Table of Contents

Deciding how to invest money in your 20s can seem overwhelming at first; many people have differing opinions or goals, and it’s hard to know where to start. But remember that you don’t need to have a lot of money upfront to reach your financial goals.

Perhaps the most important thing is to start investing early, even if your initial investments are small. Here are a few different strategies for investing money in your 20s.

Key Points

• Starting to invest early in your 20s is one of the most important financial decisions you can make, even with small amounts, as consistency over time potentially allows investments to compound.

• Organizing money by time horizon is essential – immediate needs belong in bank accounts, mid-term goals in high-yield savings or CDs, and long-term retirement savings in tax-advantaged accounts like IRAs or 401(k)s.

• Investors in their 20s can consider stocks, bonds, mutual funds, and ETFs, with stocks offering higher long-term growth potential and the S&P 500 averaging ~10% annual growth from 1957 through 2026, though investors should be aware that inflation and investment fees could affect total returns.

• Young investors could consider maximizing employer 401(k) matching contributions, as failing to contribute enough to receive the full match is equivalent to leaving free money on the table.

• Alternative investments like real estate, REITs, cryptocurrency, and commodities may help diversify a portfolio beyond traditional stocks and bonds.

Think About Financial Goals

When determining your financial goals, you may want to break down short-, medium-, and long-term milestones. You want to ask yourself what you want from your money and figure out when you’ll need to use the money. For example, the money you save for a medium-term goal, like a down payment on your first home, should be treated differently than retirement savings.

So, you may want to start buying stocks right away, but you may also want to give some strategic thought as to how that may fit into your overall financial goals.

If you have not earmarked savings for a specific financial goal, take some time to think about what purpose you’d like to apply it to. A great first saving goal is to have three to six months of living expenses in an emergency fund. After that, it might be good to turn your attention toward savings and investing for longer-term goals, like retirement.

Decide Where to House Your Money

When deciding how to invest money in your 20s, it can help to think about immediate, mid-term, and long-term financial needs. Once you have outlined some money goals, you could consider setting up your accounts. The type of account you open may depend on when you need the money.

Where to Put Immediate Money

Food, bills, rent, and everything else you must pay for on a month-to-month basis are immediate needs. People could keep this money – along with a cushion so as not to overdraft their account – in an online bank account. These types of accounts allow you to withdraw money instantaneously, generally without penalties, making them ideal for your immediate financial needs.

Where to Put Mid-term Money

Mid-term money is any money you might need in the next couple of years, such as a travel fund, wedding fund, or home down payment savings. It might make sense to keep this money in a high-yield savings account, which provides a better return on your money than traditional savings accounts.

High-yield savings accounts, along with other cash equivalents like certificates of deposits (CDs) and money market accounts, are usually considered to be lower-risk investments (though CDs are not helpful for emergency funds because of the early termination penalties).

Where to Put Mid- to Long-term Money

For money you’ll use in five to 20 years, you may be prepared to take slightly more risk than a high-yield savings account. You might choose to keep the money in your high-yield savings account or in CDs, or an online brokerage account where you can invest that money in stocks, bonds, mutual funds, or other asset classes. You can also do a combination of the different types of accounts.

Longer-term savings options, like a tax-advantage 529 plan, can also be appropriate if you’d like to start planning for higher education needs for current or future children.

Where to Put Long-Term Money

Think of long-term money as cash you won’t need for several decades. A retirement account is a great example of an appropriate place to hold long-term money. Retirement plans like a Traditional IRA, Roth IRA, or a 401(k) account can offer significant tax benefits.

💡 Ready to invest in your retirement? Consider opening a Traditional or Roth IRA with SoFi.

Start investing with up to $3,000 in stock.

For a limited time only, open and fund a SoFi Active Invest account and get up to $3,000 in stock.

Offer ends 8/16/26*.

Prefer mobile? Download the app:

Potential Assets to Invest in During Your 20s

One important thing to understand about investing in your 20s is the tradeoff between risk and reward when implementing your investing strategy. You cannot have one without the other. With this risk and reward calculation in mind, you need to determine what asset classes you might consider when investing in your 20s.

Stocks

A stock is a tiny piece of ownership in a publicly-traded company. When you invest in a stock, you could earn money through capital appreciation, dividends, or a combination of the two.

Stocks can be volatile because prices fluctuate according to supply and demand forces as they trade on an open exchange. Even though stocks can be volatile and experience losses, they tend to provide positive returns over time.

Bonds

Although not risk-free, experts generally consider bonds less risky (though not risk-free) than stocks because they are a contract that comes with a stated rate of return. Bonds backed by the U.S. government, called treasury bonds, are generally considered the least-risky within the category of bonds because it is unlikely that the U.S. government will go bankrupt.

Bonds are debt investments, meaning investors fund the debt of some entity. The money you earn on that investment is the interest they pay you for borrowing your money. In addition to treasuries and corporate bonds, there are municipal bonds, which state and local governments issue, and mortgage- and asset-backed bonds, which are bundles of mortgages or other financial assets that pass through the interest paid on mortgages or assets.

Mutual Funds and Exchange-Traded Funds

Some investors might want to utilize mutual funds or exchange-traded funds (ETFs) to gain exposure to certain asset classes.

A fund is essentially a basket of investments – stocks, bonds, another investment type, or a combination thereof. Funds are helpful because they provide immediate diversification, which may help protect against the risk of having too much money invested in one stock, sector, or any other single asset.

Funds are either actively or passively managed. A fund that is passively managed is attempting to track a specific index. An actively managed fund is maintained with a hands-on approach to determine investments in a portfolio. ETFs tend to be passively managed, but there are many actively managed ETFs funds on the market. Mutual funds can be either passively or actively managed.

Tips for Investing In Your 20s

Once you’ve become familiar with the basics of investing, it’s time to put that knowledge into action. These tips can help you shape a strategy for how to invest money in your 20s and beyond.

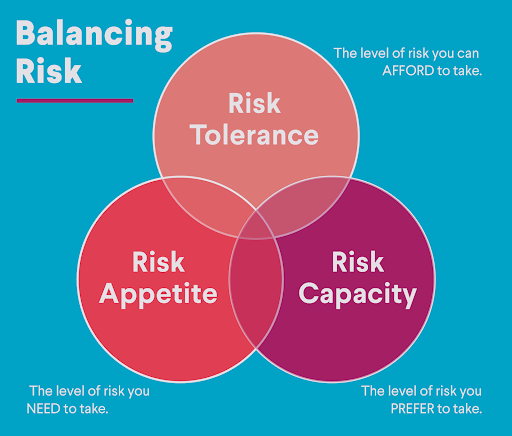

Gauge Your Personal Risk Tolerance

One of the key things to remember about investing in your 20s is that time is on your side. You have a significant time horizon window to allow your portfolio to recover from bouts of inevitable stock market volatility. Because of this, you could take more risks with your investments to try and achieve higher rewards.

Getting to know your personal risk preferences can help you decide where and how to invest in your 20s to achieve your investment goals. It’s also important to understand how risk tolerance matches your risk capacity and appetite.

Risk tolerance means the level of risk you’re comfortable taking. Risk capacity is the level of risk you prefer to take to reach your investment goals, while risk appetite is the level of risk you need to hit those milestones. When you’re younger, playing it too safe with your portfolio might mean missing out on significant investment returns.

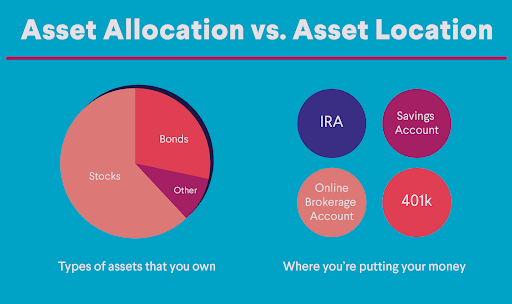

Know the Difference Between Asset Allocation and Asset Location

One strategy for investing in your 20s is to invest a higher allocation of your long-term investments in stocks and less in bonds, then slowly move into more bond investments the closer you get to retirement. This big picture decision is called asset allocation.

But asset allocation is only part of the picture. One might also consider asset location: the types of accounts where you’re putting your money, like savings accounts, an online brokerage account, a 401k, or an IRA.

Take Advantage of Free Money

One of the simplest ways to start investing in your 20s is to enroll in your workplace retirement plan like a 401k.

Once you’ve enrolled in a plan, consider contributing at least enough to get the full company match if your employer offers one. If you don’t, you could be leaving money on the table.

And if you can’t make the full contribution to get the match right away, you can still work your way up to it by gradually increasing your salary deferral percentage. For example, you could raise your contribution rate by 1% each year until you reach the maximum deferral amount.

The Takeaway

Learning how to invest money in your 20s doesn’t happen overnight. And you may still be fuzzy on how certain parts of the market work as you enter your 30s or 40s. But by continually educating yourself about different investments and investing strategies, you can gain the knowledge needed to guide your portfolio toward your financial goals.

One thing to know about investing in your 20s is that consistency can pay off in the long run. Even if you’re only able to invest a little money at a time through 401k contributions or by purchasing partial or fractional shares of stock, those amounts can add up as the years and decades pass.

Invest in what matters most to you with SoFi Active Invest. In a self-directed account provided by SoFi Securities, you can trade stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, options, and more — all while paying $0 commission on every trade. Other fees may apply. Whether you want to trade after-hours or manage your portfolio using real-time stock insights and analyst ratings, you can invest your way in SoFi's easy-to-use mobile app.

Opening and funding an Active Invest account gives you the opportunity to get up to $3,000 in the stock of your choice.¹

FAQ

What are some simple ways to start investing in your 20s?

Prospective investors in their 20s might consider opening a brokerage account to trade stocks and other securities, or they can enroll in a retirement plan, such as their employer’s 401(k) plan, that will also allow them to start investing.

What are the benefits of starting to invest in your 20s?

Starting to invest in your 20s may prove to be a beneficial financial decision, as even with small amounts, investment returns may compound and grow significantly. Of course, there are also risks to consider, but generally, the more time investors have to allow their money to generate potential returns, the better.

Is enrolling in a 401(k) the easiest way to start investing in my 20s?

It may be the simplest or easiest way to start investing. Young investors could consider maximizing employer 401(k) matching contributions, too, as it’s akin to receiving free money that can also be invested. There are risks, of course, which investors should also familiarize themselves with.

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Options involve substantial risk of loss and the possibility an investor may lose the entire amount invested. Before starting options trading, investors should be familiar with the Characteristics and Risks of Standardized Options . TTax implications with options should be considered. Consult your tax advisor to understand any impacts to your taxes.

Before investing, carefully consider the investment objectives, risks, charges, and expenses detailed in a Fund’s prospectus. This document contains important information and must be read carefully prior to investing; you can find the current prospectus by clicking the link on the Fund’s respective page.

Alternative investments are highly risky and may not be suitable for all investors. These investments often involve leveraging, speculative practices, and the potential for complete loss of investment. They typically charge high fees, lack diversification, and can be highly illiquid and volatile. Be aware that both registered and unregistered alternative investments, including Interval Funds, are not subject to the same regulatory requirements as mutual funds, and their illiquid nature may restrict your ability to trade on your timeline. Always review the specific fee schedule for Interval Funds within their prospectus.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Disclaimer: The projections or other information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results.

S&P 500 Index: The S&P 500 Index is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S. It is not an investment product, but a measure of U.S. equity performance. Historical performance of the S&P 500 Index does not guarantee similar results in the future. The historical return of the S&P 500 Index shown does not include the reinvestment of dividends or account for investment fees, expenses, or taxes, which would reduce actual returns.

Mutual Funds (MFs): Investors should read and carefully consider the information contained in the prospectus, which contains the Mutual Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or SoFi's customer service at: 1.855.456.7634. Mutual Funds must be bought and sold at NAV (Net Asset Value); unless otherwise noted in the prospectus, trades are only done once per day after the markets close. Investment returns are subject to risks. Shares may be worth more or less their original value when redeemed. The diversification of a mutual fund will not protect against loss. A mutual fund may not achieve its stated investment objective. Rebalancing and other activities within the fund may have tax implications.

Exchange Traded Funds (ETFs): Before investing in Exchange Traded Funds (ETF), always read the fund's prospectus. It contains important information about the fund’s objectives, risks, and fees. You can get a prospectus from the fund company’s website or by emailing our customer service at [email protected].

Investment Risk: Diversification can help reduce some investment risk, but cannot guarantee profit nor fully protect in a down market.

SOIN-Q226-237