Roth IRA Explained

Table of Contents

A Roth IRA is an individual retirement account that allows you to contribute after-tax dollars and then withdraw your money tax-free in retirement. A Roth IRA is different from a traditional IRA in which you contribute pre-tax dollars but owe tax on the money you withdraw in retirement.

A Roth IRA can be a valuable way to help save for retirement over the long-term with the potential for tax-free growth. Read on to learn how Roth IRAs work, the rules about contributions and withdrawals, and how to determine whether a Roth IRA is right for you — just think of it as Roth IRA information for beginners and non-beginners alike.

Key Points

• A Roth IRA is a retirement savings account that offers tax-free growth and tax-free withdrawals in retirement.

• Contributions to a Roth IRA are made with after-tax dollars, and qualified withdrawals are not subject to income tax.

• Roth IRAs have income limits for eligibility, and contribution limits that vary based on age and income.

• Unlike traditional IRAs, Roth IRAs do not entail required minimum distributions (RMDs) during the account holder’s lifetime.

• Roth IRAs can be a valuable tool for long-term retirement savings, especially for individuals who expect to be in a higher tax bracket in the future.

What Is a Roth IRA?

A Roth IRA is a retirement account that provides individuals with a way to save on their own for their golden years.

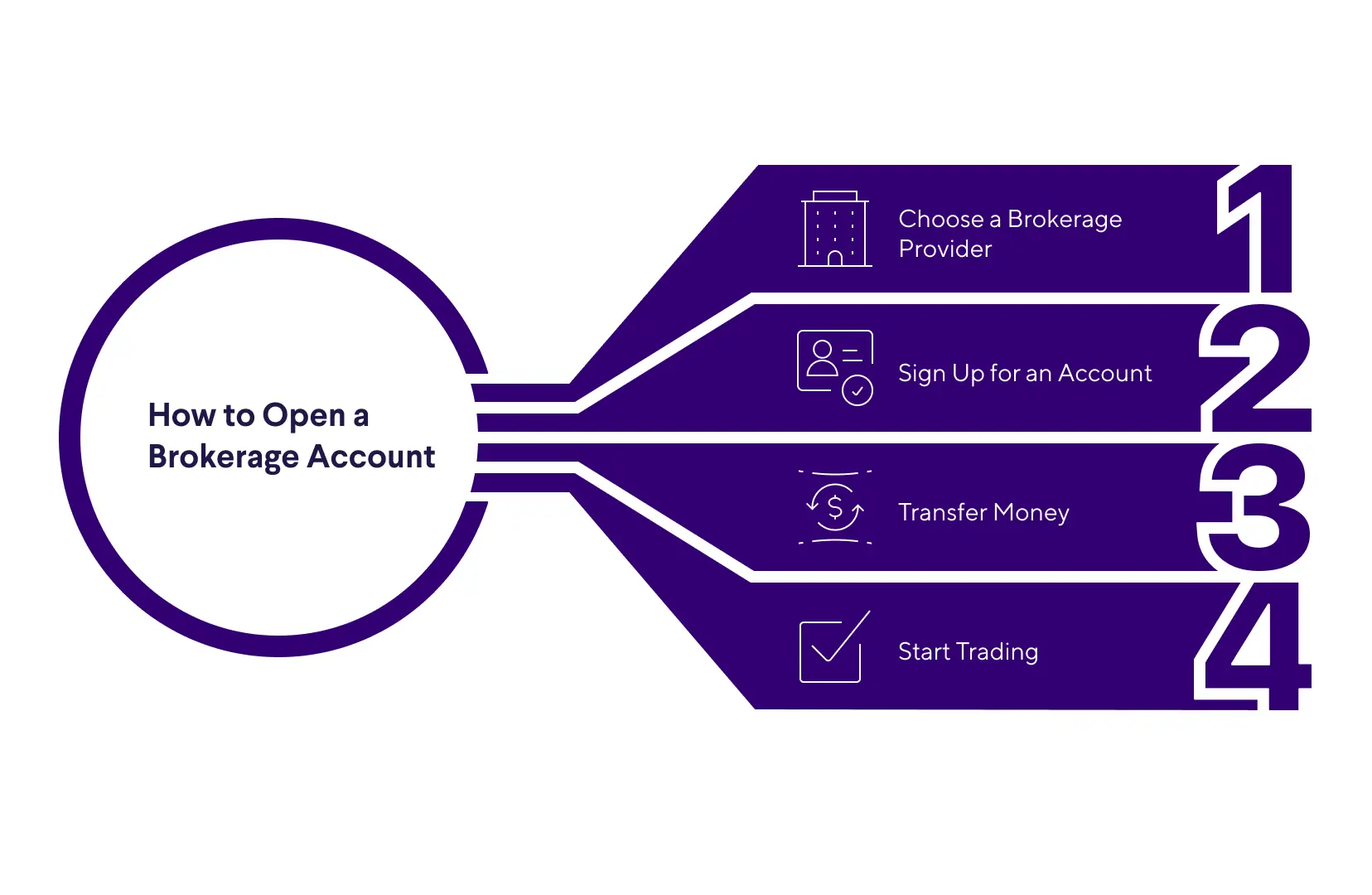

You can open a Roth IRA at most banks, online banks, or brokerages. Once you’ve set up your Roth account, you can start making contributions to it. Then you can invest those contributions in the investment vehicles offered by the bank or brokerage where you have your account.

What differentiates a Roth IRA from a traditional IRA is that you make after-tax contributions to a Roth. Because you pay the taxes upfront, the earnings in a Roth grow tax free. When you retire, the withdrawals you take from your Roth will also be tax free, including the earnings in the account.

With a traditional IRA, you make pre-tax contributions to the account, which you can deduct from your income tax, but you pay taxes on the money, including the earnings, when you withdraw it in retirement.

Roth IRA Contributions

There are several rules regarding Roth IRA contributions, and it’s important to be aware of them. First, to contribute to a Roth IRA, you must have earned income. If you don’t earn income for a certain year, you can’t contribute to your Roth that year.

Second, Roth IRAs have annual contribution limits (see more on that below). If you earn less than the Roth IRA contribution limit for the year, you can only deposit up to the amount of money you made. For instance, if you earn $5,000 in 2025, that is the maximum amount you can contribute to your Roth IRA for that year.

In addition, there are income restrictions regarding Roth IRA contributions.

In 2025, single filers with a modified adjusted gross income (MAGI) of:

• less than $150,000 can contribute the full amount to a Roth

• $150,000 to $165,000 to contribute a reduced amount

• $165,000 or more can’t contribute to a Roth

In 2025, married filers with a MAGI of:

• less than $236,000 can contribute the full amount to a Roth

• $236,000 to $246,000 can contribute a reduced amount

• $246,000 or more can’t contribute to a Roth

In 2026, single filers with a MAGI of:

• less than $153,000 can contribute the full amount to a Roth

• $153,000 to $168,000 can contribute a reduced amount

• $168,000 or more can’t contribute to a Roth

In 2026, married joint filers with a MAGI of:

• less than $242,000 can contribute the full amount

• $242,000 to $252,000 can contribute a reduced amount

• $252,000 or more can’t contribute to a Roth.

Tax Treatment

Contributions to a Roth IRA are made with after-tax dollars — meaning you pay taxes on the money before contributing it to your Roth. You can’t take your contributions as income tax deductions as you can with a traditional IRA, but you can withdraw your contributions at any time with no taxes or penalties. Once you reach age 59 ½ or older, you can withdraw your earnings, along with your contributions, tax-free.

If you expect to be in a higher tax bracket in retirement, or if you want to maximize your savings in retirement and not have to pay taxes on your withdrawals then, a Roth IRA may make sense for you.

Contribution Limits

As mentioned, Roth IRAs have annual contribution limits, which are the same as traditional IRA contribution limits.

For 2025, the annual IRA contribution limit is $7,000 for individuals under age 50, and $8,000 for those 50 and up. The extra $1,000 is called a catch-up contribution for those closer to retirement. For 2026, the contribution limit is $7,500 for those under age 50, and $8,600 for those 50 and up, including a $1,100 catch-up contribution.

Remember that you can only contribute earned income to a Roth IRA. If you earn less than the contribution limit, you can only deposit up to the amount of money you made that year.

Calculate your IRA contributions.

Get a head start on retirement planning with SoFi’s 2024 IRA contribution calculator.

Tax-Free Withdrawals

As noted, you can make withdrawals, including earnings, tax-free from a Roth once you reach age 59 ½. And you can withdraw contributions tax-free at any time. However, there are some specific Roth IRA withdrawal rules to know about so that you can make the most of your IRA.

Qualified Distributions

Since you’ve already paid taxes on the money you contribute to your Roth IRA, you can withdraw contributions at any time without paying taxes or a 10% early withdrawal penalty. But you cannot withdraw earnings tax- and penalty-free until you reach age 59 ½.

For example, if you’re age 45 and you’ve contributed $25,000 to a Roth through your online brokerage over the last five years, and your investments have seen a 10% gain (or $2,500), you would have $27,500 in the account. But you could only withdraw up to $25,000 of your contributions tax-free, and not the $2,500 in earnings.

The 5-Year Rule

According to the 5-year rule, you can withdraw Roth IRA account earnings without owing tax or a penalty, as long as it has been five years or more since you first funded the account, and you are 59 ½ or older.

The 5-year rule applies to everyone, no matter how old they are when they want to withdraw earnings from a Roth. For example, even if you start funding a Roth when you’re 60, you still have to wait five years to take qualified withdrawals.

Non-Qualified Withdrawals

Non-qualified withdrawals of earnings from a Roth IRA depends on your age and how long you’ve been funding the account.

• If you meet the 5-year rule, but you’re under age 59 ½, you’ll owe taxes and a 10% penalty on any earnings you withdraw, except in certain cases, as noted below.

• If you don’t meet the 5-year rule, meaning you haven’t had the account for five years, and if you’re less than 59 ½ years old, in most cases you will also owe taxes and a 10% penalty.

Exceptions

You can take an early or non-qualified withdrawal prior to 59 ½ without paying a penalty or taxes in certain circumstances, including:

• For a first home. You can take out up to $10,000 to pay for buying, building, or rebuilding your first home.

• Disability. You can withdraw money if you qualify as disabled.

• Death. Your heirs or estate can withdraw money if you die.

Additionally you may be able to avoid the 10% penalty (although you’ll still generally have to pay income taxes) if you withdraw earnings for such things as:

• Medical expenses. Specifically, those that exceed 7.5% of your adjusted gross income.

• Medical insurance premiums. This applies to health insurance premiums you pay for yourself during a time in which you’re unemployed.

• Qualified higher education expenses. This includes expenses like college tuition and fees.

Advantages of a Roth IRA

Depending on an individual’s income and circumstances, a Roth IRA has a number of advantages.

• No age restriction on contributions. Roth IRA account holders can make contributions at any age as long as they have earned income for the year.

* You can fund a Roth and a 401(k). Funding a 401(k) and a traditional IRA can sometimes be tricky, because they’re both tax-deferred accounts. But a Roth IRA is after-tax, so you can contribute to a Roth and a 401(k) at the same time and stick to the contribution limits for each account.

• Early withdrawal option. With a Roth IRA, an individual can generally withdraw money they’ve contributed at any time without tax or penalties (but not earnings). In contrast, withdrawals from a traditional IRA before age 59 ½ may be subject to a 10% penalty.

• Qualified Roth withdrawals are tax-free. Investors who have had the Roth for five years or more, and are at least 59 ½, are eligible to take tax- and penalty-free withdrawals of contributions and earnings.

• No required minimum distributions (RMDs). Unlike traditional IRAs, which require account holders to start withdrawing money at age 73, Roth IRAs do not have RMDs. That means an individual can withdraw the money as needed without fear of triggering a penalty.

Disadvantages of a Roth IRA

Roth IRAs also have some disadvantages to consider. These include:

• No tax deduction for contributions. A primary disadvantage of a Roth IRA is that your contributions are not tax deductible, as they are with a traditional IRA and other tax-deferred accounts like a 401(k).

• Higher earners often can’t contribute to a Roth. Individuals with a higher MAGI are generally excluded from Roth IRA accounts, unless they do what’s known as a backdoor Roth or a Roth conversion.

• The 5-year rule applies. The 5-year rule can make withdrawals more complicated for investors who open a Roth later in life. If you open a Roth or do a Roth conversion at age 60, for example, you must generally wait five years to take qualified withdrawals of contributions and earnings or face a penalty.

• Low annual contribution limit. The maximum amount you can contribute to a Roth IRA each year is low compared to other retirement accounts like a SEP IRA or 401(k). But, as noted above, you can combine saving in a 401(k) with saving in a Roth IRA.

Roth IRA Investments

How does a Roth IRA make money? Once you contribute money to your IRA account you can invest those funds in different assets such as mutual funds, exchange-traded funds (ETFs), stocks, and bonds. Depending on how those investments perform, you may earn money on them (however, no investment is guaranteed to earn money). And if you leave your earnings in the account, you can potentially earn money on your earnings through a process called compounding returns, in which your money keeps earning money for you.

To choose investments for your Roth IRA, consider your financial circumstances, goals, timeframe (when you will need the money), and risk tolerance level. That way you can determine which investment options are best for your situation.

Is a Roth IRA Right for You?

How do you know whether you should contribute to a Roth IRA? This checklist may help you decide.

• You might want to open a Roth IRA if you don’t have access to an employer-sponsored 401(k) plan, or if you do have a 401(k) plan but you’ve already maxed out your contribution to it. You can fund both a Roth IRA and an employer-sponsored plan.

• Because Roth contributions are taxed immediately, rather than in retirement, using a Roth IRA can make sense if you are in a lower tax bracket currently. It may also make sense to open a Roth IRA if you expect your tax bracket to be higher in retirement than it is today.

• Individuals who are in the beginning of their careers and earning less might consider contributing to a Roth IRA now, since they might not qualify under the income limits later in life.

• A Roth IRA may be helpful if you think you’ll work past the traditional retirement age, as long as your income falls within the limits. Since there is no age limit for opening a Roth and RMDs are not required, your money can potentially grow tax-free for a long period of time.

The Takeaway

A Roth IRA can be a valuable tool to help save for retirement. With a Roth, your earnings grow tax-free, and you can make qualified withdrawals tax-free. Plus, you can withdraw your contributions at any time with no taxes or penalties and you don’t have to take required minimum distributions (RMDs).

That said, not everyone is eligible to fund a Roth IRA. You need to have earned income, and your modified adjusted gross income cannot exceed certain limits. You must fund your Roth for at least five years and be 59 ½ or older in order to make qualified withdrawals of earnings. Otherwise, you would likely owe taxes on any earnings you withdraw, and possibly a penalty.

Still, the primary advantage of a Roth IRA — being able to have an income stream in retirement that’s tax-free — may outweigh the restrictions.

Prepare for your retirement with an individual retirement account (IRA). It’s easy to get started when you open a traditional or Roth IRA with SoFi. Whether you prefer a hands-on self-directed IRA through SoFi Securities or an automated robo IRA with SoFi Wealth, you can build a portfolio to help support your long-term goals while gaining access to tax-advantaged savings strategies.

FAQ

Are Roth IRAs insured?

If your Roth IRA is held at an FDIC-insured bank and is invested in bank products like certificates of deposit (CDs) or money market account, those deposits are insured up to $250,000 per depositor, per institution. On the other hand, if your Roth IRA is with a brokerage that’s a member of the Securities Investor Protection Corporation (SIPC), and the brokerage fails, the SIPC provides protection up to $500,000, which includes a $250,000 limit for cash. It’s very important to note that neither FDIC or SIPC insurance protects against market losses; they only cover losses due to institutional failures or insolvency.

How much can I put in my Roth IRA monthly?

For tax year 2025, the maximum you can deposit in a Roth or traditional IRA is $7,000, or $8,000 if you’re over 50. For tax year 2026, the maximum you can contribute is $7,500, or $8,600 if you’re age 50 or older. How you divide that per month is up to you. But you cannot contribute more than the annual limit.

I opened a Roth IRA — now what?

After you open a Roth IRA, you can make contributions up to the annual limit. Then you can invest those contributions in assets offered by your IRA provider. Typically you can choose from such investment vehicles as mutual funds, exchange-traded funds, stocks and bonds.

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOIN-Q424-108

CN-Q425-3236452-07