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Student Loan Refinance Terms and conditions apply. SoFi Refinance Student Loans are private loans. When you refinance federal loans with a SoFi loan, YOU FORFEIT YOUR ELIGIBILITY FOR ALL FEDERAL LOAN BENEFITS, including all flexible federal repayment and forgiveness options that are or may become available to federal student loan borrowers including, but not limited to: Public Service Loan Forgiveness (PSLF), Income-Based Repayment, Income-Contingent Repayment, extended repayment plans, PAYE or SAVE. Lowest rates reserved for the most creditworthy borrowers. Learn more at SoFi.com/eligibility. SoFi Refinance Student Loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Non-bank financial institutions provide financial services, but they don’t hold the same license or charter as a bank. Also referred to as non-bank financial companies or NBFCs, these entities can extend credit, provide investment services, cash checks, and exchange currencies. However, they generally can’t accept deposits from customers.

There are different types of non-bank financial institutions, and the way they’re structured can determine what services they provide. An NBFC can serve as a complement to traditional banking services or act as a competitor to licensed banks.

Here, you’ll learn more about these businesses, how they compare to banks, and their pros and cons.

What Are Non-Bank Financial Institutions?

Nonbanking financial institutions (NBFI) are institutions that don’t have a banking license but are able to facilitate certain types of financial services. They’re different from depository institutions, which can offer deposit accounts such as checking accounts, savings accounts, or money market accounts. An NBFI or NBFC is not licensed or equipped to accept deposits.

Non-bank financial institutions can specialize in niche financial services, including:

They can target a broad or narrow range of customers, which can include consumers, business owners, and corporate entities. Because they’re not licensed the same way that banks are, NBFCs are not subject to the same degree of government regulation and oversight.

Increase your savings with a limited-time APY boost.*

*Earn up to 4.00% Annual Percentage Yield (APY) on SoFi Savings with a 0.70% APY Boost (added to the 3.30% APY as of 12/23/25) for up to 6 months. Open a new SoFi Checking and Savings account and pay the $10 SoFi Plus subscription every 30 days OR receive eligible direct deposits OR qualifying deposits of $5,000 every 31 days by 3/30/26. Rates variable, subject to change. Terms apply here. SoFi Bank, N.A. Member FDIC.

Now that you know NBFCs’ meaning, consider how these institutions work. In general, NBFCs work by providing financial services that are outside the scope of what traditional banking typically entails. There are different types of organizations that can bear the NBFC (or NBFI) label. The type of organization can determine how it works and what services it offers.

In terms of regulation, NBFCs generally operate within the framework of the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act. However, the scope of regulation that extends to NBFCs and NBFIs is limited. For that reason, they’re sometimes referred to as “shadow banks” since they operate within the shadows of traditional banking institutions.

Pros and Cons of NBFCs

Non-bank financial institutions have both advantages and disadvantages. On one hand, they can play an important role in providing financial services outside the confines of traditional banking.

However, questions have been raised about the lack of oversight for NBFCs and what implications that might have for the individuals and businesses that use them.

Here are some of the main pros and cons of NBFCs at a glance.

Pros of NBFCs

Cons of NBFCs

NBFCs can provide easier access to credit for individuals and businesses who need to borrow money.

NBFCs cannot provide certain banking services, including offering deposit accounts.

Investors may be able to find higher-yield through an NBFC or NBFI that isn’t offered at a bank.

Financial experts have argued that NBFCs and NBFIs can pose a systemic risk to the financial system as a whole.

NBFCs can offer alternative services to customers, such as check cashing, that may otherwise be inaccessible.

Operations are largely unregulated and there may be less transparency around NBFCs vs. traditional banks.

Accountability is more of a question mark with non-bank financial companies since there’s less oversight overall. The increase in popularity of NBFCs has raised questions about the need for greater regulation of this section of the financial services industry.

You may wonder how NBFCs and NBFIs compare to banks and fintech companies. Here are some points to consider:

• Non-bank financial companies are not the same as banks, and they can also be differentiated from fintech. Again, a bank is a financial institution that holds a license or charter which allows it to accept deposits from its customers. Some banks may fall within the category of Community Development Financial Institutions (CDFIs), which help to promote access to capital and financial services in underserved areas.

• Fintech or financial technology is a term that describes the use of innovation to improve financial services and products. Fintech generally encompasses tools, apps, and other tech that can make managing money or borrowing it easier. There can be some overlap between NBFCs and fintech or between fintech and banks.

Which is better, an NBFC vs. a bank vs. fintech? There is no single answer as each one can fulfill different needs. Comparing them side by side can make it easier to distinguish between them.

Banks are financial institutions that hold a federal or state license or charter which allows them to accept deposits.

Fintech is a broad term that can refer to technological innovations that are applied within the financial services industry.

How It Works

NBFCs work by offering financial services (other than accepting deposits) to their customers, such as check cashing, investment services, or insurance.

Banks work by accepting deposits, lending money, and facilitating financial transactions. Some of the benefits of local banking include being able to open a checking account, apply for a mortgage, or pay bills online.

How fintech works can depend on its application. For example, budgeting apps can link to your checking account to track spending automatically. Robo-advisors make it easy to invest using an algorithm.

Whom It’s For

NBFCs may be right for individuals or businesses who are seeking services outside of traditional banking.

Banks are suited to people who want to be able to deposit funds, withdraw them on demand, or borrow money.

Fintech may appeal to people who want easier access to their finances online or via mobile apps.

Examples of NBFCs

As mentioned, there are different types of NBFCs and NBFIs. If you’re looking for a specific non-banking financial institution example, the list may include:

• Life insurance companies

• Insurance companies that underwrite disability insurance policies

• Property insurance companies

• Mutual funds

• Pension funds

• Hedge funds

• Financial advisors and investment advisors

• Securities traders

• Broker-dealers

• Mortgage companies

• Peer-to-peer lending companies

• Payday lenders

• Leasing or financing companies

• Companies that provide money transfer services

• Check cashing companies.

If you invest money, send money to friends and family via an app, or own a home, then chances are you’ve encountered an NBFC somewhere along the way. Examples of companies that may be classified as NBFC include LendingClub, Prosper, and Quicken Loans.

At the same time, you may also use traditional banking services if you have a checking account or savings account at a brick-and-mortar bank or an online bank.

NBFCs and the 2008 Financial Crash

The 2008 financial crash was fueled by a number of factors, including risky lending and investment practices. The resulting fallout included bank failures, banking bailouts, and a housing market crisis. Many of the companies that were engaging in these risky behaviors were NBFCs.

In 2010, the Dodd-Frank Act was passed to address some of the conditions that led to the crisis, including the lack of regulation and oversight as it pertained to NBFCs. The legislation made it possible for non-banking financial institutions to flourish, rather than whither away in the wake of the crisis.

Why? Simply because NBFCs continued to lend money at a time when traditional banks were placing greater restrictions on lending. While questions linger about the degree of regulation needed for NBFCs, their popularity has only increased since the financial crisis.

Non-bank financial institutions can play a part in how you manage your money. For some people, they may provide financial services that make their lives easier. However, they are not regulated in the same way that licensed or chartered banks are. Also, if you want to be able to deposit money into your checking or savings account, then you can do that through a bank.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with eligible direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with SoFi, NerdWallet’s 2024 winner for Best Checking Account Overall.* Enjoy 3.30% APY on SoFi Checking and Savings with eligible direct deposit.

FAQ

How are NBFCs different banks?

NBFCs are different from banks because they do not hold a banking license or charter. While they can provide some of the same financial services as banks, they’re not equipped to accept deposits from customers.

What is the difference between fintech and NBFCs?

Fintech refers to the use of innovation and technology to improve financial products and expand access to financial services. An NBFC can use fintech in order to offer its products and services to its customers. For example, an investment company may offer robo-advisor services that operate on a fintech platform.

What are the disadvantages of NBFCs?

The main disadvantages of NBFCs include lack of government regulation and oversight, as well as their inability to offer deposit accounts. However, NBFCs can offer numerous advantages, including convenient access to credit and the potential to earn higher returns on investments.

About the author

Rebecca Lake

Rebecca Lake has been a finance writer for nearly a decade, specializing in personal finance, investing, and small business. She is a contributor at Forbes Advisor, SmartAsset, Investopedia, The Balance, MyBankTracker, MoneyRates and CreditCards.com. Read full bio.

Photo credit: iStock/shapecharge SoFi Checking and Savings is offered through SoFi Bank, N.A. Member FDIC. The SoFi® Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

Annual percentage yield (APY) is variable and subject to change at any time. Rates are current as of 12/23/25. There is no minimum balance requirement. Fees may reduce earnings. Additional rates and information can be found at https://www.sofi.com/legal/banking-rate-sheet

Eligible Direct Deposit means a recurring deposit of regular income to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government benefit payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Eligible Direct Deposit”) via the Automated Clearing House (“ACH”) Network every 31 calendar days.

Although we do our best to recognize all Eligible Direct Deposits, a small number of employers, payroll providers, benefits providers, or government agencies do not designate payments as direct deposit. To ensure you're earning the APY for account holders with Eligible Direct Deposit, we encourage you to check your APY Details page the day after your Eligible Direct Deposit posts to your SoFi account. If your APY is not showing as the APY for account holders with Eligible Direct Deposit, contact us at 855-456-7634 with the details of your Eligible Direct Deposit. As long as SoFi Bank can validate those details, you will start earning the APY for account holders with Eligible Direct Deposit from the date you contact SoFi for the next 31 calendar days. You will also be eligible for the APY for account holders with Eligible Direct Deposit on future Eligible Direct Deposits, as long as SoFi Bank can validate them.

Deposits that are not from an employer, payroll, or benefits provider or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, Wise, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, or are non-recurring in nature (e.g., IRS tax refunds), do not constitute Eligible Direct Deposit activity. There is no minimum Eligible Direct Deposit amount required to qualify for the stated interest rate. SoFi Bank shall, in its sole discretion, assess each account holder's Eligible Direct Deposit activity to determine the applicability of rates and may request additional documentation for verification of eligibility.

See additional details at https://www.sofi.com/legal/banking-rate-sheet.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.