Understanding the Basics of Real Estate Options

Editor's Note: Options are not suitable for all investors. Options involve risks, including substantial risk of loss and the possibility an investor may lose the entire amount invested in a short period of time. Please see the Characteristics and Risks of Standardized Options.

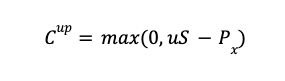

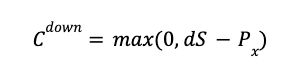

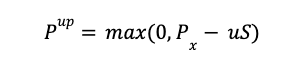

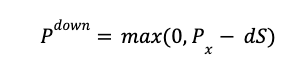

Another way to invest in real estate is through buying or selling real estate options. With an options contract, a buyer is granted the right to purchase a property for a specific price by a specific date, but they are not obligated to buy it.

In order to purchase this option, the buyer of the contract pays the seller a premium.

This is a flexible and typically less expensive way to enter the real estate market that may also help reduce risks involved in single property investment.

What Are Real Estate Options?

Real estate options are contracts between a potential buyer and seller. They grant the buyer the exclusive right to purchase a particular property within terms set in the contract. But the buyer doesn’t have to purchase the property.

However, if the buyer decides to exercise the option and purchase the property, the seller is obligated to sell the property at the agreed-upon price. Once the agreement is entered into, the property owner can’t sell to anyone else within the time period set in the option.

An options contract for a purchase is also known as a call option, whereas an option to sell would be called a put option.

Recommended: Call vs Put Options: Main Differences

How Do Options in Real Estate Work?

Generally, real estate options set a particular purchase price and are valid for anywhere from six months to one year. The buyer doesn’t have to purchase the property, but if they want to, the seller is obligated to sell to them even if the market price has gone up.

The buyer pays what is known as a “premium” in options terminology to enter into the contract. If they decide not to buy the property, the property owner (the seller) keeps that premium.

Real estate options are most often used in commercial real estate, but they can be used by retail investors as well. They aren’t sold on exchanges, and each contract is specific for the property it represents. Usually a contract is only for a single property, not multiple properties.

Real estate options are similar to stock options in that they set a specific price, premium, and period of time for a contract related to an underlying asset. Options can be exercised early or at the expiration date. They can also be sold to another investor.

• Most of the benefits involved in real estate options tilt in the buyer’s favor.

• If the property value goes up a few months into the contract, the buyer can exercise the contract and purchase the property, and sell it for a profit.

• If the property value drops, the buyer can simply let the option expire — thus losing only the premium they paid, which is typically a small percentage of the value of the underlying asset or property in this case.

If the buyer decides not to exercise the contract, they can sell it to another buyer at a potentially higher premium (and pocket the difference).

For a seller, there is the potential for them to make a profit if the buyer exercises their option to purchase the property. They may also profit if the buyer doesn’t exercise the option — at which point they can keep the premium amount, and then sell the contract (or the property) to someone else.

💡 Quick Tip: Options can be a cost-efficient way to place certain trades, because you typically purchase options contracts, not the underlying security. That said, options trading can be risky, and best done by those who are not entirely new to investing.

Lease Options

In addition to real estate options for purchases, there are also lease options. These are rent-to-own agreements between a buyer and seller. They let someone lease a property with the option to buy it after a certain amount of time, but not the obligation.

Generally with a lease option, some or all of the rental payment goes towards the purchase. Some lease options lock in a particular price, but others just give the buyer the exclusive right to buy at whatever the market price is.

Although lease options can be great for buyers, they are also more expensive than simply renting a property since they involve a premium. For this reason, it’s important for a buyer to carefully consider the contract and their future plans before entering into a lease option agreement.

2 Advantages of Real Estate Options for Buyers

Options are a common investing strategy for commercial real estate investors. There are several reasons a buyer might enter into a real estate option contract with a seller.

It Can Allow Time for the Buyer to Amass Funds

One might choose a real estate option if they want to secure a piece of land or property at a certain price but they need some time to get funds in order for the purchase.

A Real Estate Option Locks in a Price

If a buyer thinks the price of a property might go up, they can purchase an option to lock in the current market price. However, some real estate options are not completely set in their sale prices. There may be clauses in the contract to determine what the final sale price will actually be.

2 Advantages of Real Estate Options for Investors

Real estate investors can also use options to their advantage.

It’s a Lower-Risk Way to Develop Property

For example, let’s say an investor finds a property they’re interested in developing into housing. The investor needs to create a plan for the property and get other investors involved before they can buy it, so they purchase a real estate option to give them the exclusive right to buy the land.

The investor can make a profit by bringing in investors at a higher rate than the option. They can then buy the land and sell it to the developers they brought in to make a profit.

If they aren’t able to get developers and investors involved before the contract expires then they simply don’t buy the land.

An Investor Can Buy and Sell Real Estate Options

Investors can also make a profit just on buying and selling real estate options contracts rather than the properties themselves. This is a much less capital-intensive way to get involved in real estate investing.

For instance, an investor might find a property they expect will increase in value in the coming months. They purchase a real estate option to buy the land at the current market rate within the next year, pay a premium, and wait.

At any point during the period of the agreement the investor can either act on the contract and buy the property, or they can sell the contract to someone else. Let’s say the value of the property increases three months into the contract. The investor can find another investor who wants to purchase the contract for them for a higher price than the premium the original investor paid.

Whether any investor buys the property or not, the seller of the property keeps the premium.

The Takeaway

Real estate options are a way for investors to get involved in real estate investing without directly buying properties. As with any other kind of options, the investor buys the right to buy or sell at a certain price, but is not obligated to do so.

SoFi’s options trading platform offers qualified investors the flexibility to pursue income generation, manage risk, and use advanced trading strategies. Investors may buy put and call options or sell covered calls and cash-secured puts to speculate on the price movements of stocks, all through a simple, intuitive interface.

With SoFi Invest® online options trading, there are no contract fees and no commissions. Plus, SoFi offers educational support — including in-app coaching resources, real-time pricing, and other tools to help you make informed decisions, based on your tolerance for risk.

Photo credit: iStock/Melpomenem

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Options involve risks, including substantial risk of loss and the possibility an investor may lose the entire amount invested in a short period of time. Before an investor begins trading options they should familiarize themselves with the Characteristics and Risks of Standardized Options . Tax considerations with options transactions are unique, investors should consult with their tax advisor to understand the impact to their taxes.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOIN0723075