4 Student Loan Repayment Options — and How to Choose the Right One for You

Table of Contents

It’s never too early to think about student loan repayment. Whether you’re still in college, or you recently graduated and are in the grace period before repayment begins, strategizing now can help you weigh the options.

If you’ve graduated and are already working and making payments, it can be a good idea to re-evaluate your repayment plan over time. As your financial circumstances change, the way you’d like to manage your student loans may also shift.

Before considering your options, take inventory of all your student loans. Be sure to list the principal, the interest rate, the repayment period, and the servicer for each loan.

All federal student loans issued in recent years have fixed interest rates, but private student loans or older federal student loans may have variable rates. If the rate is variable, be sure to note that as well.

Key Points

• The Standard Repayment Plan is the default option for federal student loans, offering fixed payments over 10 years, but it may not be the most cost-effective for everyone.

• Income-Driven Repayment Plans adjust payments based on discretionary income and can lead to loan forgiveness after 20-25 years, though they may increase total interest paid.

• Student Loan Forgiveness Programs are available for certain borrowers, such as those in public service or teaching, but require meeting eligibility criteria like 120 qualifying payments.

• Student Loan Consolidation allows federal borrowers to combine multiple loans into one with a single payment, but it does not lower interest rates.

• Student Loan Refinancing can reduce interest rates and lower payments, but refinancing federal loans with a private lender eliminates federal protections and repayment options.

Different Student Loan Repayment Options

Once you understand the details of your student loans, it’s time to think about your repayment options. The simple choice if you have federal student loans is the Standard Repayment Plan. It’s the “default” repayment plan, so unless you sign up for another option, this is the plan you’ll have. Under the Standard plan, you typically pay a fixed amount every month for up to 10 years.

There is no “standard repayment plan” for private student loans; the interest rate may vary based on market factors, and your repayment term might be shorter or longer.

The federal government also offers graduated and extended repayment plans for borrowers. With the Graduated Repayment Plan, payments start smaller and grow over time, while the Extended Repayment Plan stretches repayment over a period of up to 25 years and payments may be either fixed or graduated.

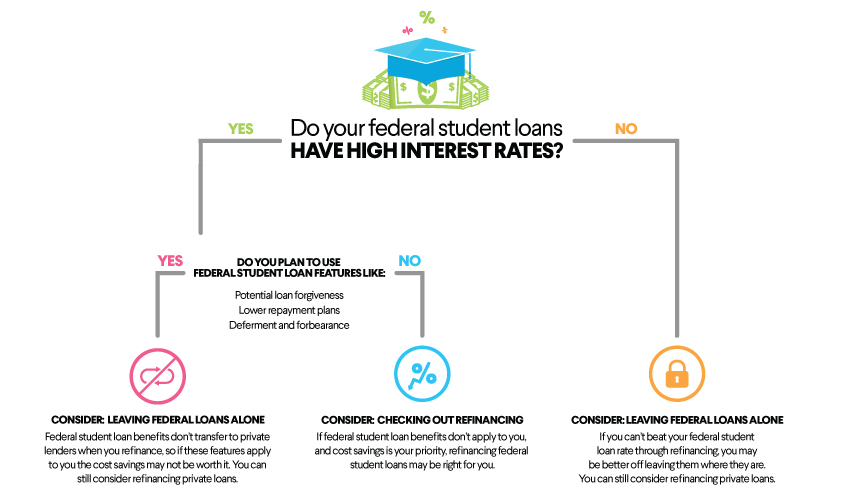

Opting for the Standard Repayment Plan may work for you, but for some borrowers, it’s not the most cost-effective choice. These borrowers may be eligible for special federal programs that can reduce the amount they owe monthly based on financial circumstances, and in some cases, forgive balances if they meet certain requirements.

Or some borrowers might be able to find a more competitive interest rate by refinancing their loans through private lenders.

💡 Quick Tip: Often, the main goal of refinancing is to lower the interest rate on your student loans — federal and/or private — by taking out one loan with a new rate to replace your existing loans. Refinancing may make sense if you qualify for a lower rate and you don’t plan to use federal repayment programs or protections, since refinancing federal loans makes them ineligible for federal benefits.

Here’s an overview of some student loan repayment options that may help if you are choosing a repayment plan:

1. Student Loan Consolidation

Federal student loan consolidation allows you to combine multiple federal student loans into a single new loan. You can’t consolidate private student loans using this federal program.

When you consolidate your federal student loans into a Direct Consolidation Loan, your new loan’s interest rate will be the weighted average of all your old student loans’ interest rates, rounded up to the nearest one-eighth of a percent. This means your interest rate won’t necessarily be lower than the rate you were paying before consolidation on some of your student loans — in fact, it could be slightly higher.

When you consolidate, you’ll also have the option to select a new repayment plan. The standard plan would still be available, but consolidation can also be a first step toward other plans of action, like student loan forgiveness or income-driven repayment.

2. Student Loan Forgiveness

Federal student loans are eligible for student loan forgiveness programs, and private student loans may qualify for some loan repayment assistance programs. For instance, some federal student loans and Direct Consolidation Loans are eligible for modified payment plans that forgive outstanding student loan balances.

Health care professionals, teachers, military service members, and those employed full-time by qualifying nonprofit or public service organizations may be eligible for certain federal student loan forgiveness programs. Some states and employers offer loan repayment assistance toward both federal and private loans for eligible workers.

Under the Public Service Loan Forgiveness (PSLF) program, those who have worked for qualified employers, such as the government or some nonprofit agencies, and have made 10 years of payments on a qualified income-driven repayment plan, can apply for forgiveness of all of their remaining federal student loan balances. That forgiveness is not considered taxable income.

The Federal Student Aid website has additional information on which federal student loans qualify for which types of forgiveness, cancellation, and/or discharge.

3. Income-Based Repayment

If the payments under the Standard Repayment Plan seem too high, federal student loans offer income-driven repayment plans, which tie the amount you pay to your discretionary income. The currently available options are Income-Based Repayment, Income-Contingent Repayment, and Pay As You Earn.

Income-driven repayment plans may help lower your monthly payments. In some cases, however, you might end up paying more over the life of the loan than you would have on the Standard Repayment Plan. That’s because with low monthly payments that stretch out over more years, you could be paying more in interest over time.

Additionally, with income-driven repayment plans, you may be eligible for student loan forgiveness if the remainder of your student loans aren’t paid off after 20 to 25 years of consistent, on-time payments.

4. Student Loan Refinancing

Refinancing student loans through a private lender offers the opportunity to consolidate multiple student loans into a single payment and potentially decrease your interest rate or lower your monthly payment.

Loan repayment terms vary based on the lender, and borrowers with better credit and earning potential (among other financial factors that vary by lender) may qualify for better terms and interest rates.

One important thing to know about refinancing, however, is that once you refinance a federal student loan into a private loan, you can’t undo that transaction and later consolidate back into a federal Direct Consolidation Loan.

This can be relevant for professionals in health care or education where federal student loan forgiveness plans are offered, or for those considering long-term employment in the public sector.

In addition, refinancing federal student loans with a private lender renders them ineligible for important borrower benefits and protections, like income-driven repayment and deferment.

💡 Quick Tip: When refinancing a student loan, you may shorten or extend the loan term. Shortening your loan term may result in higher monthly payments but significantly less total interest paid. A longer loan term typically results in lower monthly payments but more total interest paid.

Can You Change Your Student Loan Repayment Plan?

If you have federal student loans, it is possible to change your repayment plan at any time, without any fees. You’ll have the option to choose from any of the federal repayment plan options, including income-driven repayment plans.

There is less flexibility to change the terms of a private student loan. Some private lenders may offer alternative payment plans for borrowers. Check with your lender directly to see what options may be available to you.

Recommended: Student Loan Calculator

SoFi Student Loan Refinancing

Refinancing is another avenue that can result in a new repayment plan. An important consideration, however, is that refinancing federal student loans will remove them from any federal programs or protections, so this won’t be the right choice for everyone.

The Takeaway

Federal student loan borrowers have the ability to change their repayment plan at any time, without being charged any fees. There are different plans to choose from, and you can look for one that suits your situation and needs.

Changing your repayment plan is a bit more challenging for private student loans, though some private lenders may offer alternative options for borrowers. Refinancing is another option that could allow some borrowers to adjust their repayment terms.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

FAQ

What student loan repayment options are available to me?

Borrowers with federal student loans can choose from various federal repayment plans, including the standard 10-year repayment plan and income-driven repayment options. The SAVE plan, which was introduced by the Biden Administration at the end of June 2023, is no longer available. For private student loans, repayment options will be determined by the lender.

What is a standard repayment plan for student loans?

The Standard Repayment Plan for federal student loans involves fixed monthly payments over a period of 10 years. For consolidation loans, repayment may extend up to 30 years, depending on the loan amount.

How long is a typical student loan repayment?

The typical student loan repayment period may vary from individual to individual. The Standard Repayment Plan for federal loans is 10 years, but income-driven repayment plans or Direct Consolidation loans may have a term of up to 25 to 30 years. The repayment terms for private student loans vary by lender.

SoFi Student Loan Refinance SoFi Loan Products

Terms and conditions apply. SoFi Refinance Student Loans are private loans. When you refinance federal loans with a SoFi loan, YOU FORFEIT YOUR ELIGIBILITY FOR ALL FEDERAL LOAN BENEFITS, including all flexible federal repayment and forgiveness options that are or may become available to federal student loan borrowers including, but not limited to: Public Service Loan Forgiveness (PSLF), Income-Based Repayment, Income-Contingent Repayment, extended repayment plans, PAYE or SAVE. Lowest rates reserved for the most creditworthy borrowers. Learn more at SoFi.com/eligibility. SoFi Refinance Student Loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOSLR-Q225-044

Read more