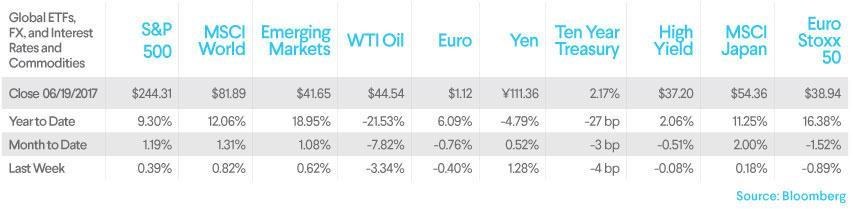

Wealth Market Commentary (Week of June 19, 2017)

A Closer Look at the State of the U.S. Economy

It’s been a relatively quiet month for the market. Equities and fixed income continue to grind higher as investors doubt a near-term revival in inflation. And, with little expectation that tax cuts will be implemented this year, the markets have taken little notice of the relentless political drama coming out of Washington. Given the lack of major market events, we’re taking a step back to focus on the unique state of the U.S. economy right now, how the Federal Reserve might respond, and what it means for the market.

The U.S. economy is currently seeing low unemployment and low inflation. This is unusual. Traditionally, unemployment and inflation have moved in opposite directions: As the unemployment rate falls, inflation starts to increase. The rationale behind this relationship is relatively straightforward: as unemployment falls, companies must compete for labor from a smaller pool. To attract workers, they increase wages and try to pass some of those higher costs on to consumers by raising prices. At the same time, consumers who are now enjoying higher wages have more to spend and start to bid up the prices of goods themselves. Combined, these factors cause rapid inflation.

What makes the relationship between employment and inflation so important is that the Federal Reserve, the central bank of the United States, uses it to manage interest rate policy. The Fed is responsible for trying to keep inflation and unemployment low. It would typically respond to the threat of inflation by raising the federal funds rate which is the rate banks use to lend money to each other overnight. The Fed uses this rate to try to influence all other interest rates such as the rate you’d pay on a car loan or the rate a firm would pay for a loan to build a factory. When the Fed raises the overnight interest rate, consumer interest rates tend to follow, which in turn slows down economic activity and keeps inflation in check.

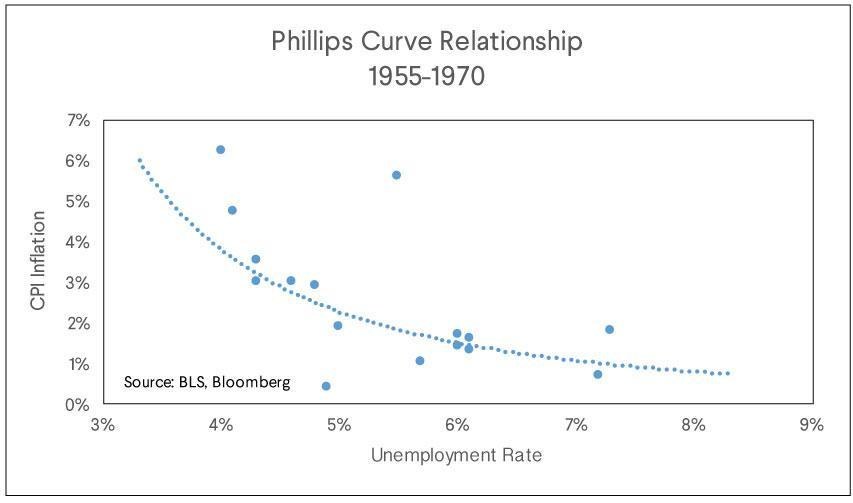

One challenge the Fed faces is that monetary policy moves much more slowly than the economy. This means the Fed has to act before inflation is a problem. The Fed has used tools like the Phillips curve (named for economist William Phillips) to forecast inflation. Below, we can see the relationship in the 1950s and 1960s when it was initially described.

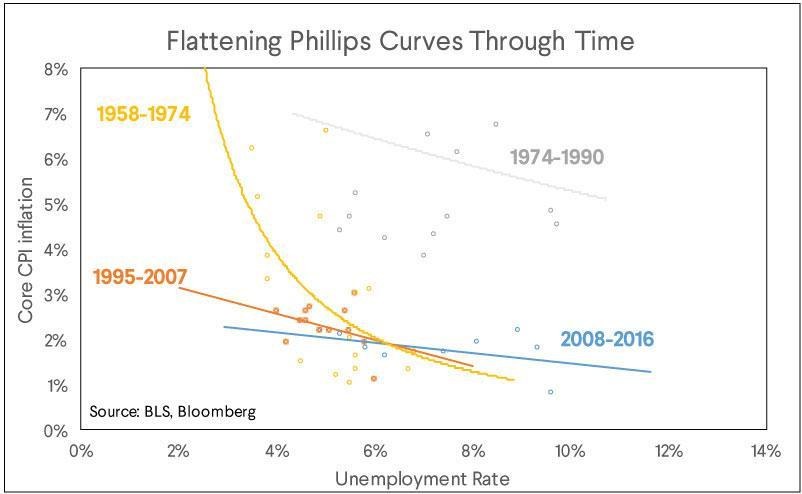

However, something unique has happened since the recession: the relationship between unemployment and inflation is not as strong as it was in the past. We can see in the chart below that the relationship between unemployment and wage inflation has been quite flat. If the relationship between unemployment and inflation that held in the 1960s held today, we would be looking at inflation of around 5% instead of the 1.7% reported last week.

No one knows for certain what might be causing this. One possibility is that the economy has changed and the relationship no longer holds. It could be partially an effect of globalization: American companies can’t raise prices because consumers will simply by cheaper imported products. Or the relationship could be non-linear: for large changes in unemployment there is little change in inflation. However, once we reach full employment, inflation could accelerate rapidly.

The Fed has also noticed the weakening relationship. This leaves them in uncharted territory, yet they are going to have to conduct monetary policy with some view on whether the relationship still holds.

We can look at this as an organizing principle for thinking about markets over the coming years: Either the Phillips curve relationship holds, or it doesn’t. The Fed either thinks it holds, or it doesn’t. This gives us four possible scenarios, each with different implications for asset prices.

If the relationship holds and the Fed thinks it does: the Fed would raise rates faster than the market expects. This would hurt equities in the short term but they should be supported by earnings growth in an inflationary environment. Fixed income, on the other hand, would be hurt as higher interest rates make previously issued bonds less attractive.

If the relationship doesn’t hold but the Fed thinks it does: the Fed would hike rates into an economy that doesn’t need it. This would likely cause some deflation as prices fall and would cause a recession. This would be bad for equities and be bad for fixed income in the short term. However, interest rates would fall again in the event of a recession, pushing bond prices higher.

If the relationship holds but the Fed doesn’t think it does: the Fed would be behind the curve. Inflation would accelerate faster than expected and the Fed would have to hike interest rates quickly in order to catch up. Initially this would be positive for stocks but over the long-term, equity and fixed income prices would likely fall because the economy would be forced to decelerate quickly due to the rapid interest rate hike.

If the relationship doesn’t hold and the Fed doesn’t think it does: the Fed wouldn’t hike rates much more than they already have and they wouldn’t need to. This looks to be the current situation priced into markets. Fixed income and equity prices would be supported as investors look for any source of return in a permanently low interest rate environment.

Which scenario is most likely? We think that at some point wage inflation will start to gain traction and consumer prices will follow. The reason this hasn’t happened yet is that the labor market is not as tight as the unemployment rate suggests, perhaps because more people keep returning to the labor force. We think the Fed is more cautious than it has been in the past, but they do seem to believe the Phillips curve relationship holds some validity. As a result, they are likely to raise rates faster than the market is currently expecting. Because of that, we like equity and short duration fixed income, which is less sensitive to higher interest rates.

The SoFi Wealth Market Commentary does not provide individually tailored investment advice. It has been prepared without regard to the circumstances and objectives of those who receive it. We recommend that investors independently evaluate particular investments and strategies, and encourage investors to seek the advice of one of our financial advisors. The appropriateness of an investment or strategy will depend on an investor’s circumstances and objectives. This is not an offer to buy or sell any security/instrument or to participate in any trading strategy. The value of and income from your investments may vary because of changes in interest rates, foreign exchange rates, default rates, prepayment rates, securities/instruments prices market indexes, operational or financial conditions of companies or other factors. Past performance is not a guide to future performance. Estimates of future performance are based on assumptions that may not be realized.

All your finances.

All in one app.

App Store rating

![]()

![]()