Liz Looks at: Why Inversion Matters

Tail over Tea Kettle

The fear-based moves in markets over the last few weeks have brought a phrase back into our conversations — curve inversion. Let’s explore what that is, what it signals about investor sentiment, and why it’s used as a forward-looking indicator.

The Long and Short of It

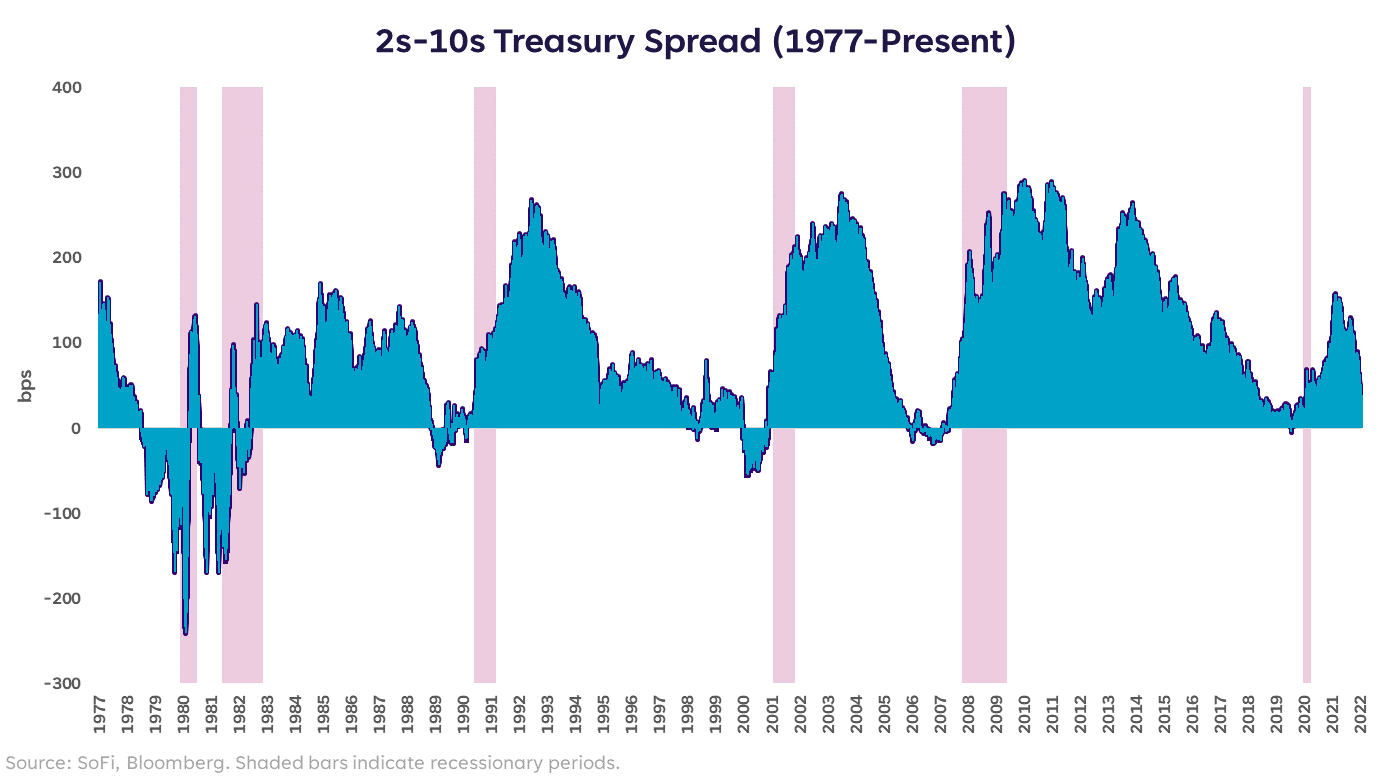

First things first, what the heck is a yield curve inversion? The U.S. Treasury yield curve is considered “inverted” when the 2-year Treasury yield rises above the 10-year Treasury yield, causing the curve to be downward sloping between those two points.

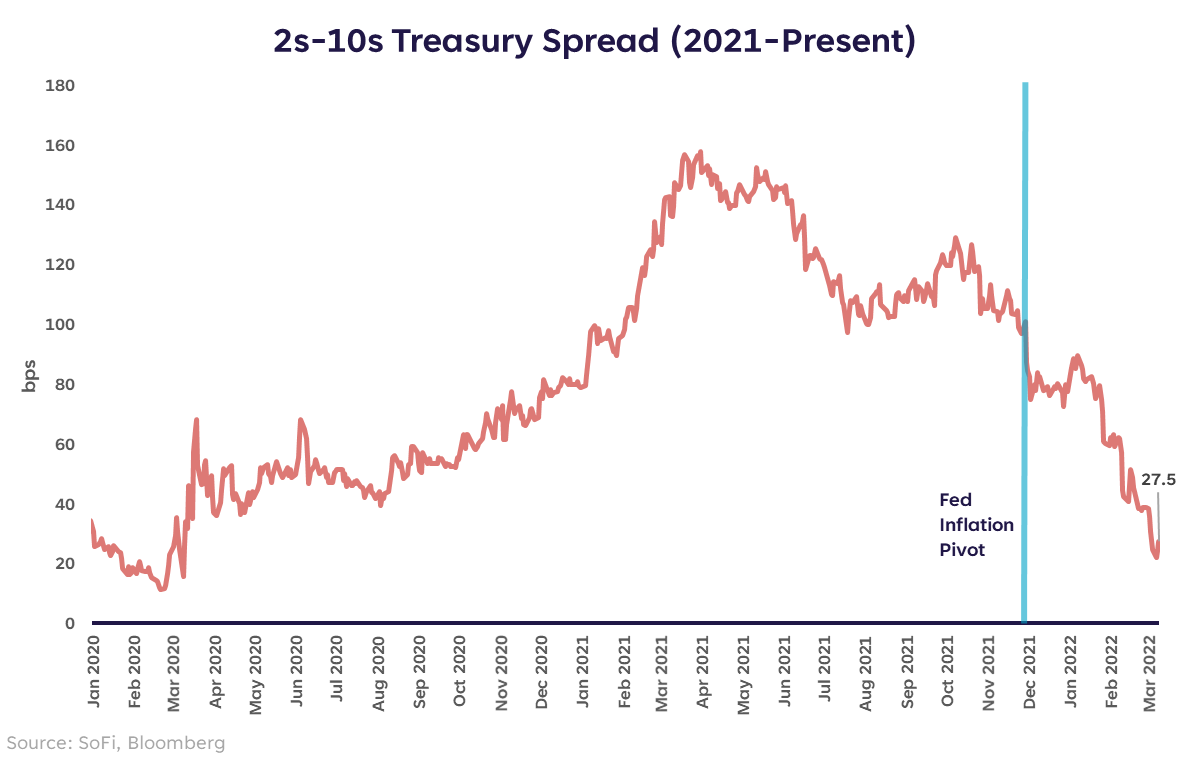

The way we watch this in daily market moves is to look at the spread between the 2-year and 10-year yield, otherwise known as the “2s/10s spread”. When this spread is larger (wider), the curve is further from inverting. As the spread narrows or turns negative, we are approaching, or in, inversion territory.

The reason we’re talking about this right now is because the 2s/10s spread has narrowed by more than 60 basis points since the beginning of the year, bringing it down to a small 27 basis point difference as of Mar 9.

Will the Fed Yield to Yields?

When the curve inverts, it signals a couple things. First, if investors are buying the 10-year Treasury (long end of the curve) and driving yields down, that usually means there’s a heightened level of fear in the market. That comes as a surprise to absolutely no one in the midst of a war between Russia and Ukraine, spiking oil prices alongside already high inflation, and an S&P 500 that’s down 11% YTD.

Second, if investors are selling the 2-year Treasury (short end of the curve) and driving yields up, that usually means they expect short-term rates to rise as a result of Fed rate hikes. Another surprise to absolutely no one.

But what does that mean overall? It means we’re in a pickle and so is the Fed — an inverted curve doesn’t make for good economic expectations in the near-to-medium term. I maintain the view that the Fed isn’t bothered by the correction that’s happened in equity markets, but they would be bothered by a yield curve inversion.

Why? Because yield curve inversions, much like spikes in oil prices, typically precede a recession.

So You’re Telling Me There’s a Chance…

Of a recession? Yes. There’s always a chance of a recession caused by some exogenous shock that we don’t see coming. The odds of that rise when we see other stresses in the markets or economy, or when the traditional signals start to make noise.

To be clear, the yield curve has not inverted. And for it to count as a true inversion that can be seen as a signal, the inversion would need to be reasonably persistent (one month or more, in my opinion). A brief intraday inversion doesn’t count. Even one that lasts a few days and is shallow, doesn’t count.

But given where the spread is at present, it’s important to watch this. I know the Fed is watching.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young Thomas is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

SOSS22031002

All your finances.

All in one app.

App Store rating

![]()

![]()