Oct

15

2020

With less people commuting to work due to COVID-19, the number of people refueling at gas stations has also shrunk.

Read more

Here are more healthcare heroes who were nominated for their dedication to helping their communities.

Read more

Retailers are on the lookout for creative ways to highlight their products. A new tool in marketers’ pockets may soon be YouTube.

Read more

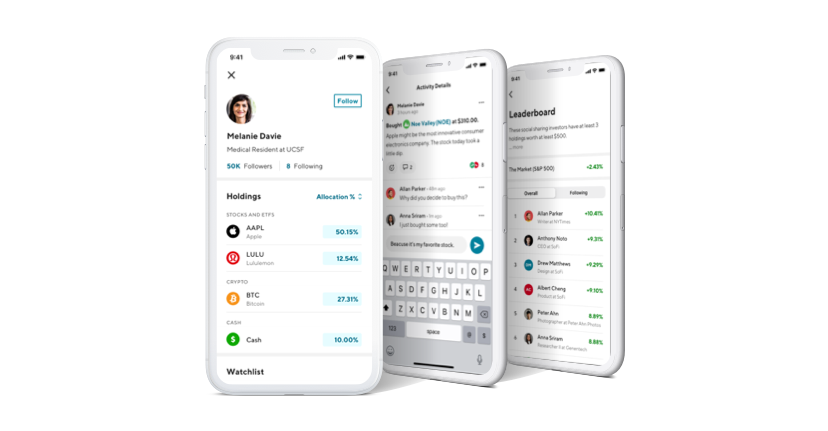

We are excited to announce today that social investing features are now live for all SoFi Invest members!

Read moreStay up to date on the latest business news and stock market happenings.