Table of Contents

Maxing out your 401(k) involves contributing the maximum allowable amount to your workplace retirement account to increase the benefit of compounding and appreciating assets over time.

All retirement plans come with contribution caps, and when you hit that limit it means you’ve maxed out that particular account.

There are a lot of things to consider when figuring out how to max out your 401(k) account, including whether maxing out your account is a good idea in the first place. Read on to learn about the pros and cons of maxing out your 401(k).

Key Points

• Maxing out your 401(k) contributions can help you save more for retirement and take advantage of tax benefits.

• If you want to max out your 401(k), strategies include contributing enough to get the full employer match, increasing contributions over time, utilizing catch-up contributions if eligible, automating contributions, and adjusting your budget to help free up funds for additional 401(k) contributions.

• Diversifying your investments within your 401(k) and regularly reviewing and rebalancing your portfolio can optimize your returns.

• Seeking professional advice and staying informed about changes in contribution limits and regulations can help you make the most of your 401(k).

What Exactly Does It Mean to ‘Max Out Your 401(k)?’

Maxing out your 401(k) means that you contribute the maximum amount allowed in a given year, as specified by the established 401(k) contribution limits. But it can also mean that you’re maxing out your contributions up to an employer’s percentage match.

If you want to max out your 401(k) in 2025, you’ll need to contribute $23,500. If you’re 50 or older, you can contribute an additional $7,500, for an annual total of $31,000. In addition, in 2025, those aged 60 to 63 may contribute up to an additional $11,250 instead of $7,500, thanks to SECURE 2.0, for an annual total of $34,750.

To max out your 401(k) in 2026, you would need to contribute $24,500. If you’re 50 or older, you can contribute an additional catch-up contribution of $8,000, for a total for the year of $32,500. Also in 2026, those aged 60 to 63 may contribute up to an additional $11,250 SECURE 2.0 catch-up instead of $8,000, for an annual total of $35,750.

Should You Max Out Your 401(k)?

Generally speaking, yes, it’s a good thing to max out your 401(k) so long as you’re not sacrificing your overall financial stability to do it. Saving for retirement is important, which is why many financial experts would likely suggest maxing out any employer match contributions first.

But while you may want to take full advantage of any tax and employer benefits that come with your 401(k), you also want to consider any other financial goals and obligations you have before maxing out your 401(k).

That doesn’t mean you should put other goals first, and not contribute to your retirement plan at all. That’s not wise. Maintaining a baseline contribution rate for your future is crucial, even as you continue to save for shorter-term aims or put money toward debt repayment.

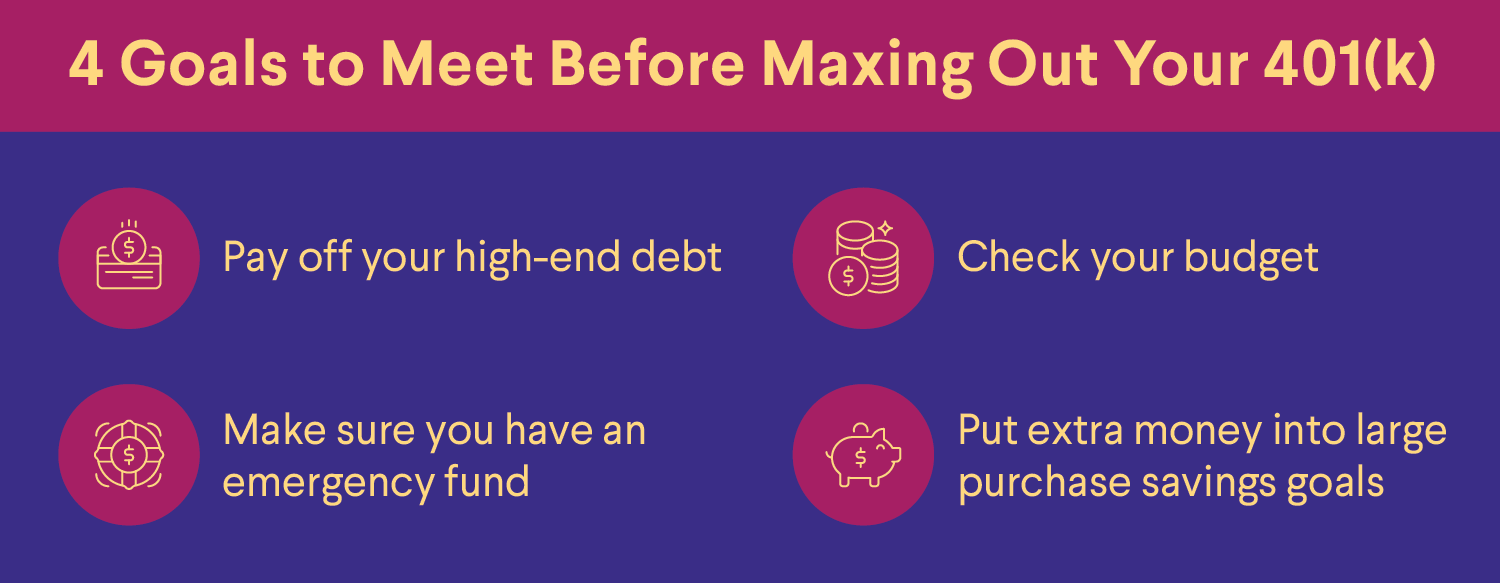

Other goals might include:

• Is all high-interest debt paid off? High-interest debt like credit card debt should be paid off first, so it doesn’t accrue additional interest and fees.

• Do you have an emergency fund? Life can throw curveballs — it’s smart to be prepared for job loss or other emergency expenses.

• Is there enough money in your budget for other expenses? You should have plenty of funds to ensure you can pay for additional bills, like student loans, health insurance, and rent.

• Are there other big-ticket expenses to save for? If you’re saving for a large purchase, such as a home or going back to school, you may want to put extra money toward this saving goal rather than completely maxing out your 401(k), at least for the time being.

Once you can comfortably say that you’re meeting your spending and savings goals, it might be time to explore maxing out your 401(k). There are many reasons to do so — it’s a way to take advantage of tax-deferred savings, employer matching (often referred to as “free money”), and it’s a relatively easy and automatic way to invest and save, since the money gets deducted from your paycheck once you’ve set up your contribution amount.

How to Max Out Your 401(k)

Only a relatively small percentage of people max out their 401(k)s, but that doesn’t mean you can’t be one of them. Here are some strategies for how to max out your 401(k).

1. Max Out 401(k) Employer Contributions

Your employer may offer matching contributions, and if so, there are typically rules you will need to follow to take advantage of their match.

An employer may require a minimum contribution from you before they’ll match it, or they might match only up to a certain amount. They might even stipulate a combination of those two requirements. Each company will have its own rules for matching contributions, so review your company’s policy for specifics.

For example, suppose your employer will match your contribution up to 3%. So, if you contribute 3% to your 401(k), your employer will contribute 3% as well. Therefore, instead of only saving 3% of your salary, you’re now saving 6%. With the employer match, your contribution just doubled. Note that employer contributions can range from nothing at all up to a certain limit. It depends on the employer and the plan.

Since saving for retirement is one of the best investments you can make, it’s wise to take advantage of your employer’s match. Every penny helps when saving for retirement, and you don’t want to miss out on this “free money” from your employer.

If you’re not already maxing out the matching contribution and wish to, you can speak with your employer (or HR department, or plan administrator) to increase your contribution amount, you may be able to do it yourself online.

2. Max Out Salary-Deferred Contributions

While it’s smart to make sure you’re not leaving free money on the table, maxing out your employer match on a 401(k) is only part of the equation.

In order to make sure you’re setting aside an adequate amount for retirement, consider contributing as much as your budget will allow. As noted earlier, individuals younger than age 50 can contribute up to $23,500 in 2025, and up to $24,500 in 2026.

Those contributions aren’t just an investment in your future lifestyle in retirement. Because they are made with pre-tax dollars, they lower your taxable income for the year in which you contribute. For some, the immediate tax benefit is as appealing as the future savings benefit.

3. Take Advantage of Catch-Up Contributions

As mentioned, 401(k) catch-up contributions allow investors aged 50 and over to increase their retirement savings — which is especially helpful if they’re behind in reaching their retirement goals.

Individuals 50 and over can contribute an additional $7,500 for a total of $31,000 in 2025. And in 2026, those 50 and older can contribute an extra $8,000 for a total of $32,500. And in both 2025 and 2026, those aged 60 to 63 can contribute up to an additional $11,250, instead of $7,500 in 2025 and $8,000 in 2026, for a total of $34,750 and $35,750 respectively. Putting all of that money toward retirement savings can help you truly max out your 401(k).

As you draw closer to retirement, catch-up contributions can make a difference, especially as you start to calculate when you can retire. Whether you have been saving your entire career or just started, this benefit is available to everyone who qualifies.

And of course, in many cases, this extra contribution will lower taxable income even more than regular contributions. Although using catch-up contributions may not push everyone to a lower tax bracket, it will certainly minimize the tax burden during the next filing season for many filers — with an important exception.

Under a new law regarding catch-up contributions that went into effect on January 1, 2026 (as part of SECURE 2.0), individuals aged 50 and older whose FICA wages exceeded $150,000 in 2025 are required to put their 401(k) catch-up contributions into a Roth 401(k) account. Because of the way Roth accounts work, these individuals will pay taxes on their catch-up contributions upfront, and make eligible withdrawals tax-free in retirement. This means their taxable income will not be lowered; they could even potentially move into higher tax bracket. Those impacted by the new law should check with their employer or plan administrator to find out how to proceed.

4. Reset Your Automatic 401(k) Contributions

When was the last time you reviewed your 401(k)? It may be time to check in and make sure your retirement savings goals are still on track. Is the amount you originally set to contribute each paycheck still the correct amount to help you reach those goals?

With the increase in contribution limits most years, it may be worth reviewing your budget to see if you can up your contribution amount to max out your 401(k). If you don’t have automatic payroll contributions set up, you could set them up.

It’s generally easier to save money when it’s automatically deducted; a person is less likely to spend the cash (or miss it) when it never hits their checking account in the first place.

If you’re able to max out the full 401(k) limit, but fear the sting of a large decrease in take-home pay, consider a gradual, annual increase such as 1% — how often you increase it will depend on your plan rules as well as your budget.

5. Put Bonus Money Toward Retirement

Unless your employer allows you to make a change, your 401(k) contribution may be deducted from any bonus you might receive at work. Some employers allow you to determine a certain percentage of your bonus to contribute to your 401(k).

Consider possibly redirecting a large portion of a bonus to 401k contributions, or into another retirement account, such as an individual retirement account (IRA). Because this money might not have been expected, you won’t miss it if you contribute most of it toward your retirement.

You could also do the same thing with a raise. If your employer gives you a raise, consider putting it directly toward your 401(k). Putting this money directly toward your retirement can help you inch closer to maxing out your 401(k) contributions.

6. Maximize Your 401(k) Returns and Fees

Many people may not know what they’re paying in investment fees or management fees for their 401(k) plans. By some estimates, the average fees for 401(k) plans are between 0.5% and 2%, but some plans may have higher fees.

Fees add up — even if your employer is paying the fees now, you’ll have to pay them if you leave the job and keep the 401(k).

Essentially, if an investor has $100,000 in a 401(k) and pays $1,000 or 1% (or more) in fees per year, the fees could add up to thousands of dollars over time. Any fees you have to pay can chip away at your retirement savings and reduce your returns.

It’s important to ensure you’re getting the most for your money in order to maximize your retirement savings. If you are currently working for the company, you could discuss high fees with your HR team.

One way to potentially lower your costs is to find more affordable investment options. Generally speaking, index funds often charge lower fees than other investments. If an employer’s plan offers an assortment of low-cost index funds, may consider investing in these funds to save some money and help build a diversified portfolio.

What Happens If You Contribute Too Much to Your 401(k)?

After an individual maxes out their 401(k) for the year — meaning they’ve hit the contribution limit corresponding to their age range — if they don’t stop making contributions they will risk paying additional taxes on their overcontributions.

In the event that an individual makes an overcontribution, they might let their plan manager or administrator know, and withdraw the excess amount. If they leave the excess in the account, it’ll be taxed twice — once when it was contributed initially, and again when they take it out.

What to Do After Maxing Out a 401(k)?

If you max out your 401(k) this year, pat yourself on the back. Maxing out your 401(k) is a financial accomplishment. But now you might be wondering, what’s next? Here are some additional retirement savings options to consider if you have already maxed out your 401(k).

Open an IRA

An individual retirement account (IRA) can be an option to complement an employer’s retirement plans. With a traditional IRA, you can contribute pre-tax dollars up to the annual limit, which is $7,000 in 2025. If you’re 50 or older, you can contribute an extra $1,000, for an annual total of $8,000 in 2025. In 2026, you can contribute up to $7,500, while those 50 and older can contribute an additional $1,100, for a total of $8,600 for 2026.

You may also choose to consider a Roth IRA. As with a traditional IRA, the annual contribution limit for a Roth IRA in 2025 is $7,000, and $8,000 for those 50 or older. And in 2026, the annual Roth IRA contribution limit is $7,500, and $8,600 for those age 50 and up.

Roth IRA accounts have income limits, but if you’re eligible, you can contribute with after-tax dollars, which means you won’t have to pay taxes on earnings withdrawals in retirement as you do with traditional IRAs.

It’s possible to open an IRA at a brokerage, mutual fund company, or other financial institution. If you ever leave your job, you can typically roll your employer’s 401(k) into your IRA without facing tax consequences as long as both accounts are similarly taxed, such as rolling funds from a traditional 401(k) to a traditional IRA, and funds are transferred directly from one plan to the other. Doing a 401(k) to IRA rollover may allow you to invest in a broader range of investments with lower fees.

Boost an Emergency Fund

Experts often advise establishing an emergency fund with at least three to six months of living expenses before contributing to a retirement savings plan. Perhaps you’ve already done that — but haven’t updated that account in a while. As your living expenses increase, it’s a good idea to make sure your emergency fund grows, too. This will cover you financially in case of life’s little curveballs: new brake pads, a new roof, or unforeseen medical expenses.

Save for Health Care Costs

Contributing to a health savings account (HSA) can reduce out-of-pocket costs for expected and unexpected health care expenses, though you can only open and contribute to an HSA if you are enrolled in a high-deductible health plan (HDHP).

For tax year 2025, those eligible can contribute up to $4,300 pre-tax dollars for an individual plan or up to $8,550 for a family plan. Those 55 or older who are not enrolled in Medicare can make an additional catch-up contribution of $1,000 per year.

For tax year 2026, those who are eligible can contribute up to $4,400 for an individual plan or up to $8,750 for a family plan. Those 55 or older who are not enrolled in Medicare can again make an additional catch-up of $1,000.

The money in this account can be used for qualified out-of-pocket medical expenses such as copays for doctor visits and prescriptions. Another option is to leave the money in the account and let it grow for retirement. Once you reach age 65, you can take out money from your HSA without a penalty for any purpose. However, to be exempt from taxes, the money must be used for a qualified medical expense. Any other reasons for withdrawing the funds will be subject to regular income taxes.

Increase College Savings

If you’re feeling good about maxing out your 401(k), consider increasing contributions to your child’s 529 college savings plan (a tax-advantaged account meant specifically for education costs, sponsored by states and educational institutions).

College costs continue to creep up every year. Helping your children pay for college helps minimize the burden of college expenses, so they hopefully don’t have to take on many student loans.

Open a Brokerage Account

After maxing out a 401(k), individuals might also consider opening a brokerage account. Brokerage firms offer various types of investment accounts, each with different services and fees. A full-service brokerage firm may provide different financial services, which include allowing investors to trade securities.

Many brokerage firms require individuals to have a certain amount of cash to open accounts and have enough funds for trading fees and commissions. While there are no limits on how much can be contributed to the account, earned dividends are taxable in the year they are received. Therefore, if you earn a profit or sell an asset, you must pay a capital gains tax. On the other hand, if you sell a stock at a loss, that becomes a capital loss. This means that the transaction may yield a tax break by lowering your taxable income.

Pros and Cons of Maxing Out Your 401(k)

thumb_up

Pros:

• Increased Savings: More contributions added to a retirement savings plan could lead to more growth over time.

• Simplified Saving and Investing: Maxing out your 401(k) can also make your saving and investing relatively easy, as long as you’re taking a no-lift approach to setting your money aside thanks to automatic contributions.

thumb_down

Cons:

• Affordability: Maxing out a 401(k) may not be financially feasible for everyone. It may be challenging due to existing debt or other savings goals.

• Risk: Like all investments, there is the risk of loss.

• Opportunity Costs: Money invested in retirement plans could be used for other purposes. During strong stock market years, non-retirement investments may offer more immediate access to funds.

Test your understanding of what you just read.

The Takeaway

Maxing out your 401(k) involves matching your employer’s maximum contribution match, and also, contributing as much as legally allowed to your retirement plan in a given year. If you have the flexibility in your budget to do so, maxing out a 401(k) can be an effective way to build retirement savings.

And once a 401(k) is maxed out? There are other ways an individual might direct their money, including opening an IRA, or contributing more to an HSA or to a child’s 529 plan.

Prepare for your retirement with an individual retirement account (IRA). It’s easy to get started when you open a traditional or Roth IRA with SoFi. Whether you prefer a hands-on self-directed IRA through SoFi Securities or an automated robo IRA with SoFi Wealth, you can build a portfolio to help support your long-term goals while gaining access to tax-advantaged savings strategies.

Help build your nest egg with a SoFi IRA.

FAQ

What happens if I max out my 401(k) every year?

Assuming you don’t overcontribute, you may see your retirement savings increase if you max out your 401(k) every year, and hopefully, be able to reach your retirement and savings goals sooner.

Will you have enough to retire after maxing out a 401(k)?

There are many factors that need to be considered to determine if you’ll have enough money to retire if you max out your 401(k). Start by getting a sense of how much you’ll need to retire by using a retirement expense calculator. Then you can decide whether maxing out your 401(k) for many years will be enough to get you there, assuming an average stock market return and compounding built in.

First and foremost, you’ll need to consider your lifestyle and where you plan on living after retirement. If you want to spend a lot in your later years, you’ll need more money. As such, a 401(k) may not be enough to get you through retirement all on its own, and you may need additional savings and investments to make sure you’ll have enough.

What is the best way to max out a 401(k)?

Some effective ways to max out a 401(k) include contributing up to the allowable amount for the year (for 2025, that’s $23,500 for those under age 50, and for 2026, it’s $24,500); using catch-up contributions if you’re aged 50 or older ($7,500 in 2025, and $8,000 in 2026, or $11,250 if you’re ages 60 to 63 in 2025 and 2026); contributing enough to get your employer’s matching contributions if offered; automating your contributions and increasing them yearly, if possible; and directing a percentage of any bonus you receive into your 401(k).

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Mutual Funds (MFs): Investors should read and carefully consider the information contained in the prospectus, which contains the Mutual Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or SoFi's customer service at: 1.855.456.7634. Mutual Funds must be bought and sold at NAV (Net Asset Value); unless otherwise noted in the prospectus, trades are only done once per day after the markets close. Investment returns are subject to risks. Shares may be worth more or less their original value when redeemed. The diversification of a mutual fund will not protect against loss. A mutual fund may not achieve its stated investment objective. Rebalancing and other activities within the fund may have tax implications.

Investment Risk: Diversification can help reduce some investment risk, but cannot guarantee profit nor fully protect in a down market.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

This article is not intended to be legal advice. Please consult an attorney for advice.

SOIN-Q425-085

Q126-3525874-013