An employee savings plan (ESP) is a valuable financial tool designed to help workers set aside money for future goals, such as retirement or health care expenses. Offered as a workplace benefit, these plans provide structured and often tax-advantaged ways to save regularly through automatic payroll deductions. Some employers may also add to their employees’ savings with matching contributions. A popular ESP offered by U.S. employers is the 401(k) retirement plan.

Below, we take a closer look at how ESPs work, the types available, their benefits and potential drawbacks, and how to make the most of this valuable workplace perk.

Key Points

• An employee savings plan offers a way to save for future goals like retirement through payroll deductions.

• Contributions are often matched by employers, increasing savings potential.

• Retirement sayings plans typically offer a range of investment options, including stocks and bonds, but generally charge fees.

• Contributions and earnings may grow tax-deferred until withdrawal.

• Other types of employee savings plans include health savings accounts, pension plans, and profit-sharing plans.

What Is an Employee Savings Plan?

Some employers offer an employee savings plan to help employees invest for retirement and other long-term financial goals. Leveraging an employee savings plan is one of the first steps to building a simple savings plan you can stick to.

Typically, each employee chooses how much they want to contribute to the plan each pay period. That amount is then deducted from the employee’s paycheck. The automated process can help make it easier to save, and employees generally have the option to change their contribution amount based on their needs and goals.

Employee savings plan contributions are often made on a pre-tax basis. That means the funds are transferred to your savings plan before taxes are taken from your paycheck. This allows you to save money for future needs while paying taxes on a smaller portion of your salary.

In some cases, your employer may offer a matching contribution to any funds you contribute to your employee savings plan. Usually, there is a match limit equivalent to a certain percentage of your salary.

For instance, imagine your employer matches 100% of your contributions up to 3% of your salary and you earn $75,000 a year. That amounts to $2,250 of essentially “free money” each year. As long as you contribute at least $2,250 to your plan, your employer will give you the same amount, for a total of $4,500 — plus anything over that amount you decide to contribute.

Types of Employee Savings Plans

Employee savings plans most commonly help workers save for retirement and come in two main forms: defined-contribution plans offered by private employers (known as 401(k) plans), and defined-contribution plans offered by public or non-profit organizations (known as 403(b) or 457(b) plans).

Another type of employee savings plan you may see is a health savings account (HSA). Some companies will offer this kind of account to employees with high-deductible health plans (HDHPs ). An HSA lets you save money tax-free to pay for qualified medical costs that aren’t covered by insurance.

A profit-sharing plan is less common, but also helps you save for retirement. With this type of ESP, employees receive an amount from their employer based on company profits. Smaller companies may offer a stand-alone profit-sharing plan, where only employer contributions are permitted. Larger companies, on the other hand, may make contributions based on profits to an employee’s 401(k) plan; they may or may not offer employer-matching contributions as well.

A pension plan is another type of employer-sponsored retirement savings plan. With this plan, employers contribute to a pool of funds for a worker’s future benefit. In some cases, the employee can also contribute to the plan via paycheck deductions. When the employee retires, they receive their pension either as a lump-sum payment or a set monthly payment for life. These days, very few companies offer this type of benefit, instead opting to offer a 401(k) plan or other similar option.

What Are the Benefits of an Employee Savings Plan?

There are a number of advantages to using an employee savings plan. The first is that contributions are typically made on a pre-tax basis. This gives you a tax break upfront, reducing the amount of taxes you pay on your overall salary. So even though your take-home pay is smaller because of those automatic contributions, your taxable income is also less. Plus you have a growing investment account to help you prepare for retirement or other goals.

Another advantage of participating in an employee savings plan is that your employer could offer a free contribution match as part of their benefits package to retain team members. According to 2024 research by Vanguard, 96% of 401(k) plans have some kind of an employer contribution.

Employer-sponsored retirement saving plans also come with larger annual contribution limits than individual retirement accounts (IRAs). In 2025, the 401(k) contribution limit is $23,500 for employee salary deferrals ($70,000 for combined employee and employer contributions). Those aged 50 to 59 or 64 or older are eligible for an additional $7,500 in catch-up contributions; those aged 60 to 63 can contribute up to $11,250 in catch-up contributions, if their plan allows. A traditional IRA, on the other hand, only allows you to contribute $7,000 ($8,000 for those age 50 or older) for tax year 2025.

In 2026, the 401(k) contribution limit is $24,500 for employee salary deferrals ($72,000 for combined employee and employer contributions). Those aged 50 to 59 or 64 or older are eligible for an additional $8,000 in catch-up contributions; those aged 60 to 63 can contribute up to $11,250 in catch-up contributions, if their plan allows. By comparison, a traditional IRA only allows you to contribute $7,500 ($8,600 for those age 50 or older) for tax year 2026.

Under a new law regarding catch-up contributions that went into effect on January 1, 2026 (as part of SECURE 2.0), individuals aged 50 and older whose FICA wages exceeded $150,000 in 2025 are required to put their catch-up contributions into a Roth 401(k) account. Because of the way Roth accounts work, these individuals will pay taxes on their 401(k) catch-up contributions upfront, and make eligible withdrawals tax-free in retirement. This means their taxable income will not be lowered; they could even potentially move into higher tax bracket. Those impacted by the new law should check with their employer or plan administrator to find out how to proceed.

What to Look Out For

While there are a number of advantages that come with an employee savings plan, there are also some pitfalls to beware of. Consider these points:

• Some employers require you to work at the company for a certain number of years (often five) before you are fully vested, meaning you own 100% of your employer’s contributions to your 401(k). If you leave the company (either voluntarily or involuntarily) before that time has elapsed, you may forfeit some or all of the company match. Any contributions you make, however, are 100% owned by you and cannot be forfeited. It’s important to find out these details from the human resources department at your company, especially if you’re thinking about a job change.

• Another downside to an employer savings plan for retirement is that although your contributions may be tax-free, you typically have to pay federal and state income taxes when you make withdrawals.

• Another factor to consider is your tax bracket. Some people may expect to be in a higher tax bracket during their prime working years, so the immediate tax deduction may be helpful. Others may end up being in a higher tax bracket after they’ve accumulated wealth over decades and reach retirement age.

• In addition to paying income taxes on your withdrawals, employee savings plans for retirement also typically come with a 10% early withdrawal penalty if you take out cash before reaching 59 ½ years old. There are some exceptions to this penalty, but be aware of it should you be considering making an early withdrawal.

• Also remember that your plan contributions are investments that are subject to risk. It’s not like a savings account through a financial institution that offers a yield based on your deposits. You will typically be responsible for crafting your portfolio and managing your investments. The options available to you may vary based on the specific plan offered by your employer.

• No matter how much you contribute, the value of your plan is impacted by the performance of your investment choices, regardless of how much money you contributed over the years. It is also helpful to review your goals regularly and gauge your risk based on your time horizons.

For instance, investors may opt to invest in riskier investment vehicles when they’re younger because the potential for gains may outweigh the risk. As they get older and approach retirement, they may begin to allocate less money to those higher-risk investments.

• Finally, be aware of any administrative fees that come with your plan. Fees for 401(k) plans typically range from 0.5% to 2%, but can vary widely depending on the size of the plan, number of participants, and the plan’s provider. You can find the fees in the prospectus you receive when you enroll in the plan

Many employee savings plans designed to save for retirement allow you to borrow funds from your account if you choose to. Typically, you can borrow up to 50% of your 401(k) account balance for up to five years, up to a maximum of $50,000.

You’ll pay interest just as you would with any other loan, but that money gets paid back into your account. This may be one option to consider if you find yourself in need of cash, but there are several drawbacks to be aware of.

The loan terms only apply while you remain at the job providing the employee savings plan. If you leave your job with a loan balance, you must repay the full amount by the due date of your next federal tax return.

Another consideration is that if you don’t pay the loan back by its due date, it counts as a distribution and you will likely have to pay income taxes and a penalty on the money.

You’ll also miss out on the growth those borrowed funds may have experienced, which could set back your retirement goals. To avoid this scenario, it’s a good idea to build an emergency fund and keep it in an account that pays a competitive rate but allows you to easily access your funds when you need them, such as a high-yield savings account.

The Takeaway

An employee savings plan can be an advantageous way to save towards retirement and other goals. It can be especially beneficial if your employer offers matching contributions, which can help boost your savings.

By starting early and automating the process, you can build an investment account with robust contributions throughout your career.

An employee savings plan can be one part of a well-rounded financial portfolio, but there are other types of savings accounts that can be useful as well. For shorter-term goals, like building an emergency fund or saving for a large purchase or upcoming vacation, it may be worth opening a high-yield savings account.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with eligible direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with SoFi, NerdWallet’s 2024 winner for Best Checking Account Overall.* Enjoy 3.30% APY on SoFi Checking and Savings with eligible direct deposit.

🛈 While SoFi does not offer Employee Savings Plans (ESPs), we do offer alternative savings vehicles such as high-yield savings accounts.

SoFi Checking and Savings is offered through SoFi Bank, N.A. Member FDIC. The SoFi® Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

Annual percentage yield (APY) is variable and subject to change at any time. Rates are current as of 12/23/25. There is no minimum balance requirement. Fees may reduce earnings. Additional rates and information can be found at https://www.sofi.com/legal/banking-rate-sheet

Eligible Direct Deposit means a recurring deposit of regular income to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government benefit payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Eligible Direct Deposit”) via the Automated Clearing House (“ACH”) Network every 31 calendar days.

Although we do our best to recognize all Eligible Direct Deposits, a small number of employers, payroll providers, benefits providers, or government agencies do not designate payments as direct deposit. To ensure you're earning the APY for account holders with Eligible Direct Deposit, we encourage you to check your APY Details page the day after your Eligible Direct Deposit posts to your SoFi account. If your APY is not showing as the APY for account holders with Eligible Direct Deposit, contact us at 855-456-7634 with the details of your Eligible Direct Deposit. As long as SoFi Bank can validate those details, you will start earning the APY for account holders with Eligible Direct Deposit from the date you contact SoFi for the next 31 calendar days. You will also be eligible for the APY for account holders with Eligible Direct Deposit on future Eligible Direct Deposits, as long as SoFi Bank can validate them.

Deposits that are not from an employer, payroll, or benefits provider or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, Wise, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, or are non-recurring in nature (e.g., IRS tax refunds), do not constitute Eligible Direct Deposit activity. There is no minimum Eligible Direct Deposit amount required to qualify for the stated interest rate. SoFi Bank shall, in its sole discretion, assess each account holder's Eligible Direct Deposit activity to determine the applicability of rates and may request additional documentation for verification of eligibility.

See additional details at https://www.sofi.com/legal/banking-rate-sheet.

*Awards or rankings from NerdWallet are not indicative of future success or results. This award and its ratings are independently determined and awarded by their respective publications.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

We do not charge any account, service or maintenance fees for SoFi Checking and Savings. We do charge a transaction fee to process each outgoing wire transfer. SoFi does not charge a fee for incoming wire transfers, however the sending bank may charge a fee. Our fee policy is subject to change at any time. See the SoFi Bank Fee Sheet for details at sofi.com/legal/banking-fees/.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement. Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

How much does the average American have in savings? Age tends to have a lot to do with it. Generally, as people get older, they are likely to have more savings.

But what the average person has in a savings account also depends on their financial goals and personal circumstances.

If you’re looking for a benchmark of just how much you should save by a specific age, or how much you should start contributing right now, read on for average savings by age and some tips that could help.

Key Points

• The average savings for individuals under 35 is $20,540.

• Individuals between the ages of 35 and 44 have an average savings of $41,540.

• Those aged 45 to 54 have an average savings of $71,130.

• The average savings for individuals between 55 and 64 is $72,520.

• Individuals aged 65 and older have an average savings of $100,2500.

The Importance of Saving for the Future

Life can happen fast. For example, the average cost of having a new baby is almost $19,000, including approximately $3,000 in out-of-pocket expenses for pregnancy and delivery. And then there’s the cost of caring for a child, which some estimates put at more than $310,605 for raising them through age 17.

And, if that baby wants to get a college degree, you’re looking at a whole new realm of savings. The cost of a four-year public college education can range from about $108,584 to $182,832, according to the Education Data Initiative.

There’s one other big reason to save for the future: People are living longer. According to a 2025 survey by the Employee Benefit Research Institute, only 28% of American workers are “very confident they will be able to retire comfortably.” Thirty-two percent of workers say their lack of confidence is because they have less than $25,000 in savings and investments.

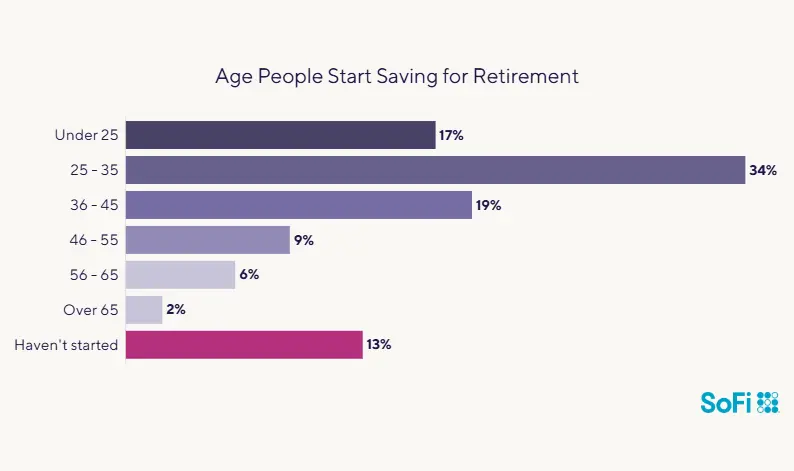

Fortunately, the concept of saving for the future seems to be resonating with people at younger ages. According to the SoFi 2024 Retirement Survey, more than half (51%) of respondents started saving for retirement before age 35, with many of that group starting by age 25.

Source: SoFi 2024 Retirement Survey

A Savings Shortfall

Still, Americans’ savings strategy has a way to go. More than half of Americans can’t cover an unexpected $1,000 expense, according to Bankrate’s 2025 emergency savings report. Only 41% say they could cover it.

And 37% of all Americans don’t have enough cash in savings to cover even a $400 emergency, the Federal Reserve found in its “Economic Well-Being of U.S. Households in 2024” report.

Average Savings by Age in the USA

The Federal Reserve’s latest (2022) Survey of Consumer Finances shows that the typical American household has an average savings balance of $62,410.

But average savings varies greatly by age and number of people in a household. Here’s what savings by age looks like.

Average Savings for Those 35 and Younger

Americans under the age of 35 had an average savings account balance of $20,540, according to the Fed’s survey.

This is a large age bracket that can range from those just graduating high school to recent college grads to young professionals well into a decade’s worth of work.

It’s wise to have three to six months of expenses in an emergency fund. At the very least, aiming to have $1,000 handy in a savings account for unexpected expenses is recommended.

For those who have started their careers, employer-sponsored retirement funds such as a 401(k) plan can be good options to start saving for long-term retirement goals.

It makes sense to contribute at least enough to get matching funds from an employer, if that’s an option with your company’s plan. For reference, the average 401(k) savings for those ages 25 to 34 is $42,640, according to Vanguard’s “How America Saves 2025” report.

Americans ages 35 to 44 had an average savings account balance of $41,540, according to the Federal Reserve survey. Those in this age bracket are now well into adulthood. At this stage of life, it’s prudent to have that three-to six-months’ worth of savings in an emergency fund, to cover the cost of everything from an accident to a lost job.

And, of course, keep contributing to your 401(k). For reference, the average 401(k) savings for those ages 35 to 44 is $103,552, according to the Vanguard report.

Average Savings by Age: 45 to 54

People ages 45 to 54 had an average savings account balance of $71,130, according to the Fed’s survey.

At this point, general financial advice dictates that a 50-year-old should have at least six times their annual salary if their intention is to retire at 67.

Those in this age group have an average 401(k) savings of $188,643.

Average Savings by Age: 55 to 64

The Fed survey found that Americans ages 55 to 64 had an average savings account balance of $72,520.

Since this is the time when most Americans are staring down retirement in a few years, it’s generally a good idea to boost retirement savings into high gear.

That’s because while younger people in 2025 are capped at contributing $23,500 a year to a 401(k) account, those age 50 and up are allowed to contribute an additional $7,500.This is known as a catch-up contribution. Also for 2026, those under age 50 can contribute up to $24,500, and those 50 and up can contribute an additional $8,000. And those aged 60 to 63 may again contribute an additional $11,250 instead of $8,000.

Under a new law that went into effect on January 1, 2026 (as part of SECURE 2.0), individuals aged 50 and older who earned more than $150,000 in FICA wages in 2025 are required to put their 401(k) catch-up contributions into a Roth 401(k) account. With Roth accounts, individuals pay taxes on contributions upfront, but can make qualified withdrawals tax-free in retirement.

The average retirement savings account for a person aged 55 to 64 is $271,230. It’s important to note that taking a withdrawal from such a plan before the age of 59 ½ could mean paying taxes and penalties.

Average Savings by Age: 65 and Older

This is when savings really peaks for the average American. The latest Federal Reserve Survey of Consumer Finances found that Americans ages 65 to 74 had an average savings account balance of $100,250.

However, that savings number does drop over time. According to the survey, Americans ages 75 and up had an average savings account balance of $82,800.

This underscores the importance of creating a retirement budget and sticking to it in order to have enough savings for as long as needed.

But before retirement, try to hit the average retirement savings amount for those ages 65 and up, which is $299,442.

This chart offers an at-a-glance comparison of the average American savings by age.

Age

Average savings

Under 35

$20,540

35-44

$41,540

45-54

$71,130

55-64

$72,520

65+

$100,250

Median Savings by Age

Median savings is different from average savings. The median is the number in the middle of all the other numbers, meaning half the numbers are higher and half are lower. So with median savings, half the people in an age category will have saved more and half will have saved less.

These are the median savings by age, according to the latest Federal Reserve Survey of Consumer Finances:

• Under 35: $5,400

• 35-44: $7,500

• 45-54: $8,700

• 55-64: $8,000

• 65-74: $13,400

Savings vs Retirement Savings

What Americans have saved for emergencies, expenses, and other near-future goals is different from what they have in their retirement savings accounts, as you can see from all the information above. It’s critical to have both types of savings at the same time.

And keep this in mind: As you get older, and closer to retirement, it’s important that your retirement savings grow even more. It’s a good idea to contribute the maximum amount allowed to your retirement accounts at this time, if you can. This is one of the ways to save for retirement.

Saving a Little Bit More

Reaching specific savings goals doesn’t have to be complicated. It just means doing a bit of homework, strategizing, and staying diligent about personal finances.

The first step in saving more is to analyze current expenses to see what can be cut back on or cut out altogether to make more room for saving. This means creating a personal budget and tracking current spending.

To track spending, a person could create an excel spreadsheet and list all expenditures by categories like groceries, phone bill, car expenses, housing, medical, entertainment and others over the course of a month, filling it in with every single dollar spent to see where the money is going. Or you can use an online tracker like SoFi’s tracker, which allows users to connect all their accounts to one dashboard and track spending habits in real time.

After the month is up, the next step is to look back on the expenditures list. Was there anything that surprised you? Do you need all those streaming subscriptions? How about that gym membership — did it actually get used? This is the time to get a little ruthless.

After figuring out what’s left, try implementing a general budget outline like the 50/30/20 rule. This means that approximately 50% of your after-tax income goes toward essential expenses like food and rent, while 30% goes toward discretionary expenses like nights out at the movies or concerts. The last 20% belongs to savings and retirement account goals.

Next, it’s time to get creative about saving even more for the future. This can be done by putting more cash into a high-yield savings account via direct deposit right from a paycheck.

Those looking to save a few more bucks every month could also do so by getting rid of unnecessary expenses. But, instead of pocketing that cash, consider using mobile banking to direct that cash right to savings.

Still feeling the pinch and don’t really have room to save more from a budget? Working part-time for, say, a ride-sharing company could allow you to set your own hours and earn extra income based on how much time you can dedicate to it. Other options might include freelance work in photography, writing, or other creative arts.

The Takeaway

Saving for goals in the near term — such as a house or a car — along with putting away money for an emergency savings fund to cover unexpected expenses, is important at every age. And so is investing in your future, including for retirement. The earlier you start saving for all your goals, the better.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with eligible direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with SoFi, NerdWallet’s 2024 winner for Best Checking Account Overall.* Enjoy 3.30% APY on SoFi Checking and Savings with eligible direct deposit.

FAQ

How much should a 30 year old have in savings?

By age 30, you should have the equivalent of your annual salary saved. So if you make $60,000 a year, you should have $60,000 in savings.

How much money does an average person have in savings?

The average American has a savings balance of $62,410, according to the 2022 Federal Reserve Survey of Consumer Finances, which is the latest data available.

How many Americans have $100,000 in savings?

According to one 2023 survey, only 14% of Americans have at least $100,000 in savings.

SoFi Checking and Savings is offered through SoFi Bank, N.A. Member FDIC. The SoFi® Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

Annual percentage yield (APY) is variable and subject to change at any time. Rates are current as of 12/23/25. There is no minimum balance requirement. Fees may reduce earnings. Additional rates and information can be found at https://www.sofi.com/legal/banking-rate-sheet

Eligible Direct Deposit means a recurring deposit of regular income to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government benefit payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Eligible Direct Deposit”) via the Automated Clearing House (“ACH”) Network every 31 calendar days.

Although we do our best to recognize all Eligible Direct Deposits, a small number of employers, payroll providers, benefits providers, or government agencies do not designate payments as direct deposit. To ensure you're earning the APY for account holders with Eligible Direct Deposit, we encourage you to check your APY Details page the day after your Eligible Direct Deposit posts to your SoFi account. If your APY is not showing as the APY for account holders with Eligible Direct Deposit, contact us at 855-456-7634 with the details of your Eligible Direct Deposit. As long as SoFi Bank can validate those details, you will start earning the APY for account holders with Eligible Direct Deposit from the date you contact SoFi for the next 31 calendar days. You will also be eligible for the APY for account holders with Eligible Direct Deposit on future Eligible Direct Deposits, as long as SoFi Bank can validate them.

Deposits that are not from an employer, payroll, or benefits provider or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, Wise, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, or are non-recurring in nature (e.g., IRS tax refunds), do not constitute Eligible Direct Deposit activity. There is no minimum Eligible Direct Deposit amount required to qualify for the stated interest rate. SoFi Bank shall, in its sole discretion, assess each account holder's Eligible Direct Deposit activity to determine the applicability of rates and may request additional documentation for verification of eligibility.

See additional details at https://www.sofi.com/legal/banking-rate-sheet.

We do not charge any account, service or maintenance fees for SoFi Checking and Savings. We do charge a transaction fee to process each outgoing wire transfer. SoFi does not charge a fee for incoming wire transfers, however the sending bank may charge a fee. Our fee policy is subject to change at any time. See the SoFi Bank Fee Sheet for details at sofi.com/legal/banking-fees/.

*Awards or rankings from NerdWallet are not indicative of future success or results. This award and its ratings are independently determined and awarded by their respective publications.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Disclaimer: The projections or other information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

It’s an honor to be asked to be a member of a friend’s or family member’s wedding, but it also comes with a cost. Between buying/renting attire, attending prewedding events, and purchasing gifts, it can run around $1,650 to be a bridesmaid and $1,600 to be a groomsman.

Just one wedding can take a bite out of your budget, not to mention the familiar scenario of attending several weddings in one year. We’ll help you understand the expenses that go into being a part of the big day so you can prepare and budget well in advance.

• Being in a wedding costs around $1,650 for bridesmaids and $1,600 for groomsmen, with expenses varying widely by location and event style.

• Bridesmaids typically pay for their dress ($128 on average), alterations, accessories, hair, and makeup, and they may also contribute to the bachelorette party.

• Groomsmen usually cover attire or tux rentals ($100-$250) and bachelor party expenses (averaging $1,300).

• Travel and accommodations add significantly to costs, especially for destination events.

• Both bridesmaids and groomsmen are expected to give gifts, with bridesmaids spending around $170 and groomsmen about $160 on average.

How Much Does It Cost to Be a Bridesmaid?

While the average bridesmaid may spend $1,650 to be a part of the bridal party, costs vary significantly depending on the location of the wedding, number of events, and dress code. Before you agree to participate as a bridesmaid (or maid of honor), it’s important to consider what costs you may be responsible for.

Etiquette dictates that bridesmaids cover the cost of their dress, shoes, and any accessories the bride has selected for them to wear. According to The Knot’s 2025 Real Weddings Study (which surveyed nearly 17,000 couples who wed in 2024), the average bridesmaid dress costs $128 per person.

You’ll likely also be responsible for any alterations, which can run from $75 to $150, depending on what adjustments are needed. While there are ways you can save — such as renting a dress — that decision is often not up to the bridesmaid.

Traditionally, if the bride requests that everyone in the party have their hair and makeup done in a certain style, she will cover the cost. If, on the other hand, bridesmaids are given the option to opt in or do their own thing, the bridesmaids generally cover the cost of getting glammed up for the big day. The average cost of wedding hair for bridesmaids is $100, and you can tack on another $100 for makeup.

Bachelorette Party

Bachelorette parties have become more elaborate in recent years. Typically, every attendant pays for their own expenses, while also splitting the cost to cover most, or all, of the bride’s expenses.

According to The Knot, the average cost of a bachelorette party in 2023 was $1,300 per person. Of course, the cost of attending a bachelorette party varies significantly depending on the type, location, and length of the event. Celebrations that last one to two days cost, on average, $1,135 per attendee, while those that go on for three to four days can total $1,630 each. Also, the farther you need to travel to the event, the more you’ll need to spend. Guests who travel to the bachelorette party locale by plane spend an average of $2,000, while those who travel by personal car spend an average of $900 to attend the event.

Wedding Travel and Accommodations

For the wedding itself, the bridal party is typically expected to cover the costs of travel and accommodations, which can vary significantly depending on the location of the event and length of stay (with members of the bridal party possibly needing to arrive early or stay late).

On average, wedding guests who need to travel outside of their town or city to attend a wedding spend between $840 and $1680 on travel and up to $630 on accommodations. You could end up spending significantly more if you’re covering travel costs for yourself and other family members, or if the wedding involves long-distance travel. When the wedding is local, travel costs are likely to be minimal.

Bridesmaids traditionally give shower and wedding gifts, which add to the cost of being in someone’s wedding. According to The Knot, the average bridesmaid bridal shower gift costs between $50 and $75, while the average bridesmaid wedding gift costs around $170. A group gift may allow you to spend less while giving something nicer than you could afford on your own.

What Does the Maid of Honor Pay For?

Being the maid of honor generally doesn’t cost more than being a bridesmaid, but it does come with additional duties and a greater commitment of time. Generally, the maid of honor is there to assist with any tasks she can take off the bride’s to-do list. They may be involved in planning prewedding events and communicating with other members of the wedding party.

In some cases, the maid of honor might plan the shower and help cover the costs. However, these days, the cost of a wedding shower is more commonly covered by family.

Groomsmen typically pay for their wedding attire, the cost to attend a bachelor party (which may include sharing the cost for the groom’s attendance), the cost to attend the wedding (which might involve travel and accommodations), as well as a wedding gift. Here’s a look at what it all adds up to.

Formalwear or Tuxedo Rental

Just like bridesmaids generally pay for their dresses, groomsmen typically pay for their wedding day clothing. This might be a suit, tuxedo, shirt and slacks, or another type of attire selected by the groom or couple. Typically, the groomsmen’s attire is purchased or rented, but in some cases, a groom will let their wedding party choose from their own wardrobe, which can be a more affordable option.

If you need to rent a tux for the event, costs vary depending on what style, design, brand, and accessories you’ll need to wear. On average, you can expect to pay between $150 and $300 to rent a tux for the standard period.

Bachelor Party

Groomsmen normally take part in planning the bachelor party and may cover their own costs and the groom’s. According to a recent survey by The Knot (which included roughly 500 respondents who attended, or planned to attend, a bachelor party in 2023), the average cost of a bachelor party is $1,400 per person. The survey also found that the average bachelor celebration lasts for two days, and roughly one-fifth of attendees are flying to the party destination. Indeed, 29% of those surveyed are spending $2,000 or more to celebrate in a major metro city.

For guests who drove or were planning to drive to the event’s location, spending was less, averaging $1,000 per attendee.

Wedding Gift

Groomsmen are generally expected to give the couple a wedding gift, though they are not expected to spend more on a gift than other guests do. According to The Knot’s 2024 Real Wedding Guest Study, wedding party members spend an average of $160 on their gifts. If you want to save money, consider chipping in for a group gift with other wedding party members.

The Takeaway

It’s not unusual for a bridesmaid to spend $1,650, including the dress, bachelorette party, and gifts. Groomsmen may spend just a little bit less ($1,600) for a rental tux, bachelor party, and wedding gift. Keep in mind, however, that the cost to be in someone’s wedding can run much higher or lower, depending on the location and style of the wedding.

If you haven’t saved up enough money to be in a friend’s or family member’s wedding in advance, there are better options than throwing it all on a credit card. Personal loans are designed to help cover life’s big events. SoFi Personal Loans offer low fixed rates, no-fee options, and a quick and easy online application process. Checking your rate takes just a minute.

SoFi’s Personal Loan was named a NerdWallet 2026 winner for Best Personal Loan for Large Loan Amounts.

FAQ

What do bridesmaids and groomsmen usually pay for?

Bridesmaids and groomsmen are typically expected to pay for their wedding-day attire and accessories, travel and accommodations, and a wedding gift. They might also cover the costs of bachelorette or bachelor parties, which often make up a large portion of the expense.

How can I participate in a wedding while staying on budget?

You can keep costs down by splitting the cost of a group gift, limiting optional expenses such as professional hair and makeup, and choosing more affordable travel and accommodation options if needed. Planning ahead and discussing your expectations can help you manage your budget.

Does being the maid of honor cost more than being a bridesmaid?

Not necessarily. The maid of honor usually has more responsibilities and dedicates more time to helping with the wedding, but the role doesn’t generally cost more than being a bridesmaid, since most of the major expenses are the same and wedding shower costs are commonly covered by family.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Maxing out your 401(k) involves contributing the maximum allowable amount to your workplace retirement account to increase the benefit of compounding and appreciating assets over time.

All retirement plans come with contribution caps, and when you hit that limit it means you’ve maxed out that particular account.

There are a lot of things to consider when figuring out how to max out your 401(k) account, including whether maxing out your account is a good idea in the first place. Read on to learn about the pros and cons of maxing out your 401(k).

Key Points

• Maxing out your 401(k) contributions can help you save more for retirement and take advantage of tax benefits.

• If you want to max out your 401(k), strategies include contributing enough to get the full employer match, increasing contributions over time, utilizing catch-up contributions if eligible, automating contributions, and adjusting your budget to help free up funds for additional 401(k) contributions.

• Diversifying your investments within your 401(k) and regularly reviewing and rebalancing your portfolio can optimize your returns.

• Seeking professional advice and staying informed about changes in contribution limits and regulations can help you make the most of your 401(k).

What Exactly Does It Mean to ‘Max Out Your 401(k)?’

Maxing out your 401(k) means that you contribute the maximum amount allowed in a given year, as specified by the established 401(k) contribution limits. But it can also mean that you’re maxing out your contributions up to an employer’s percentage match.

If you want to max out your 401(k) in 2025, you’ll need to contribute $23,500. If you’re 50 or older, you can contribute an additional $7,500, for an annual total of $31,000. In addition, in 2025, those aged 60 to 63 may contribute up to an additional $11,250 instead of $7,500, thanks to SECURE 2.0, for an annual total of $34,750.

To max out your 401(k) in 2026, you would need to contribute $24,500. If you’re 50 or older, you can contribute an additional catch-up contribution of $8,000, for a total for the year of $32,500. Also in 2026, those aged 60 to 63 may contribute up to an additional $11,250 SECURE 2.0 catch-up instead of $8,000, for an annual total of $35,750.

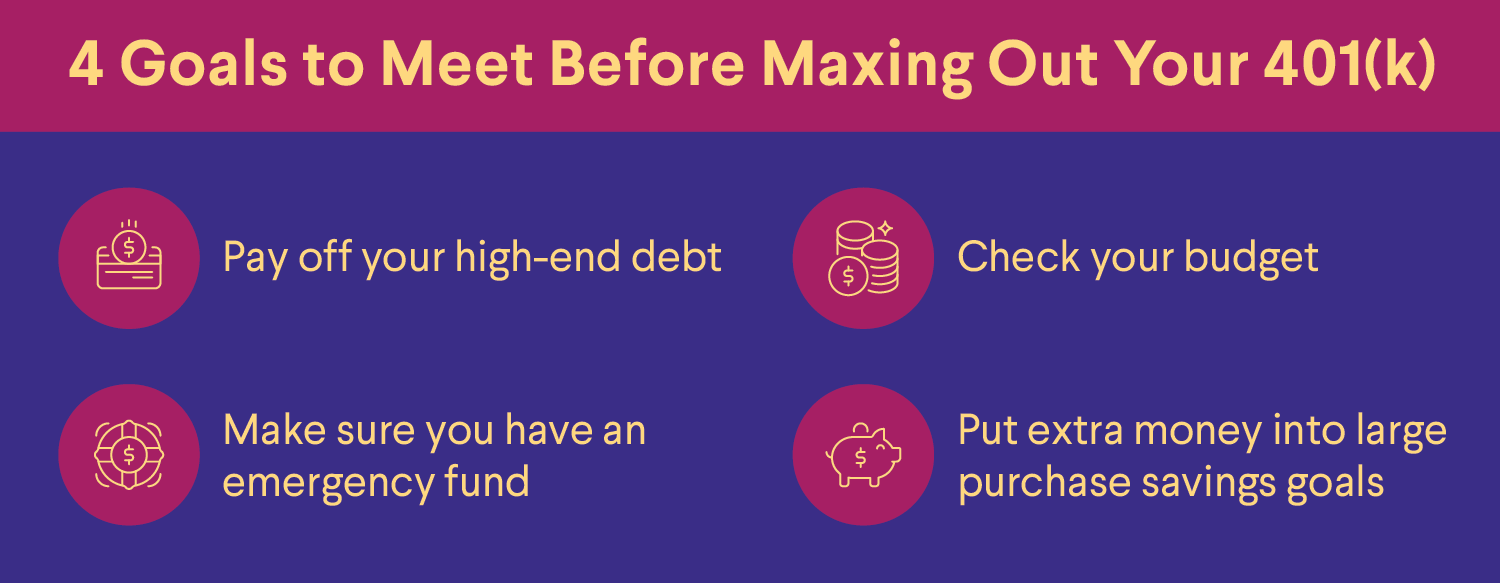

Should You Max Out Your 401(k)?

Generally speaking, yes, it’s a good thing to max out your 401(k) so long as you’re not sacrificing your overall financial stability to do it. Saving for retirement is important, which is why many financial experts would likely suggest maxing out any employer match contributions first.

But while you may want to take full advantage of any tax and employer benefits that come with your 401(k), you also want to consider any other financial goals and obligations you have before maxing out your 401(k).

That doesn’t mean you should put other goals first, and not contribute to your retirement plan at all. That’s not wise. Maintaining a baseline contribution rate for your future is crucial, even as you continue to save for shorter-term aims or put money toward debt repayment.

Other goals might include:

• Is all high-interest debt paid off? High-interest debt like credit card debt should be paid off first, so it doesn’t accrue additional interest and fees.

• Do you have an emergency fund? Life can throw curveballs — it’s smart to be prepared for job loss or other emergency expenses.

• Is there enough money in your budget for other expenses? You should have plenty of funds to ensure you can pay for additional bills, like student loans, health insurance, and rent.

• Are there other big-ticket expenses to save for? If you’re saving for a large purchase, such as a home or going back to school, you may want to put extra money toward this saving goal rather than completely maxing out your 401(k), at least for the time being.

Once you can comfortably say that you’re meeting your spending and savings goals, it might be time to explore maxing out your 401(k). There are many reasons to do so — it’s a way to take advantage of tax-deferred savings, employer matching (often referred to as “free money”), and it’s a relatively easy and automatic way to invest and save, since the money gets deducted from your paycheck once you’ve set up your contribution amount.

How to Max Out Your 401(k)

Only a relatively small percentage of people max out their 401(k)s, but that doesn’t mean you can’t be one of them. Here are some strategies for how to max out your 401(k).

1. Max Out 401(k) Employer Contributions

Your employer may offer matching contributions, and if so, there are typically rules you will need to follow to take advantage of their match.

An employer may require a minimum contribution from you before they’ll match it, or they might match only up to a certain amount. They might even stipulate a combination of those two requirements. Each company will have its own rules for matching contributions, so review your company’s policy for specifics.

For example, suppose your employer will match your contribution up to 3%. So, if you contribute 3% to your 401(k), your employer will contribute 3% as well. Therefore, instead of only saving 3% of your salary, you’re now saving 6%. With the employer match, your contribution just doubled. Note that employer contributions can range from nothing at all up to a certain limit. It depends on the employer and the plan.

Since saving for retirement is one of the best investments you can make, it’s wise to take advantage of your employer’s match. Every penny helps when saving for retirement, and you don’t want to miss out on this “free money” from your employer.

If you’re not already maxing out the matching contribution and wish to, you can speak with your employer (or HR department, or plan administrator) to increase your contribution amount, you may be able to do it yourself online.

2. Max Out Salary-Deferred Contributions

While it’s smart to make sure you’re not leaving free money on the table, maxing out your employer match on a 401(k) is only part of the equation.

In order to make sure you’re setting aside an adequate amount for retirement, consider contributing as much as your budget will allow. As noted earlier, individuals younger than age 50 can contribute up to $23,500 in 2025, and up to $24,500 in 2026.

Those contributions aren’t just an investment in your future lifestyle in retirement. Because they are made with pre-tax dollars, they lower your taxable income for the year in which you contribute. For some, the immediate tax benefit is as appealing as the future savings benefit.

3. Take Advantage of Catch-Up Contributions

As mentioned, 401(k) catch-up contributions allow investors aged 50 and over to increase their retirement savings — which is especially helpful if they’re behind in reaching their retirement goals.

Individuals 50 and over can contribute an additional $7,500 for a total of $31,000 in 2025. And in 2026, those 50 and older can contribute an extra $8,000 for a total of $32,500. And in both 2025 and 2026, those aged 60 to 63 can contribute up to an additional $11,250, instead of $7,500 in 2025 and $8,000 in 2026, for a total of $34,750 and $35,750 respectively. Putting all of that money toward retirement savings can help you truly max out your 401(k).

As you draw closer to retirement, catch-up contributions can make a difference, especially as you start to calculate when you can retire. Whether you have been saving your entire career or just started, this benefit is available to everyone who qualifies.

And of course, in many cases, this extra contribution will lower taxable income even more than regular contributions. Although using catch-up contributions may not push everyone to a lower tax bracket, it will certainly minimize the tax burden during the next filing season for many filers — with an important exception.

Under a new law regarding catch-up contributions that went into effect on January 1, 2026 (as part of SECURE 2.0), individuals aged 50 and older whose FICA wages exceeded $150,000 in 2025 are required to put their 401(k) catch-up contributions into a Roth 401(k) account. Because of the way Roth accounts work, these individuals will pay taxes on their catch-up contributions upfront, and make eligible withdrawals tax-free in retirement. This means their taxable income will not be lowered; they could even potentially move into higher tax bracket. Those impacted by the new law should check with their employer or plan administrator to find out how to proceed.

4. Reset Your Automatic 401(k) Contributions

When was the last time you reviewed your 401(k)? It may be time to check in and make sure your retirement savings goals are still on track. Is the amount you originally set to contribute each paycheck still the correct amount to help you reach those goals?

With the increase in contribution limits most years, it may be worth reviewing your budget to see if you can up your contribution amount to max out your 401(k). If you don’t have automatic payroll contributions set up, you could set them up.

It’s generally easier to save money when it’s automatically deducted; a person is less likely to spend the cash (or miss it) when it never hits their checking account in the first place.

If you’re able to max out the full 401(k) limit, but fear the sting of a large decrease in take-home pay, consider a gradual, annual increase such as 1% — how often you increase it will depend on your plan rules as well as your budget.

5. Put Bonus Money Toward Retirement

Unless your employer allows you to make a change, your 401(k) contribution may be deducted from any bonus you might receive at work. Some employers allow you to determine a certain percentage of your bonus to contribute to your 401(k).

Consider possibly redirecting a large portion of a bonus to 401k contributions, or into another retirement account, such as an individual retirement account (IRA). Because this money might not have been expected, you won’t miss it if you contribute most of it toward your retirement.

You could also do the same thing with a raise. If your employer gives you a raise, consider putting it directly toward your 401(k). Putting this money directly toward your retirement can help you inch closer to maxing out your 401(k) contributions.

6. Maximize Your 401(k) Returns and Fees

Many people may not know what they’re paying in investment fees or management fees for their 401(k) plans. By some estimates, the average fees for 401(k) plans are between 0.5% and 2%, but some plans may have higher fees.

Fees add up — even if your employer is paying the fees now, you’ll have to pay them if you leave the job and keep the 401(k).

Essentially, if an investor has $100,000 in a 401(k) and pays $1,000 or 1% (or more) in fees per year, the fees could add up to thousands of dollars over time. Any fees you have to pay can chip away at your retirement savings and reduce your returns.

It’s important to ensure you’re getting the most for your money in order to maximize your retirement savings. If you are currently working for the company, you could discuss high fees with your HR team.

One way to potentially lower your costs is to find more affordable investment options. Generally speaking, index funds often charge lower fees than other investments. If an employer’s plan offers an assortment of low-cost index funds, may consider investing in these funds to save some money and help build a diversified portfolio.

What Happens If You Contribute Too Much to Your 401(k)?

After an individual maxes out their 401(k) for the year — meaning they’ve hit the contribution limit corresponding to their age range — if they don’t stop making contributions they will risk paying additional taxes on their overcontributions.

In the event that an individual makes an overcontribution, they might let their plan manager or administrator know, and withdraw the excess amount. If they leave the excess in the account, it’ll be taxed twice — once when it was contributed initially, and again when they take it out.

What to Do After Maxing Out a 401(k)?

If you max out your 401(k) this year, pat yourself on the back. Maxing out your 401(k) is a financial accomplishment. But now you might be wondering, what’s next? Here are some additional retirement savings options to consider if you have already maxed out your 401(k).

Open an IRA

An individual retirement account (IRA) can be an option to complement an employer’s retirement plans. With a traditional IRA, you can contribute pre-tax dollars up to the annual limit, which is $7,000 in 2025. If you’re 50 or older, you can contribute an extra $1,000, for an annual total of $8,000 in 2025. In 2026, you can contribute up to $7,500, while those 50 and older can contribute an additional $1,100, for a total of $8,600 for 2026.

You may also choose to consider a Roth IRA. As with a traditional IRA, the annual contribution limit for a Roth IRA in 2025 is $7,000, and $8,000 for those 50 or older. And in 2026, the annual Roth IRA contribution limit is $7,500, and $8,600 for those age 50 and up.

Roth IRA accounts have income limits, but if you’re eligible, you can contribute with after-tax dollars, which means you won’t have to pay taxes on earnings withdrawals in retirement as you do with traditional IRAs.

It’s possible to open an IRA at a brokerage, mutual fund company, or other financial institution. If you ever leave your job, you can typically roll your employer’s 401(k) into your IRA without facing tax consequences as long as both accounts are similarly taxed, such as rolling funds from a traditional 401(k) to a traditional IRA, and funds are transferred directly from one plan to the other. Doing a 401(k) to IRA rollover may allow you to invest in a broader range of investments with lower fees.

Boost an Emergency Fund

Experts often advise establishing an emergency fund with at least three to six months of living expenses before contributing to a retirement savings plan. Perhaps you’ve already done that — but haven’t updated that account in a while. As your living expenses increase, it’s a good idea to make sure your emergency fund grows, too. This will cover you financially in case of life’s little curveballs: new brake pads, a new roof, or unforeseen medical expenses.

Save for Health Care Costs

Contributing to a health savings account (HSA) can reduce out-of-pocket costs for expected and unexpected health care expenses, though you can only open and contribute to an HSA if you are enrolled in a high-deductible health plan (HDHP).

For tax year 2025, those eligible can contribute up to $4,300 pre-tax dollars for an individual plan or up to $8,550 for a family plan. Those 55 or older who are not enrolled in Medicare can make an additional catch-up contribution of $1,000 per year.

For tax year 2026, those who are eligible can contribute up to $4,400 for an individual plan or up to $8,750 for a family plan. Those 55 or older who are not enrolled in Medicare can again make an additional catch-up of $1,000.

The money in this account can be used for qualified out-of-pocket medical expenses such as copays for doctor visits and prescriptions. Another option is to leave the money in the account and let it grow for retirement. Once you reach age 65, you can take out money from your HSA without a penalty for any purpose. However, to be exempt from taxes, the money must be used for a qualified medical expense. Any other reasons for withdrawing the funds will be subject to regular income taxes.

Increase College Savings

If you’re feeling good about maxing out your 401(k), consider increasing contributions to your child’s 529 college savings plan (a tax-advantaged account meant specifically for education costs, sponsored by states and educational institutions).

College costs continue to creep up every year. Helping your children pay for college helps minimize the burden of college expenses, so they hopefully don’t have to take on many student loans.

Open a Brokerage Account

After maxing out a 401(k), individuals might also consider opening a brokerage account. Brokerage firms offer various types of investment accounts, each with different services and fees. A full-service brokerage firm may provide different financial services, which include allowing investors to trade securities.

Many brokerage firms require individuals to have a certain amount of cash to open accounts and have enough funds for trading fees and commissions. While there are no limits on how much can be contributed to the account, earned dividends are taxable in the year they are received. Therefore, if you earn a profit or sell an asset, you must pay a capital gains tax. On the other hand, if you sell a stock at a loss, that becomes a capital loss. This means that the transaction may yield a tax break by lowering your taxable income.

Pros and Cons of Maxing Out Your 401(k)

thumb_up

Pros:

• Increased Savings: More contributions added to a retirement savings plan could lead to more growth over time.

• Simplified Saving and Investing: Maxing out your 401(k) can also make your saving and investing relatively easy, as long as you’re taking a no-lift approach to setting your money aside thanks to automatic contributions.

thumb_down

Cons:

• Affordability: Maxing out a 401(k) may not be financially feasible for everyone. It may be challenging due to existing debt or other savings goals.

• Risk: Like all investments, there is the risk of loss.

• Opportunity Costs: Money invested in retirement plans could be used for other purposes. During strong stock market years, non-retirement investments may offer more immediate access to funds.

Test your understanding of what you just read.

The Takeaway

Maxing out your 401(k) involves matching your employer’s maximum contribution match, and also, contributing as much as legally allowed to your retirement plan in a given year. If you have the flexibility in your budget to do so, maxing out a 401(k) can be an effective way to build retirement savings.

And once a 401(k) is maxed out? There are other ways an individual might direct their money, including opening an IRA, or contributing more to an HSA or to a child’s 529 plan.

Prepare for your retirement with an individual retirement account (IRA). It’s easy to get started when you open a traditional or Roth IRA with SoFi. Whether you prefer a hands-on self-directed IRA through SoFi Securities or an automated robo IRA with SoFi Wealth, you can build a portfolio to help support your long-term goals while gaining access to tax-advantaged savings strategies.

Help build your nest egg with a SoFi IRA.

🛈 While SoFi does not offer 401(k) plans at this time, we do offer a range of Individual Retirement Accounts (IRAs).

FAQ

What happens if I max out my 401(k) every year?

Assuming you don’t overcontribute, you may see your retirement savings increase if you max out your 401(k) every year, and hopefully, be able to reach your retirement and savings goals sooner.

Will you have enough to retire after maxing out a 401(k)?

There are many factors that need to be considered to determine if you’ll have enough money to retire if you max out your 401(k). Start by getting a sense of how much you’ll need to retire by using a retirement expense calculator. Then you can decide whether maxing out your 401(k) for many years will be enough to get you there, assuming an average stock market return and compounding built in.

First and foremost, you’ll need to consider your lifestyle and where you plan on living after retirement. If you want to spend a lot in your later years, you’ll need more money. As such, a 401(k) may not be enough to get you through retirement all on its own, and you may need additional savings and investments to make sure you’ll have enough.

What is the best way to max out a 401(k)?

Some effective ways to max out a 401(k) include contributing up to the allowable amount for the year (for 2025, that’s $23,500 for those under age 50, and for 2026, it’s $24,500); using catch-up contributions if you’re aged 50 or older ($7,500 in 2025, and $8,000 in 2026, or $11,250 if you’re ages 60 to 63 in 2025 and 2026); contributing enough to get your employer’s matching contributions if offered; automating your contributions and increasing them yearly, if possible; and directing a percentage of any bonus you receive into your 401(k).

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Mutual Funds (MFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or clicking the prospectus link on the fund's respective page at sofi.com. You may also contact customer service at: 1.855.456.7634. Please read the prospectus carefully prior to investing.Mutual Funds must be bought and sold at NAV (Net Asset Value); unless otherwise noted in the prospectus, trades are only done once per day after the markets close. Investment returns are subject to risk, include the risk of loss. Shares may be worth more or less their original value when redeemed. The diversification of a mutual fund will not protect against loss. A mutual fund may not achieve its stated investment objective. Rebalancing and other activities within the fund may be subject to tax consequences.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

This article is not intended to be legal advice. Please consult an attorney for advice.

Retirement will likely be the most significant expense of your lifetime, which means saving for retirement is a big job. This is especially true if you envision a retirement that is rich with experiences such as traveling through Europe or spending time with your grown children and grandkids. A retirement savings plan may help you achieve these financial goals and stay on track.

There are all types of retirement plans you may consider to help you build your wealth, from 401(k)s to Individual Retirement Accounts (IRAs) to annuities. Understanding the nuances of these different retirement plans, like their tax benefits and various drawbacks, may help you choose the right mix of plans to achieve your financial goals.

Key Points

• There are various types of retirement plans, including traditional and non-traditional options, such as 401(k), IRA, Roth IRA, SEP IRA, and Cash-Balance Plan.

• Employers offer defined contribution plans (e.g., 401(k)) where employees contribute and have access to the funds, and defined benefit plans (e.g., Pension Plans) where employers invest for employees’ retirement.

• Different retirement plans have varying tax benefits, contribution limits, and employer matches, which should be considered when choosing a plan.

• Individual retirement plans like Traditional IRA and Roth IRA provide tax advantages but have contribution restrictions and penalties for early withdrawals.

• It’s possible to have multiple retirement plans, including different types and accounts of the same type, but there are limitations on tax benefits based on the IRS regulations.

🛈 SoFi does not offer employer-sponsored plans, such as 401(k) or 403(b) plans, but we do offer a range of individual retirement accounts (IRAs).

Types of Retirement Accounts

There are several different types of retirement plans, including some traditional plan types you may be familiar with as well as non-traditional options.

Traditional retirement plans can be IRA accounts or 401(k). These tax-deferred retirement plans allow you to contribute pre-tax dollars to an account. With a traditional IRA or 401(k), you only pay taxes on your investments when you withdraw from the account.

Non-traditional retirement accounts can include Roth 401(k)s and IRAs, for which you pay taxes on funds before contributing them to the account and withdraw money tax-free in retirement.

Here’s information about some of the most common retirement plan types:

There are typically two types of retirement plans offered by employers:

• Defined contribution plans (more common): The employee invests a portion of their paycheck into a retirement account. Sometimes, the employer will match up to a certain amount (e.g. up to 5%). In retirement, the employee has access to the funds they’ve invested. 401(k)s and Roth 401(k)s are examples of defined contribution plans.

• Defined benefit plans (less common): The employer invests money for retirement on behalf of the employee. Upon retirement, the employee receives a regular payment, which is typically calculated based on factors like the employee’s final or average salary, age, and length of service. As long as they meet the plan’s eligibility requirements, they will receive this fixed benefit (e.g. $100 per month). Pension plans and cash balance accounts are common examples of defined benefit plans.

Let’s get into the specific types of plans employers usually offer.

401(k) Plans

A 401(k) plan is a type of work retirement plan offered to the employees of a company. Traditional 401(k)s allow employees to contribute pre-tax dollars, where Roth 401(k)s allow after-tax contributions.

• Income Taxes: If you choose to make a pre-tax contribution, your contributions may reduce your taxable income. Additionally, the money will grow tax-deferred and you will pay taxes on the withdrawals in retirement. Some employers allow you to make after-tax or Roth contributions to a 401(k). You should check with your employer to see if those are options.

• Contribution Limit: $23,500 in 2025 and $24,500 in 2026 for the employee; people 50 and older can contribute an additional $7,500 in 2025 and $8,000 in 2026. However, in 2025 and 2026, under the SECURE 2.0 Act, a higher catch-up limit of $11,250 applies to individuals ages 60 to 63.

And under a new law that went into effect on January 1, 2026 (as part of SECURE 2.0), individuals aged 50 and older who earned more than $150,000 in FICA wages in 2025 are required to put their 401(k) catch-up contributions into a Roth 401(k) account. Because of the way Roth accounts work, these individuals will pay taxes on their catch-up contributions upfront, but can make eligible withdrawals tax-free in retirement.

• Pros: Money is deducted from your paycheck, automating the process of saving. Some companies offer a company match. There is a significantly higher limit than with Traditional IRA and Roth IRA accounts.

• Cons: With a 401(k) plan, you are largely at the mercy of your employer — there’s no guarantee they will pick plans that you feel are right for you or are cost effective for what they offer. Also, the value of a 401(k) comes from two things: the pre-tax contributions and the employer match, if your employer doesn’t match, a 401(k) may not be as valuable to an investor. There are also penalties for early withdrawals before age 59 ½, although there are some exceptions, including for certain public employees.

• Usually best for: Someone who works for a company that offers one, especially if the employer provides a matching contribution. A 401(k) retirement plan can also be especially useful for people who want to put retirement savings on autopilot.

• To consider: Sometimes 401(k) plans have account maintenance or other fees. Because a 401(k) plan is set up by your employer, investors only get to choose from the investment options they provide.

403(b) Plans

A 403(b) retirement plan is like a 401(k) for certain individuals employed by public schools, churches, and other tax-exempt organizations. Like a 401(k), there are both traditional and Roth 403(b) plans. However, not all employees may be able to access a Roth 403(b).

• Income Taxes: With a traditional 403(b) plan, you contribute pre-tax money into the account; the money will grow tax-deferred and you will pay taxes on the withdrawals in retirement. Additionally, some employers allow you to make after-tax or Roth contributions to a 403(b); the money will grow tax-deferred and you will not have to pay taxes on withdrawals in retirement. You should check with your employer to see if those are options.

• Contribution Limit: $23,500 in 2025 and $24,500 in 2026 for the employee; people 50 and older can contribute an additional $7,500 in 2025 and $8,000 in 2026. In 2025 and 2026, under the SECURE 2.0 Act, those ages 60 to 63 can contribute a higher catch-up amount of $11,250. As noted above with 401(k) plans, as of January 1, 2026, individuals aged 50 and older with FICA wages exceeding $150,000 in 2025 are required to put their catch-up contributions into a Roth account.

The maximum combined amount both the employer and the employee can contribute annually to the plan (not including the catch-up amounts) is generally the lesser of $70,000 in 2025 and $72,000 in 2026 or the employee’s most recent annual salary.

• Pros: Money is deducted from your paycheck, automating the process of saving. Some companies offer a company match. Also, these plans often come with lower administrative costs because they aren’t subject to Employee Retirement Income Security Act (ERISA) oversight.

• Cons: A 403(b) account generally lacks the same protection from creditors as plans with ERISA compliance.

• To consider: 403(b) plans offer a narrow choice of investments compared to other retirement savings plans. The IRS states these plans can only offer annuities provided through an insurance company and a custodial account invested in mutual funds.

Solo 401(k) Plans

A Solo 401(k) plan is essentially a one-person 401(k) plan for self-employed individuals or business owners with no employees, in which you are the employer and the employee. Solo 401(k) plans may also be called a Solo-k, Uni-k, or One-participant k.

• Income Taxes: The contributions made to the plan are tax-deductible.

• Contribution Limit: $23,500 in 2025 and $24,500 in 2026, or 100% of your earned income, whichever is lower, plus “employer” contributions of up to 25% of your compensation from the business. The 2025 total cannot exceed $70,000, and the 2026 total cannot exceed $72,000. (On top of that, people 50 and older are allowed to contribute an additional $7,500 in 2025 and $8,000 in 2026. In 2025 and 2026, those ages 60 to 63 can contribute a higher catch-up amount of $11,250 under the SECURE 2.0 Act .)

• Pros: A solo 401(k) retirement plan allows for large amounts of money to be invested with pre-tax dollars. It provides some of the benefits of a traditional 401(k) for those who don’t have access to a traditional employer-sponsored 401(k) retirement account.

• Cons: You can’t open a solo 401(k) if you have any employees (though you can hire your spouse so they can also contribute to the plan as an employee — and you can match their contributions as the employer).

• Usually best for: Self-employed people with enough income and a large enough business to fully use the plan.

SIMPLE IRA Plans (Savings Incentive Match Plans for Employees)

A SIMPLE IRA plan is set up by an employer, who is required to contribute on employees’ behalf, although employees are not required to contribute.

• Income Taxes: Employee contributions are made with pre-tax dollars. Additionally, the money will grow tax-deferred and employees will pay taxes on the withdrawals in retirement.

• Contribution Limit: $16,500 in 2025 and $17,000 in 2026. Employees aged 50 and over can contribute an extra $3,500 in 2025 and $4,000 in 2026, bringing their total to $20,000 in 2025 and $21,000 in 2026. In 2025 and 2026, under the SECURE 2.0 Act, people ages 60 to 63 can contribute a higher catch-up amount of $5,250.

• Pros: Employers contribute to eligible employees’ retirement accounts at 2% their salaries, whether or not the employees contribute themselves. For employees who do contribute, the company will match up to 3%.

• Cons: The contribution limits for employees are lower than in a 401(k) and the penalties for early withdrawals — up to 25% for withdrawals within two years of your first contribution to the plan — before age 59 ½ may be higher.

• To consider: Only employers with less than 100 employees are allowed to participate.

This is a retirement account established by a small business owner or self-employed person for themselves (and if applicable, any employees).

• Income Taxes: Your contributions will reduce your taxable income. Additionally, the money will grow tax-deferred and you will pay taxes on withdrawals in retirement.

• Contribution Limit: For 2025, $70,000 or 25% of earned income, whichever is lower; for 2026, $72,000 or 25% of earned income, whichever is lower.

• Pros: Higher contribution limit than IRA and Roth IRAs, and contributions are tax deductible for the business owner.

• Cons: These plans are employer contribution only and greatly rely on the financial wherewithal and available cash of the business itself.

• Usually best for: Self-employed people and small business owners who wish to contribute to an IRA for themselves and/or their employees.

• To consider: Because you’re setting up a retirement plan for a business, there’s more paperwork and unique rules. When opening an employer-sponsored retirement plan, it generally helps to consult a tax advisor.

Profit-Sharing Plans (PSPs)

A Profit-Sharing Plan is a retirement plan funded by discretionary employer contributions that gives employees a share in the profits of a company.

• Income taxes: Deferred; assessed on distributions from the account in retirement.

• Contribution Limit: The lesser of 25% of the employee’s compensation or $70,000 in 2025 (On top of that, people 50 and older are allowed to contribute an additional $7,500 in 2025. And people ages 60 to 63 can make a higher contribution of $11,250 in 2025 under SECURE 2.0.) In 2026, the contribution limit is $72,000 or 25% of the employee’s compensation, whichever is less. Those 50 and up can contribute an extra $7,500 in 2025 and $8,000 in 2026. And people ages 60 to 63 can once again make a higher contribution of $11,250 in 2026 under SECURE 2.0.

• Pros: An employee receives a percentage of a company’s profits based on its earnings. Companies can set these up in addition to other qualified retirement plans, and make contributions on a completely voluntary basis.