Academic dismissal is when a student is asked to leave a school due to continued poor academic performance. It typically follows a period of probation, which occurs when a student is given a warning and a set amount of time in which they can try to improve their grades and avoid dismissal.

While academic dismissal may seem like the end of the world, it doesn’t mean that the student can never go to college again. It simply means they have to stop attending their current school, at least for a certain period of time. In addition, there are a number of ways to get back on track after a dismissal and either overturn the decision and return to school, or start on a new path that’s a better fit.

• Poor academic performance, such as a GPA below 2.0, can lead to academic dismissal.

• Dismissal impacts financial aid eligibility, which typically requires students to maintain satisfactory academic progress.

• Appealing dismissal involves reflecting on reasons, presenting a sincere case, and showing maturity.

• After dismissal, consider community college, trade schools, or employment as alternative paths.

• Some colleges allow a student to re-apply after academic dismissal, providing they wait a period of time and offer a thoughtful approach to restarting their academic career.

Reasons for Academic Dismissal

Everyone’s academic journey is different, and for some, the transition to college-level work can be more challenging than for others. A student may struggle with grades because they chose a major that’s not compatible with their specific skill set. Or perhaps they faced too many distractions, from personal events or hardships to an overwhelming list of extracurriculars.

When teachers and administrators notice a pattern of poor academic performance, including a GPA below 2.0 or a failure to attain enough credits (as a result of dropping or failing to complete enough courses in a semester), they may put a student on academic probation.

If a student fails to bring up their GPA by the end of their probation period, they may face academic dismissal. Academic probation is not meant to serve as a kind of punishment, but more as a wake-up call to students who are falling seriously behind.

Depending on the school, academic probation may make students ineligible for certain university activities. This makes sense, as probation is meant to be a time to focus seriously on grades in an effort to avoid eventual academic dismissal.

Academic probation or dismissal can also affect a student’s financial aid. The U.S. Department of Education requires students to maintain satisfactory academic progress toward their degrees to receive financial aid — which may include federal, state, and institutional grants and scholarships; work-study; and federal student and parent loans.

There are still options for students who lose their financial aid due to poor academic standing, including some private student loans. Keep in mind, though, that your GPA can also impact your ability to get a private student loan. Each private loan is different, so there’s no one magic number for a student’s GPA. It can be worth shopping around and comparing options from different lenders.

If a student ultimately faces the prospect of academic dismissal, there are multiple routes they can take to try and handle the situation. First, it can be wise to take a moment to reflect on what may have caused the decision to dismiss and reassess one’s priorities. Perhaps a student was up against too much pressure, was pursuing a subject area that didn’t suit them, or had a personal crisis.

If a student decides to appeal the decision, they should be prepared to present a strong and sincere case. Luckily, most schools will allow students to appeal academic dismissal. Most school authorities are receptive to select reasoning or excuses for a poor academic performance. These usually include extenuating circumstances like financial issues, psychological or mental issues, or a family crisis, including an unexpected death in the family.

Approach the case with understanding and humility instead of anger, and try to fight the battle without parents. Students may want to prove that they can handle the stress and academic rigor of college on their own, which involves a certain degree of maturity and independence.

Bouncing Back After Being Dismissed

There’s a lot you can learn from an academic incident like probation or dismissal, and ultimately, it can help you become a better and more dedicated student.

Applying to college after academic dismissal can be a good idea, but only if a student has taken the time to reflect and is ready to make a fresh start. This is especially true if a student is re-applying to the same school.

Some schools will require that students wait at least a year before re-applying, and some will have students show that they’ve received a certain number of credits from community college while on hiatus from the institution. Research each school’s particular policy on reapplying before taking any specific measures.

It can be helpful to talk to professors and academic counselors to determine if going back to college is the right decision and if so, if a student should re-apply to the same school.

It can also be helpful to research schools that have lenient policies around past dismissals when looking to re-apply to school.

College is not for everyone. Other options may include getting a job, pursuing a trade at trade school, or completing an apprenticeship. There’s not one route to a career, so bouncing back may look a little different for everyone.

The Takeaway

It’s important to handle academic probation and dismissal thoughtfully and methodically, assessing all available options and identifying the issues that may have caused a student to fall behind in the first place. If college is still on the table, set a goal to improve grades, whether through tutoring, time management strategies, or a peer study group. Also look into what’s required in terms of getting or regaining financial aid.

If you’ve exhausted all federal student aid options, no-fee private student loans from SoFi can help you pay for school. The online application process is easy, and you can see rates and terms in just minutes. Repayment plans are flexible, so you can find an option that works for your financial plan and budget.

Cover up to 100% of school-certified costs including tuition, books, supplies, room and board, and transportation with a private student loan from SoFi.

FAQ

What is academic dismissal?

Academic dismissal occurs when a student is required to leave a college due to continued poor academic performance.

Will I be warned before academic dismissal?

Yes, typically a student is put on academic probation prior to academic dismissal. This is a warning period during which grades must be improved to continue as a student at the school.

Does academic dismissal mean I can’t go back to my school?

When academic dismissal occurs, some colleges may allow you to reapply after a specific period of time and by showing why you are now qualified to return to your studies. It’s worthwhile to check with a school about their policy if you are at risk of academic dismissal.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loans are subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, the student's at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change. This information is current as of 4/22/2025 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

While many med school students eventually may earn six figures or more, they also can expect to graduate with student debt that averages close to a quarter of a million dollars. According to the Education Data Initiative (EDI), the average medical school debt for students is $234,597.

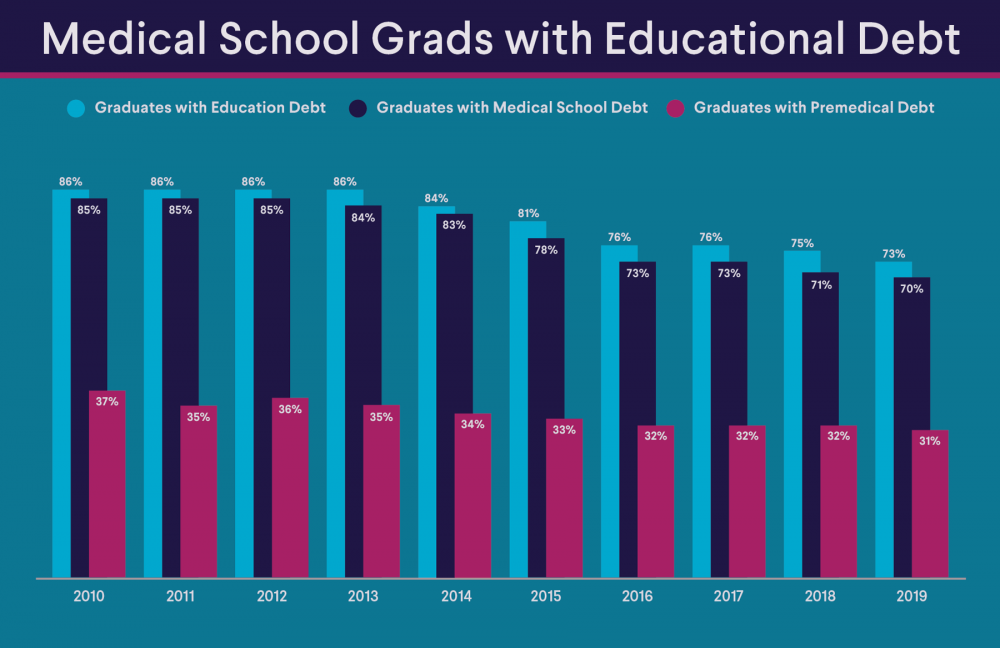

And that’s just what these graduates owe for their medical school education. EDI found that 31% of indebted medical school graduates also have premedical education debt to pay for.

Because of the high cost of medical school debt, it’s crucial for aspiring and current medical school students and graduates to understand their debt repayment options.

• The average medical school debt for graduates in 2024 was reported at $234,597, contributing to a total education debt of approximately $264,519 when including premedical loans.

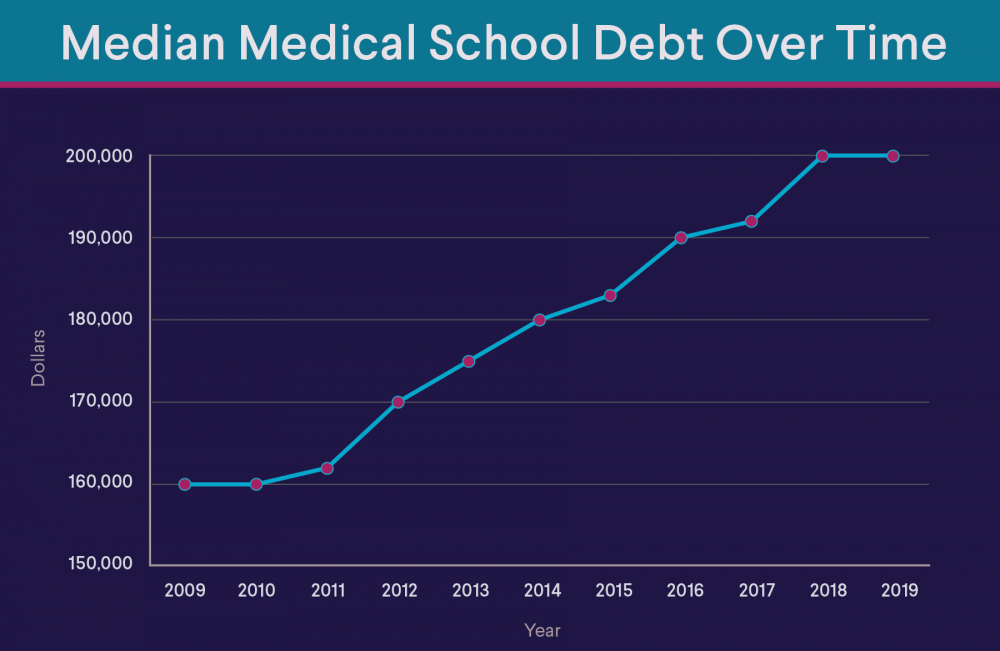

• Average medical school debt increased by 48.5% between 1998 and 2019.

• Federal student loans currently available for medical students include Direct Unsubsidized Loans and Grad PLUS loans, but Grad PLUS Loans will be eliminated as of July 1, 2026.

• Graduates facing high debt can consider options like deferment, income-driven repayment, refinancing, or loan consolidation to help manage their financial burden.

• A disparity in student debt exists among medical schools, with some institutions leading to significantly higher debt levels compared to others, highlighting the variability in medical education costs.

Medical School Debt Statistics

Here’s a snapshot of what the average medical school debt can look like for graduates, based on a roundup of the most recent statistics available:

• According to a 2024 report by EducationData.org, medical school graduates had, on average, $264,519 in total education debt (premed and medical school). Compare that with the average educational debt for the class of 1999-2000: $87,020.

• When the Association of American Medical Colleges (AAMC) looked at members of the class of 2020 who took out educational loans (the most recent data available), it found that:

◦ 5.4% borrowed $1 to $49,999 for premed studies and medical school

◦ 6.1% borrowed $50,000 to $99,999

◦ 8.2% borrowed $100,000 to $149,999

◦ 13.7% borrowed $150,000 to $199,999

◦ 25.1% borrowed $200,000 to $299,999

◦ 11.2% borrowed $300,000 to $399,999

◦ 2.9% borrowed $400,000 to $499,999

• Between 1998 and 2019, average medical school debt increased by 48.5%.

The increase in medical school debt is due to a number of factors, including the cost of education, the type of medical specialty a student chooses, years spent training, and relocating for a residency, among others.

Tuition and Fees

The cost of medical school increased 39% between 2001 and 2024, according to EDI. The average cost of tuition and fees for a first-year medical student in the 2023-2024 school year was $58,327. The average price of medical application fees alone was almost $3,000 in 2023.

The cost of tuition and fees can vary widely depending on whether a medical student attends a public or private university. According to the AAMC, the average cost of tuition and fees at private schools is more than $60,000 yearly. At public schools, the cost is approximately $41,000 for in-state students.

Cost of Living and Relocation

In addition to tuition and fees, medical students also need to cover cost-of-living expenses, such as housing, food, transportation, and books and other supplies needed for classes. Depending where the student goes to school, these expenses can add upward of $10,000 to the total cost of medical schooling.

When a med student is ready to begin their residency, it will typically involve relocating to another city. Along with travel expenses involved with applying for residency, a medical student will also likely need to pay for movers or to ship their belongings, rent for a new place to live (which typically involves a security deposit), and any necessary fees to hook up utilities and so on. If a med student is doing their residency in a big city, the cost for everything from food to rent may be more expensive as well.

Choice of Specialization

The area of medicine a medical student chooses to specialize in can also impact the average cost of medical school. Certain specialties require longer and more specialized training. For example, med students who want to become surgeons typically need to do an extended residency of five to seven years, compared to three to five years of residency for those studying to become primary care physicians. This can result in a higher overall cost for borrowers in specialties and sub-specialties of medicine.

What Does This Mean for Borrowers?

With all these expenses to cover, many aspiring doctors turn to student loans when they’re trying to figure out how to pay for medical school. Data from EDI shows that 70% of medical school students take out loans to help with medical school costs specifically.

It’s important to note that when it comes to borrowing for medical school, loan terms and conditions offered by the federal government might be different from borrowing as an undergrad. This is one of the basics of student loans that it’s helpful to understand when it comes to the average medical school debt.

Some med students may benefit from finding scholarships and loan forgiveness programs that may cut their costs substantially. But many will end up making loan payments for years — or even decades.

So what does the average debt after medical school look like? According to EDI, the average doctor will ultimately pay from $135,000 to $440,000 for their educational loans, with interest factored in.

Due to upcoming changes to student loans as part of the domestic policy bill that was signed in July 2025, there will be just one type of federal student loan available to medical students as of July 1, 2026 — the Direct Unsubsidized Loan.

Another type of federal student loan that has previously been available to those going to medical school, the Grad PLUS Loan, will be eliminated for new borrowers on July 1, 2026.

Instead graduate students will have new lending limits through the Direct Unsubsidized Loan program. This includes an annual limit of $20,500 for graduate students with a $100,000 lifetime limit. Professional students, such as medical students, may qualify for a Direct Unsubsidized Loan with a yearly limit of $50,000 and a lifetime limit of $200,000.

However, those who already have Grad PLUS Loans before the changes take place, can continue to borrow money under the current limits for three additional academic years.

Medical students also can apply for private student loans to help cover their average medical student debt. Generally, borrowers need a solid credit history for private student loans, among other financial factors that will vary by lender. Private lenders offer different rates, terms, and conditions, so it can be worthwhile to shop around.

Just be aware that federal loans currently come with many student protections and benefits that private loans don’t, such as the Public Service Loan Forgiveness program and income-driven repayment.

Temporarily delaying payments while in school may seem like a good idea during a stressful time, but delaying can be costly. During student loan deferment, most Direct Unsubsidized Loans and Direct PLUS loans continue to accrue interest. The problem those in medical fields can face is debt accumulation during their residency, which can last anywhere from three to seven years.

Even while making a modest income — in 2024, the average resident earned $70,000, according to Medscape — the debt would grow considerably.

If your loans are in deferment, making interest-only payments and putting that money toward student loans can reduce the amount of interest that could be added to the loan.

Income-Driven Repayment

Medical residents who can’t afford full payments may want to consider an income-driven repayment (IDR) plan. These plans are designed to make student loan payments more manageable by basing monthly payments on the borrower’s discretionary income and family size.

As of August 2025, there are three income-driven repayment plans you can enroll in, but only one of them — the Income-Based Repayment (IBR) Plan — may allow borrowers to have the outstanding balance of their loan forgiven after 20 years.

However, the new U.S. domestic policy bill will eliminate a number of student loan repayment plans. For borrowers taking out their first loans on or after July 1, 2026, there will be only one repayment option that is similar to the current IDR plans: the Repayment Assistance Program (RAP). On RAP, payments range from 1% to 10% of a borrower’s adjusted gross income for up to 30 years. At that point, any remaining debt will be forgiven. If a borrower’s monthly payment doesn’t cover the interest owed, the interest will be cancelled.

Refinancing Loans

Refinancing medical school loans to help cover the average medical student debt is an option during residency, after residency, or both.

Refinancing student loans with a private lender might help save you money if you can get a lower interest rate than the rates of your current student loans.

Student loan refinancing means paying off one or more of your existing student loans with one new loan. An advantage of refinancing student loans is that you’ll only have one monthly payment to make.

If you refinance your student loans and get a better rate, you could choose a term that allows you to pay off the loan more quickly if you’re able to shoulder the payments, which should save you on interest.

However, refinancing federal loans isn’t a good fit for those who wish to take advantage of federal programs and protections. Refinancing federal loans means you no longer have access to these benefits.

Consolidating Loans

The federal government offers Direct Consolidation Loans through which multiple eligible federal student loans may be combined into one. The interest rate on the new loan is the weighted average of the original loans’ interest rates, rounded up to the nearest one-eighth of a percentage point.

If your payment goes down, it’s likely because the term has been extended from the standard 10-year repayment to up to 30 years on the consolidation loan. Although you may pay less each month, you’ll be paying more in interest over the life of your loan.

Schools With the Highest Student Debt

When it comes to student debt, all medical programs are not equal. According to U.S. News and World Report’s “Best Grad School” rankings, the range can be extensive. Out of 122 medical schools listed, the three that left grads with the most debt in 2022 (the most recent year available) were:

• Nova Southeastern University Patel College of Osteopathic Medicine (Patel) in Fort Lauderdale, Florida: $322,067

• Western University of Health Sciences in Pomona, California: $281,104

• West Virginia School of Osteopathic Medicine in Lewisburg, West Virginia: $268,416

On the other end of the spectrum, the school that graduated students with the least amount of debt was the University of Houston Tilman J. Fertitta Family College of Medicine, with about $34,000 of debt, according to a 2025 report by the AAMC.

Public vs. Private Medical School

The cost of attending a private medical school is typically higher than a public school.

According to EDI, these were the average yearly costs of tuition and fees based on the type of school.

• Public medical school: $53,845

• Private medical school: $67,950

• Public school, in-state resident: $52,107

• Public school, nonresident: $67,348

However, EDI also found that the average cost of an out-of-state education has decreased; whereas costs for in-state public schools have risen by more than 10%.

Strategies for Minimizing Medical School Debt

For medical students looking for ways to reduce the amount of debt they accumulate, there are some programs that can help. Here are two options to explore.

Scholarships and Grants

There are many scholarships and grants available to medical school students to help reduce the average cost of medical school. In fact, some of the top medical school scholarships are worth thousands of dollars to those who qualify.

Scholarships are offered by the federal government, state governments, private organizations, and even medical schools. Cast a wide net to search for a scholarship you may be eligible for.

Service-Based Loan Forgiveness Programs

Medical students may also be eligible to have their student loans forgiven. For example, there are loan repayment programs for those in the medical field who choose to work in an underserved area and/or medical specialty.

The National Health Service Corps Loan Repayment Program offers doctors and other eligible health care providers an opportunity to have their qualifying federal or private student loans repaid while serving in communities with limited access to care.

Medical professionals in a variety of fields, including pediatric research, health disparities research, and clinical research, may be eligible for the National Institutes of Health (NIH) Loan Repayment Programs. Payments may be up to $50,000 annually and can be applied to qualifying federal or private educational debt.

And the Public Service Loan Forgiveness (PSLF) program may be an option for doctors who work in public service careers. If they work full-time for a qualifying government, nonprofit, or public health employer and make 120 qualifying student loan payments, borrowers may be eligible to have their remaining federal Direct loan balance erased.

The Takeaway

Studying medicine can lead to a lucrative career, but the expense involved can be daunting. When the average debt of a medical student tops $230,000 (excluding undergraduate debt), some aspiring and newly minted doctors will want to look for a remedy, stat. Options to help make payments more manageable include income-driven repayment, federal Direct Loan Consolidation, and refinancing.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

With SoFi, refinancing is fast, easy, and all online. We offer competitive fixed and variable rates.

FAQ

How long does it take to pay off medical school debt?

The time to pay off medical school debt varies widely, typically ranging from approximately eight to 25 years. Factors include the total debt amount, income, repayment plan, and any loan forgiveness programs. Many doctors aim to pay off their debt within 10 years, but it can take longer depending on individual circumstances.

Is medical school worth it financially?

Medical school can be financially worthwhile due to the high earning potential of physicians. However, it often comes with significant debt. The return on investment depends on factors like specialty choice, career path, and personal financial management. Many find it worth it, but it’s a complex decision.

How can you pay off medical school debt faster?

To pay off medical school debt faster, consider strategies like living frugally, maximizing income through high-paying specialties, refinancing loans, and exploring loan forgiveness programs. Creating a strict budget and making extra payments may also accelerate the process.

What is the average debt for medical students who attend private institutions?

The average debt for medical students in the class of 2024 who attended private schools is $227,839, according to the American Association of Medical Colleges. By comparison, the average debt for medical students who attend public colleges is $203,606, the AAMC found.

Are there medical schools with lower tuition costs?

Yes, there are medical schools with lower tuition costs. Public medical schools with the lowest annual tuition costs include the University of Texas Austin Dell Medical School ($19,994 for residents and $35,058 for nonresidents), the University of Central Florida Medical School ($29,680 for in-state and $59,241 for out-of-state), and the University of Texas Rio Grande Valley School of Medicine ($21,532 for residents and $34,632 for nonresidents).

The least expensive private schools of medicine are New York University Grossman School of Medicine, which is offering a full tuition scholarship, and Baylor College of Medicine ($19,682 for residents and $32,782 for nonresidents).

SoFi Student Loan Refinance Terms and conditions apply. SoFi Refinance Student Loans are private loans. When you refinance federal loans with a SoFi loan, YOU FORFEIT YOUR ELIGIBILITY FOR ALL FEDERAL LOAN BENEFITS, including all flexible federal repayment and forgiveness options that are or may become available to federal student loan borrowers including, but not limited to: Public Service Loan Forgiveness (PSLF), Income-Based Repayment, Income-Contingent Repayment, extended repayment plans, PAYE or SAVE. Lowest rates reserved for the most creditworthy borrowers. Learn more at SoFi.com/eligibility. SoFi Refinance Student Loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loans are subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, the student's at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change. This information is current as of 4/22/2025 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Private lenders that refinance student loans base rates they offer on the loan term, the borrower’s risk profile, and a rate index. Typically, the most financially stable applicants get the lowest rates.

When the goal is a lower rate, lower monthly payments, or both, the fixed or variable rate you qualify for makes all the difference. (You can also get a lower rate by refinancing with an extended term, but if you do so you may pay more interest over the life of the loan.)

Here’s a look at what you need to know about how interest rates for student loan refinances work.

Student Loan Refinancing, Explained

When you refinance, you take out a new private loan and use it to pay off your existing federal or private student loans. The new loan will have a new repayment term and interest rate, which hopefully will be better.

Most refinancing lenders offer fixed or variable interest rates and terms of five to 20 years. Shortening or lengthening your existing student loan term or terms can affect your monthly payment and the total cost of your new loan. The two key ways to save money by refinancing are:

• A shorter repayment term

• A lower rate

Then again, someone wanting lower monthly payments might choose a longer term, but that may result in more interest paid over the life of the loan.

There are no fees to refinance student loans. Nor is there any limit to the number of times you can refinance. Lenders will want to see a decent credit score, a stable income, and manageable debt. Adding a cosigner may strengthen your profile.

Student loan consolidation and refinancing are terms that are often used interchangeably, but they are not technically the same thing. In general, consolidation means combining multiple loans to create one simplified payment. However, student loan consolidation most often refers to a federal program that allows you to combine multiple types of federal student loans into a single loan. The new loan will have a new term of up to 30 years, but the new rate will not be lower.

However, student loan consolidation most often refers to a federal program that allows you to combine multiple types of federal student loans into a single loan. The new loan, called a Direct Consolidation Loan, will have a new term of up to 30 years, but the new interest rate will not be lower.

Refinancing of student loans is offered by private lenders, such as banks and credit unions. Federal and/or private student loans are refinanced into a new loan that ideally has a better rate; you can refinance a single loan, or consolidate multiple loans into a single new loan through this refinancing process.

If you refinance federal student loans privately, you lose access to federal repayment plans, forgiveness programs, and other benefits.

What Are Interest Rates?

Interest rates are the amount lenders charge individuals to borrow money. When you take out a loan, you must pay back the amount you borrowed, plus interest, usually represented by a certain percentage of the loan principal (the amount you have remaining to pay off).

When interest rates are high, borrowing money is more expensive. And when interest rates are low, borrowing can be cheaper.

Interest rates can be fixed, variable, or a hybrid. For fixed interest rates, lenders set the rate at the beginning of the loan, and that rate will not change over the life of the loan.

A variable interest rate is indexed to a benchmark interest rate. As that benchmark rises or falls, so too will the variable rate on your loan. Variable-rate loans may be best for short-term loans that you can pay off before interest rates have a chance to rise.

Hybrid rates may start out with a fixed interest rate for a period of time, which then switches to a variable rate.

How Is Interest Rate Different From APR?

While interest rate refers to the monthly amount you’ll need to pay to borrow money, annual percentage rate (APR) represents your interest rate for an entire year and any other costs and fees associated with the loan.

As a result, APR gives you a better sense of exactly how expensive a loan might be and helps when comparing loan options.

What Factors Influence Student Loan Interest Rates?

Interest rates for federal student loans are set by Congress and change each year. Federal loans use the 10-year Treasury note as an index for interest rates. These rates apply to all borrowers.

Private lenders, on the other hand, will look at other factors when determining interest rates, such as credit score and credit history. Their interest rates are not governed by legislation so rates can be higher or lower than the federal one, depending on the type of loan and terms. Prevailing interest rates, however, still play a big factor since they change annually.

Typically, lenders see those with higher scores as more likely to pay off their loans on time, and may reward this with lower interest rates. Lenders see borrowers with lower scores as being at greater risk of defaulting on their loans. To offset the risk, they tend to offer higher interest rates.

Some lenders offer a rate discount if you sign up for their autopay program.

What Drives Student Loan Refinancing Rates?

Student loan refinancing rates are driven by many of the same factors that drive rates on your initial loan, such as credit score and credit history. You may want to consider refinancing during an era of low rates or if your financial situation has improved. For example, if you’ve increased your income or you’ve paid off other debts and your credit score received a boost, you may look into refinancing your loans at a lower interest rate.

Many graduates haven’t had much time to build a credit history. A cosigner with good credit may help an individual qualify for a refinance at a lower rate. Cosigners share responsibility for loan payments, of course. So if you miss a payment, they’ll be on the hook.

Refinance Student Loans With SoFi

You might choose to refinance student loans when interest rates are relatively low or your financial situation has improved, potentially providing access to a new private student loan at a lower rate.

Refinancing may be a good move for borrowers with higher-interest private student loans and those with federal student loans who don’t plan to use federal programs like income-driven repayment, Public Service Loan Forgiveness, or forbearance.

A student loan refinancing calculator can help you determine how much you might save by refinancing your student loans. You can compare your options on different loan terms while keeping in mind that a longer term could increase your total interest costs.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

With SoFi, refinancing is fast, easy, and all online. We offer competitive fixed and variable rates.

FAQ

How are student loan refinancing rates calculated?

Lenders base interest rates largely on factors like an applicant’s credit history, income, debt, and prevailing interest rates which change annually.

Does refinancing save you money?

When you refinance your student loans with a new loan at a lower interest rate, you will pay less interest over the life of the loan, given the same or similar loan terms.

What is an average interest rate for student loans?

The average interest rate among all student loans, federal and private, is 5.80%, according to Education Data Initiative researchers. Private student loan rates have a wide range for fixed- and variable-rate loans and generally run from 3.19% to 17.95%.

For the 2025-2026 school year, the interest rate on Direct Subsidized or Unsubsidized loans for undergraduates is 6.39%, the rate on Direct Unsubsidized loans for graduate and professional students is 7.94%, and the rate on Direct PLUS loans for graduate students, professional students, and parents is 8.94%. The interest rates on federal student loans are fixed and are set annually by Congress.

Photo credit: iStock/Kateryna Onyshchuk SoFi Student Loan Refinance Terms and conditions apply. SoFi Refinance Student Loans are private loans. When you refinance federal loans with a SoFi loan, YOU FORFEIT YOUR ELIGIBILITY FOR ALL FEDERAL LOAN BENEFITS, including all flexible federal repayment and forgiveness options that are or may become available to federal student loan borrowers including, but not limited to: Public Service Loan Forgiveness (PSLF), Income-Based Repayment, Income-Contingent Repayment, extended repayment plans, PAYE or SAVE. Lowest rates reserved for the most creditworthy borrowers. Learn more at SoFi.com/eligibility. SoFi Refinance Student Loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Can you pay off someone else’s loan? As a general rule, yes — so if you’re a student loan borrower and someone offers you assistance in paying off your loans, you may want to take them up on it.

However, it’s important to understand the implications. While a parent, grandparent, or even a mysterious benefactor could pay off your student loans, they may be responsible for a gift tax if they contribute more than the annual limit. The gift could also come with emotional strings attached.

Read on to learn about the tax implications of paying off someone else’s student loans — and how to repay your loans if the responsibility is all yours.

• If someone pays off your student loans, they may face a gift tax if the amount exceeds the annual IRS exclusion limit.

• Employers can contribute to your student loans without it counting as taxable income, up to a certain amount per year.

• Payments made by parents or others directly to the loan servicer do not count as taxable income for the recipient.

• Gift tax implications apply if a single individual gifts more than $19,000 in one year, but actual tax liability may depend on lifetime gift amounts.

• Ways to pay off your student loans include student loan consolidation, student loan forgiveness, student loan refinancing, and income-driven repayment plans.

Student Loan Repayment

Repaying student loans is a significant financial commitment that requires careful planning and management. After graduation, most federal student loans enter a grace period, typically lasting six months, during which no payments are required. This grace period allows you to get settled into your post-graduation life and start preparing for regular monthly payments. Once the grace period ends, you will begin making payments according to the repayment plan you have chosen.

The standard repayment plan is a fixed monthly payment over 10 years, but there are several other options available to accommodate different financial situations, including income-driven repayment plans.

Common Repayment Scenarios Involving Third Parties

Third parties, such as family members, friends, or employers, can play a significant role in helping borrowers pay off their student loans.

For instance, parents or grandparents might choose to make payments directly to the loan servicer, or they could gift money to the borrower to be used for loan repayment.

Employers may offer student loan repayment assistance as part of their benefits package, contributing a set amount each month or year toward the borrower’s loans. Through CARES Act legislation, employers can contribute up to $5,250 per employee per year toward student loans without the payment counting toward the employee’s taxable income, through 2025.

While these third-party contributions can be a huge relief, it’s important for borrowers to communicate clearly with their servicers and ensure that payments are applied correctly to avoid any administrative issues.

Tax Implications of Employer Student Loan Assistance

Employer-provided student loan assistance can offer significant financial relief, but it also comes with potential tax implications. As of 2023, the first $5,250 of employer contributions toward an employee’s student loans is tax-free. Any amount above this threshold is considered taxable income and must be reported on the employee’s W-2 form. This means that the employee will owe income tax on the additional amount, which could affect their overall tax liability.

Can Parents Pay Off Their Child’s Student Loans?

Yes, they can. But can parents pay off student loans without a gift tax? It depends. If a parent is a cosigner, paying the student loans in full will not trigger a gift tax. In the mind of the IRS, the parent is not providing a gift but is paying off a debt.

However, if a parent is not a cosigner, a gift tax could be triggered, depending on how much they pay.

How the Gift Tax Works

The gift tax applies to the transfer of any type of property (including money), or the use of income from property, without expecting to receive something of at least equal value in return, the IRS says — adding that if you make an interest-free or reduced-interest loan, you may be making a gift.

There are some exceptions. Gifts between spouses aren’t included in the gift tax. That means if you are married and your spouse pays off your loans, that would not trigger a gift tax event.

Tuition paid directly to qualifying educational institutions in the United States or overseas is also not subject to gift tax, but student loans are different.

The annual exclusion for gifts is $19,000 in 2025. That means an individual can give you up to $19,000 without triggering the gift tax, which the givers, not receivers, generally pay. If your parents file taxes jointly, they would be able to give a combined $38,000 a year, which could include paying down loans. Borrowers who have the good fortune to snag $19,000 from mom, dad, granddad, and grandma could get a total of $76,000 without any family member having to file a gift tax return.

As stated, the annual gift tax exclusion for 2025 is $19,000. However, a gift of more than $19,000 towards your student loans doesn’t mean that your benefactor is on the hook for paying a tax on their gift.

The excess amount just gets added to the lifetime exclusion — currently set at $13.99 million. As long as the benefactor’s total lifetime gifts are below that amount, they don’t have to worry about paying a gift tax. Still, if bumping against that lifetime exclusion is a concern, they can spread out their support over the years to avoid gifting you more than $19,000 in a calendar year.

Filing Requirements for Gifts Over the Limit

When an individual gives a gift that exceeds the annual exclusion limit, they are required to file a gift tax return, Form 709, with the IRS.

If the total value of gifts given over the years, including the current gift, does not exceed this lifetime exemption of 13.99 million, no gift tax will be due. However, failing to file the required return can result in penalties and interest. Therefore, it’s essential for individuals who make large gifts to stay informed about these requirements and to consult with a tax professional to ensure compliance and manage their tax obligations effectively.

What Happens When Someone Pays Off Student Loans For You?

• Paying you, with the expectation you will pay the lender

But if someone pays off your debt, is that income? Once another person has paid off your student loans, it’s as if you had paid them off yourself. You would not have any tax liability.

Financial and Tax Consequences

When someone pays off a student loan on your behalf, the financial and tax consequences can vary. Financially, the immediate benefit is the reduction or elimination of your debt, which can build your credit score, free up cash flow, and reduce financial stress.

However, from a tax perspective, the situation is a bit more complex. If the payment is made by a family member or friend, it is generally considered a gift and is not taxable to you, provided it does not exceed the annual gift tax exclusion limit, which is $19,000 per recipient as of 2025. If the gift exceeds this limit, the giver may need to file a gift tax return, but this typically does not result in immediate tax for the recipient.

If the payment is made by an employer, up to $5,250 of the assistance is tax-free, but any amount above this threshold is considered taxable income to you and must be reported on your W-2.

Impact on Credit and Loan Balances

When someone pays off your student loan, the impact on your credit and loan balances is generally positive. Your loan balance will decrease or be completely eliminated, which can significantly improve your debt-to-income ratio and reduce your monthly financial obligations.

The timely payment of your student loan can have a positive effect on your credit score, as it demonstrates responsible debt management. However, it’s important to ensure that the lender reports the payment to the credit bureaus, as this will help reflect the positive change in your credit report.

Other Options to Pay Off Student Loans

Not everyone has a benefactor, of course. While someone taking your student loan balance down to zero can seem like a dream, there are realistic ways to ease the burden of student loans, no third party required.

The one thing that won’t help: if you stop paying your student loans. Ignoring your student loan payments will result in an increased balance, additional fees, and a lower credit score.

If you hold federal student loans and stop paying them, part of your wages could be garnished, and your tax refund could be withheld. If you default on a private student loan, the lender might file a suit to collect from you.

In other words, coming up with a repayment plan is crucial. Strategies to pay off undergraduate and graduate student loans include student loan consolidation, student loan refinancing, student loan forgiveness, and income-driven repayment plans.

Student Loan Consolidation

If you have federal student loans, you may consider consolidation, or combining multiple loans into one federal loan. The interest rate is the weighted average of all the loans’ rates, rounded up to the nearest one-eighth of a percentage point.

Federal student loan consolidation via a Direct Consolidation Loan can lower your monthly payment by giving you up to 30 years to repay your loans. It can also streamline payment processing.

Consolidating federal loans other than Direct Loans may give borrowers access to programs they might not otherwise be eligible for, including additional income-driven repayment plan options and Public Service Loan Forgiveness.

Student loan forgiveness is a program designed to alleviate the financial burden of student debt for eligible borrowers. These programs are often aimed at individuals who have pursued specific careers in public service, teaching, or other fields that benefit society. To qualify, borrowers typically need to meet certain criteria, such as making a set number of on-time payments and working in a qualifying job for a specified period. The most well-known program is the Public Service Loan Forgiveness (PSLF) program, which forgives the remaining balance of federal student loans after 120 qualifying payments.

Borrowers who take out loans on or after July 1, 2026 can still benefit from PSLF so long as they choose the RAP and not the standard repayment plan.

Another way students can get their loans forgiven is through a disability discharge. Disability discharge is a provision that allows borrowers with total and permanent disabilities to have their federal student loans forgiven. To qualify, borrowers must provide documentation from a physician or the Social Security Administration (SSA) confirming their disability status. Once approved, the borrower’s remaining loan balance is forgiven, and they are no longer responsible for making payments.

Student Loan Refinancing

With student loan refinancing, a borrower takes on one new, private student loan to pay off previous federal and/or private student loans. Ideally, the goal is a lower interest rate. The repayment term might also change.

However, refinancing federal loans means that borrowers will no longer be eligible for federal repayment plans, forgiveness programs, and other benefits. If a borrower needs access to those programs, student loan refinancing won’t make sense.

But for borrowers who have no plans to use the federal programs, a lower rate could make refinancing worthwhile. Using a student loan refinancing calculator can help a borrower see how much money they might save by refinancing one or all of their loans.

Income-driven repayment (IDR) plans are federal student loan repayment options designed to make monthly payments more affordable by basing them on a borrower’s income and family size. These plans typically cap your monthly payment at 5% to 20% of your discretionary income and extend the loan term to 20 or 25 years, depending on the specific plan.

Starting on July 1, 2026, income-driven repayment plans PAYE, ICR, and SAVE will be replaced by a new Repayment Assistance Plan (RAP). The existing IDR plans will be eliminated by July 1, 2028. With RAP, payments range from 1% to 10% of adjusted gross income with terms up to 30 years. After the term is up, any remaining debt will be forgiven.

Refinancing Student Loans With SoFi

Even if your parents, grandparents, or others in your life are not in a position to pay off your student loans for you, understanding your options for potentially lowering your monthly payments or saving money over the life of a loan can give you multiple avenues to explore as you work toward taking control of your finances.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

With SoFi, refinancing is fast, easy, and all online. We offer competitive fixed and variable rates.

FAQ

Can I pay off my child’s student loans?

Yes, you can pay off your child’s student loans. But, depending on the amount, there may be tax implications.

Is paying off a child’s student loans considered a gift?

Yes. Paying student loans for someone else is considered a gift and would incur a gift tax for any gift above $19,000, which is the gift exclusion cutoff for 2025. That means both parents can contribute $38,000 per calendar year toward their child’s student loans without owing gift tax.

Can I pay off my sibling’s student loans?

Yes. You can absolutely win sibling of the year and pay off your sibling’s student loans. Just know that any gift above $19,000 in 2025 will trigger a gift tax that you will be responsible for paying.

Do I owe taxes if someone else pays my student loans?

If someone else pays your student loans, the amount paid may be considered taxable income, especially if it exceeds the annual gift tax exclusion. However, if the payments are made directly to the lender, they are generally not taxable. Always consult a tax professional for specific advice.

Can paying off someone’s loans impact their eligibility for forgiveness programs?

Paying off someone’s loans can impact their eligibility for forgiveness programs, as these programs often require a specific amount of unpaid debt and a history of consistent payments. If the loans are fully paid off, the individual may no longer qualify for forgiveness. Consult the specific program’s rules for details.

Photo credit: iStock/Halfpoint

SoFi Student Loan Refinance Terms and conditions apply. SoFi Refinance Student Loans are private loans. When you refinance federal loans with a SoFi loan, YOU FORFEIT YOUR ELIGIBILITY FOR ALL FEDERAL LOAN BENEFITS, including all flexible federal repayment and forgiveness options that are or may become available to federal student loan borrowers including, but not limited to: Public Service Loan Forgiveness (PSLF), Income-Based Repayment, Income-Contingent Repayment, extended repayment plans, PAYE or SAVE. Lowest rates reserved for the most creditworthy borrowers. Learn more at SoFi.com/eligibility. SoFi Refinance Student Loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Student loan debt can be overwhelming, especially as interest builds and payments drag on for years after graduation. For borrowers seeking relief, one strategy that sometimes comes up is using a personal loan to pay off student loans. On the surface, it may seem like a simple debt-swap — replace one loan with another and, ideally, secure better terms. But is it a smart idea?

While personal loans can be used for many things, they are generally not the best option for paying off student loans. Many lenders prohibit using personal loans for educational costs (including SoFi), which includes paying off student loans. Even if you can find a lender that does allow it, there are pros and cons to using a personal loan to pay off your student loan balance. Here’s what you need to know.

• Many lenders do not allow you to use a personal loan for paying off student loans.

• Personal loans often have higher interest rates and shorter terms than student loans.

• A lower interest rate can sometimes be secured, potentially reducing overall debt costs.

• Federal protections like deferment and forgiveness are lost when using a personal loan.

• Other repayment options, such as federal consolidation loans, student loan refinancing, and income-driven repayment plans, may be a better fit.

Personal Loans vs. Student Loans

At first glance, personal loans and student loans might seem similar. Both provide a lump sum of money up front, require you to pay it back in monthly payments, and charge interest. But the structure, purpose, and protections of each are different.

Student loans are specifically designed to help finance education. They often feature relatively low interest rates and deferred repayment while in school. In the case of federal student loans, they also offer unique benefits like income-driven repayment (IDR) plans, forbearance during hardship, and potential forgiveness programs.

Personal loans, by contrast, are loans that can be used for virtually any legal purpose. Common uses for personal loans include home renovations, unexpected emergencies, medical expenses, major events like weddings, and debt consolidation (when you combine multiple high-interest debts into a single loan with a potentially lower interest rate).

Personal loans tend to carry shorter repayment terms (often two to seven years), and their interest rates can vary widely based on your credit score. Importantly, they don’t offer any of the protections or flexible repayment options that federal student loans provide.

Note: While SoFi personal loans cannot be used for post-secondary education expenses, we do offer private student loans with great interest rates.

Can You Use a Personal Loan to Pay Off Student Loans?

It depends. While it may technically be possible to use a personal loan to pay off your student loans, either federal or private, many lenders do not allow you to use the proceeds of a personal loan for this purpose.

This restriction exists largely due to regulatory and risk concerns. Education-related lending in the U.S. is heavily regulated, and lenders that want to offer student loan refinancing must meet specific legal and compliance standards. To avoid those complications, many personal loan providers choose not to allow their products to be used for anything related to student loans or education.

If you are unsure if a lender will allow you to use the funds to pay off your student debt, it’s a good idea to let them know this is your intent at the outset. This could be a reason why you would be denied for a personal loan. However, if you use the proceeds of a personal loan for a prohibited use, you’ll be violating the loan agreement and might face legal consequences or be required to repay the full amount of the loan immediately.

So while using a personal loan to pay off student debt is theoretically possible, finding a lender that allows it — and does so under favorable terms — could be a major challenge.

Private vs. Federal Student Loans

If you do happen to find a lender that permits this use, it’s crucial to consider what kind of student loans you’re dealing with.

Private student loans often come with fewer borrower protections and may carry higher interest rates than federal loans. If your credit is excellent and the new personal loan offers a better rate and shorter term, using it to pay off private loans could make financial sense — if permitted by the lender.

Federal student loans, however, come with significant advantages that you will lose if you switch to a personal loan. These include access to IDRs, deferment and forbearance options, and the possibility of forgiveness through Public Service Loan Forgiveness (PSLF). Giving up these benefits for a loan that’s less flexible could be risky.

Pros and Cons of Using a Personal Loan to Pay off Student Loans

If you can find a lender that allows it, here are some pros and cons of using a personal loan to pay off student debt.

Pros

• Potentially lower interest rate: If you took out private student loans with a relatively high rate and currently have strong credit, you may be able to qualify for a personal loan with a lower rate than your student loans.

• Predictable payments: If you have a private student loan with a variable interest rate, using a fixed-rate personal loan to pay it off will provide you with a fixed monthly payment, which can make budgeting simpler.

• Faster repayment timeline: Because personal loans usually have shorter terms, using a personal loan to pay off your student debt could help you eliminate your student loan debt more quickly — provided you can afford the higher payments.

Cons

• Loss of federal protections: If you’re paying off federal student loans, you’ll forfeit benefits like IDR plans, deferment, forbearance, and forgiveness opportunities, which can provide a valuable safety net.

• Higher monthly payments: Because personal loans generally have shorter repayment terms than student loans, your monthly payments may be higher, even if the interest rate is lower.

• No tax benefits: You can generally deduct student loan interest, up to $2,500, from your taxable income each year. Interest on personal loans, on the other hand, doesn’t qualify for a similar tax break.

Other Ways to Pay Off Student Loans

If using a personal loan to pay off your student loans isn’t feasible or cost-effective, here are some other student loan repayment options to consider.

Student Loan Refinancing

Student loan refinancing involves taking out a new student loan from a private lender to replace one or more existing loans, ideally at a lower interest rate. Unlike personal loans, there are numerous options available when it comes to finding a lender that will refinance your student loans.

Be aware, though: Refinancing federal loans with a private lender will still eliminate federal protections. Also keep in mind that refinancing student loans for a longer term can increase the overall cost of the loan, since you’ll be paying interest for a longer period of time.

If you have federal loans and your payments are unaffordable, you may qualify for an IDR plan. Generally, your payment amount under an IDR plan is a percentage of your discretionary income and remaining debt may be forgiven after decades of consistent repayment.

Keep in mind that under the new domestic policy bill, many existing federal IDR plans will close by July 1, 2028. After those plans are eliminated, borrowers whose loans were all disbursed before July 1, 2026, can choose between the Repayment Assistance Plan (RAP) and Income-Based Repayment (IBR) plan.

Federal Loan Consolidation

Federal loan consolidation allows you to combine multiple federal loans into a single loan with a weighted average interest rate. Consolidation can simplify repayment and may help you qualify for certain forgiveness programs, but you won’t necessarily save on interest.

Loan Rehabilitation

If your federal loans are in default, loan rehabilitation allows you to make a series of consecutive, agreed-upon payments (usually nine over ten months) to bring your loan current. This also removes the default status from your credit report and restores eligibility for federal benefits. To begin the loan rehabilitation process, you must contact your loan holder.

Currently, borrowers can only use a rehabilitation agreement to remove their loans from default once. Starting July 1, 2027, borrowers will be able to use rehabilitation to exit default twice.

The Takeaway

While the idea of using a personal loan to pay off student loans might seem appealing, it may not be a viable nor an advisable solution. Many lenders prohibit using personal loan funds for education-related expenses, including paying off student loans. Even if you find a lender that allows it, the trade-offs can be significant, especially if you’re dealing with federal student loans.

Instead, you might explore options designed specifically for managing student debt, such as student loan refinancing, consolidation, or enrolling in an income-driven repayment plan. These programs may offer benefits that are better fit to your situation.

Debt repayment strategies are not one-size-fits-all. It’s important to carefully evaluate your options — and read the fine print — before making a move that could impact your financial future for years to come.

While SoFi personal loans cannot be used for post-secondary education expenses, they can be used for a wide range of purposes, including credit card consolidation. SoFi offers competitive fixed rates and same-day funding for qualified borrowers. See your rate in minutes.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. See your rate in minutes.

SoFi’s Personal Loan was named a NerdWallet 2026 winner for Best Personal Loan for Large Loan Amounts.

FAQ

Can you consolidate student loans with a personal loan?

Technically, you might be able to use a personal loan to pay off student loans, but it’s not true consolidation — and many lenders don’t allow it. Personal loan lenders will often explicitly prohibit using loan funds for education-related expenses, including paying off existing student loans. Even if permitted, this route eliminates federal protections like income-driven repayment and forgiveness programs. Alternatives such as federal consolidation or student loan refinancing can be safer and more effective ways to manage or streamline student loan repayment.

What are the risks of using a personal loan to pay off student debt?

Using a personal loan to pay off student debt carries several risks, starting with the fact that many lenders prohibit this use altogether. If you find a lender that allows it, keep in mind that using a personal loan to pay off federal student loans will mean losing federal benefits like income-driven repayment, deferment, forbearance, and loan forgiveness. Personal loans also typically have higher interest rates and shorter repayment terms than student loans, which could increase your monthly payments.

Does paying off student loans with a personal loan hurt your credit?

Many personal loan lenders don’t allow you to use a personal loan to pay off student loans. But if you can find one that does, paying off student loans with a personal loan may impact your credit in several ways.

Initially, your credit could dip temporarily due to the new account and hard inquiry. However, if you make regular, on-time payments, the loan could have a positive influence on your credit profile over time. On the other hand, missed payments could negatively affect your credit. It’s important to consider lender rules and your ability to manage repayment before using a personal loan to pay off student loans.

Are there better options than personal loans for student debt?

Yes, there are a number of options that may be better than personal loans for paying off student loans. Federal consolidation loans can combine multiple federal loans into one, simplifying repayment. Income-driven repayment plans for federal loans adjust payments to your earnings, making them more manageable. Refinancing with a private lender might reduce rates and monthly payments Additionally, some employers offer student loan repayment assistance, which can significantly ease the financial burden.

Can using a personal loan to pay student loans disqualify you from forgiveness programs?

Yes. If you pay off your federal student loans with a personal loan, you’ll forfeit federal benefits like income-driven repayment, deferment, forbearance, and loan forgiveness. The same is true if you refinance your federal student loans with a private student loan lender.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.