If so, you are in the right place! Get started by entering your personal confirmation number below.

Received an offer from us?

If so, you are in the right place! Get started by entering your personal confirmation number below.

Leaving SoFi Website

You are now leaving the SoFi website and entering a third-party website. SoFi has no control over the content, products or services offered nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. SoFi does not guarantee or endorse the products, information or recommendations provided in any third party website.

By Wesley Yu |

Uncategorized |

Comments Off on LCM | ACAT 1% IRA ACQ

{/* OFFER – HERO */}

{/* OFFER – Banner */}

SoFi Invest®

{/* OFFER – Title */}

{/* OFFER – Description */} Get a 1% ACAT Match.

For a limited time only, get a 1% match when you transfer your IRA to SoFi. Offer ends 3/31/26. Terms apply.*

{/* DISCLOSURE CONTENT */}

{/* INSERT DISCLOSURE’S HERE */}

SoFi Self-directed IRA ACAT 1% Match Terms & Conditions

The SoFi Self-directed IRA ACAT 1% Match is governed by the following Terms & Conditions:

Offer: SoFi will match 1% of a customer's ACAT transfers, subject to a maximum match of $10,000 (equivalent to 1% of up to $1,000,000 in ACAT transfers), into their existing or newly opened SoFi self-directed individual retirement account (IRA) during the Offer Period. Transfers must be maintained in the IRA account for five (5) years from the settlement date. Matches will be paid in cash within 5 business days from the date which the funds settle in your SoFi self-directed IRA account.

Offer Period: The Offer Period is from February 17, 2026 - March 31, 2026, though SoFi may modify, suspend, or terminate the Offer at any time without advance notice.

Eligibility: The Match is available to customers who have an existing or newly opened SoFi self-directed IRA (Traditional IRA or Roth IRA) in good standing during the Offer Period through SoFi Securities LLC. Only asset transfers via ACAT are eligible. The transferred assets must be settled before the end of the Offer Period to be eligible for the match.

Calculations and Payments: Matches will be paid out in cash into the account the ACAT was transferred into within 5 business days of the settlement date. The 1% Match is calculated based on the total assets transferred (via ACAT). The customer's SoFi Invest IRA account must be in good standing to receive the payout.

Example: If you complete an ACAT of $20,000 into a SoFi Self-directed Traditional IRA during the Offer Period, you will be matched 1%, equaling $200.

Limitations: This Offer may not be combined with any other offers. The Match will not exceed $10,000 (equivalent to 1% of up to $1,000,000 in ACAT transfers). Qualifying deposits must remain in the SoFi IRA account that earned the Match for five (5) years to keep the entire match amount. If a member makes a withdrawal before the five (5) year Holding Period is complete, they will be subject to an early withdrawal fee and SoFi will remove a proportional amount of the Match from the member's account. The proportional amount is based on the breach in retention value, not retention period.

To avoid this fee, the total equity of the member's account ("total equity") must remain at the original pre-promotion total equity in the account, plus the qualifying deposit and match amount. If a withdrawal causes the total equity to fall below this combined amount, the fee will be applied. The fee will also apply if the member initiates a withdrawal and the total equity has decreased, for any reason including investment losses. Distributions required by law (e.g., required minimum distributions in IRAS) can also trigger the fee. However, the fee will not apply if the member's total equity has risen by an amount greater than the withdrawal amount, either by investment gains or additional deposits.

The proportional early withdrawal fee is deducted from the requested withdrawal amount. In the event of an ACAT transfer out, there will be an early withdrawal fee for the entire match amount. If insufficient cash is available in this account, the fee will be debited from an outgoing financial institution or added to a margin balance. SoFi reserves the right to liquidate securities to pay for this early withdrawal fee. SoFi will also bill an ACAT out fee separate from an early withdrawal fee. For additional details on the SoFi fee schedule click here.

Examples:

Asset Transfer (ACAT)

1% Match

Total Equity Balance

Withdrawal Date

Withdrawal Amount

Remaining Equity Balance

Early Withdrawal Fee

$20,000

$200

$20,200

5+ years from deposit date

-$2,000

$18,200

$0 (earned full match amount)

$20,000

$200

$20,200

Less than 5 years from deposit date

-$2,000

$18,200

$19.80

$20,000

$200

$25,000 Account balance increases due to investments

Less than 5 years from deposit date

-$2,000

$23,200

$0

$20,000

$200

$15,000 Account balance decreases due to investments

Less than 5 years from deposit date

-$2,000

$13,000

$71.29

Fraud and Violations: SoFi reserves the right to decline, rescind, or delay granting the 1% Match if fraudulent activity or violations of these Terms are suspected. SoFi will liquidate any security to recover the match amount if required.

Not a Recommendation: This Match is not a recommendation to buy, sell, or hold any security, nor is the Offer a recommendation or endorsement of any investment strategy. The Match is not a recommendation that a customer rollover or transfer assets into a SoFi IRA, nor a recommendation for any specific account type. There are many factors that an investor should consider before initiating a rollover as it is one of a few options. An investor should consult with a qualified advisor prior to initiating a transfer or rollover. Customers that wish to participate in the Match are acknowledging the offer is not investment advice and are participating in the Match voluntarily.

Taxes: The Match is treated as taxable income as determined by applicable tax guidance and does not impact contribution limits. Recipient is responsible for any applicable federal, state or local taxes associated with receiving the offer; consult with your tax advisor to determine applicable tax consequences. Each investor's tax situation is unique, and SoFi does not provide tax advice.

Disclosures: SoFi reserves the right to change or terminate the Match at any time without notice. The Match is not transferable, saleable, or valid in conjunction with other offers and is available to U.S. residents for personal, non-commercial use only. Participation in this Match constitutes acceptance of these Terms.

{/* CTA Mobile */}

{

(window.Android || window.callbackHandler).postMessage(JSON.stringify({

name: ‘onClose’,

value: ‘onClose’,

actionUrl: ‘https://sofi.app.link/sign-up-retirement/’

}));

}}

>

Open an account

The contribution limit for a traditional IRA in 2025 is $7,000 or $8,000 for those age 50 and older. In 2026, the limit is $7,500 or $8,600 for those age 50 and older.

Tip: The annual IRA contribution limit applies to all your IRA accounts combined, including both Traditional and Roth IRAs.

Eligibility criteria for traditional IRA contributions.

There are some criteria regarding income eligibility that you should be aware of as you’re getting ready to make contributions to a traditional IRA.

Contributions must be made with earned income.

The following are IRS-approved sources of earned income:

• Wages, salaries, and tips from which federal income taxes are withheld.

• Income from a job from which an employer did not withhold taxes, such as freelance work.

• Self-employed income.

Traditional IRAs have no income limit.

In other words, no matter how much money you make, you can contribute to a traditional IRA. By contrast, Roth IRAs do have income limits.

No age limit.

There is no age limit to contribute to a traditional IRA.

2025 Traditional IRA income and tax deductibility limits.

While income doesn’t determine eligibility to contribute to a traditional IRA, it can have an impact on deductible contributions if an individual or their spouse has a retirement plan at work and their income exceeds a certain level. The chart below outlines traditional IRA contributions limits for 2025 based on filing status and whether you or your spouse are covered by an employer-sponsored retirement plan.

Filing status

Modified adjusted gross income (MAGI)

Deduction limit

Single or head of household (and you are covered by an employer-sponsored retirement plan.)

$79,000 or less

Full deduction

More than $79,000 and less than $89,000

Partial deduction

$89,000 or more

No deduction

Married filing jointly (and you are covered by an employer-sponsored retirement plan.)

$126,000 or less

Full deduction

More than $126,000 but less than $146,000

Partial deduction

$146,000 or more

No deduction

Married filing jointly (and your spouse is covered by an employer-sponsored retirement plan.)

$236,000 or less

Full deduction

More than $236,000 but less than $246,000

Partial deduction

$246,000 or more

No deduction

Married filing separately (and you or your spouse are covered by an employer-sponsored retirement plan.)

This error can be costly. Excess funds are taxed at 6% for each year they remain in the IRA. However, individuals can avoid this tax by withdrawing excess contributions by the due date of their individual tax return. They must also withdraw any income earned on the excess funds during that period. However you will need to report those earnings as income on your tax return. And you may have to pay a 10% penalty for early withdrawal of the earnings if you are under age 59½.

Strategies to Avoid Excess Contributions

It’s also important to be aware that the IRA contribution limit is a combined maximum for all the IRAs you may have, including Roth IRAs. So your contributions to a traditional IRA and a Roth IRA cannot exceed the overall yearly contribution limit, which in 2025 is $7,000 for those under age 50 and $8,000 for those 50 and older. In 2026, those limits change to $7,500 for those under age 50 and $8,600 for those 50 and older.

Is there an income limit to contribute to a traditional IRA?

No, there is no income limit to contribute to a traditional IRA. Individuals, regardless of their income, can contribute $7,000 to a traditional IRA in 2025 (or $8,000 if they are age 50 or older). In 2026, they can contribute $7,500 to a traditional IRA in 2025 (or $8,600 if they are age 50 or older).

Does contributing to a traditional IRA reduce taxable income?

Contributing to a traditional IRA may reduce your taxable income for the year. However, some or all of your contributions may be ineligible for tax deduction depending on your income and whether or not you or a spouse is covered by a retirement plan at work.

Can I max out a 401(k) and a traditional IRA in the same year?

Yes, you can max out a 401(k) and a traditional IRA in the same year. You can contribute up to $23,500 to a 401(k) in 2025 (or up to $31,000 for those age 50 and older), and you can also contribute up to $7,000 in a traditional IRA (or up to $8,000 for those 50 and older) in 2025.

For 2026, you can contribute up to $24,500 in a 401(k) (or up to $32,500 for those age 50 and older), and you can also contribute up to $7,500 in a traditional IRA (or up to $8,600 for those 50 and older).

Note that those age 60-63 may contribute a higher 401(k) catch-up contribution of up to $11,250 in both 2025 and 2026 due to a SECURE 2.0 provision.

Also, under a new law that went into effect on January 1, 2026 as part of SECURE 2.0, individuals aged 50 and older who earned more than $150,000 in FICA wages in 2025 are required to put their 401(k) catch-up contributions into a Roth 401(k) account.

A mortgage refinance swaps out your old mortgage with a new one, including a fresh set of terms and interest rate. It may or may not come with financial benefits, depending on your goals and how a new loan quote stacks up against your existing home loan.

In this guide to refinancing a mortgage, you’ll learn how a mortgage refinance works and how you qualify for refinancing. We’ll walk you through what a refinance application is like and explain how much you can borrow when you refinance. Get the lowdown on the pros and cons of refinancing your mortgage.

• Mortgage refinancing requirements are similar to applying for your original home loan.

• Your home must be appraised before you can close on a refinanced mortgage.

• Comparing multiple lenders ensures you find the best terms available.

• Refinancing doesn’t necessarily save you money, so weigh all of your options carefully.

What is Mortgage Refinancing?

Refinancing a mortgage is when you get a new mortgage with different terms from the old one. The new lender pays off the original balance you owed, then begins to receive payments from you.

People refinance for a number of reasons, such as qualifying for a lower interest rate, changing the payment term, or cashing out some of their equity. In order to refinance your home loan, you need to submit a full application, get a home appraisal, and pay closing costs.

Consequently, you should have a clear financial goal in mind that makes up for the time and expense of mortgage refinancing.

Mortgage Refinancing Requirements

• Credit score: Most lenders require a minimum score based on the type of mortgage you’re applying for. For a conventional loan, a score of 620 or better is the norm.

• Equity: If you’re doing a cash-out refinance, you’ll need enough equity to cover the new mortgage balance plus the amount of money you want to borrow against the property.

• Debt: The lender evaluates your current debt load along with the new mortgage payment to make sure it’s affordable.

• Income: Your debt-to-income ratio is calculated to compare how much of your income is put toward debt payments each month (including your mortgage). Each lender has its own requirement, but it’s usually 50% or less.

• Employment verification: You must verify that you have steady income, often with recent pay stubs or federal tax returns.

• Assets for closing costs: Just as with any other home loan, you’ll have to show you have the funds to cover closing costs. Closing costs for a refinance range from 2% to 5% of your loan amount.

• Appraisal: Your home must be appraised to make sure the value is equal to or greater than your new mortgage balance.

If you meet these refinancing mortgage requirements, you’re ready to start the qualification process.

How to Qualify for Mortgage Refinancing

You’re ready to apply, but how does mortgage refinancing work? You can check your eligibility and request lender quotes before you get too far into the application. The mortgage preapproval process is an evaluation with a lender that looks at your credit and income to determine whether or not you meet the mortgage refinance requirements.

You can also look at different types of mortgages and cash-out options with estimated monthly payments before you go through underwriting. Once you have a loan quote you like and the loan officer is confident in your preapproval, your application moves to the underwriting process.

At this point, you may be asked to submit extra documentation and you’ll also need to pay for the appraisal. Home appraisal fees range from $300 to $600, and you usually must pay for it at the time the service is completed.

How Does Mortgage Refinancing Work?

You understand the basic process, but how does refinancing a mortgage work in terms of updating your loan?

Here’s what happens: Depending on your financial situation and your existing mortgage, you may want to change the terms of your home loan (we’ll get to potential reasons to do this in a bit). You typically can’t negotiate those terms with the lender, so you can instead shop around for a new mortgage at different lenders (you can also include your original lender in your search).

Once you find new loan terms that fit your goals, you go through the refinancing application process. After closing, the new lender pays off your mortgage balance with the old lender. Then you start making payments on your new loan according to the updated terms.

Common loan terms that can be changed with a refinanced mortgage include:

• Interest rate (amount and type, such as fixed or adjustable)

• Length of loan term

• Mortgage insurance

• Loan balance

On average, it takes 30 to 45 days to refinance a mortgage.

Types of Mortgage Refinancing

There are several types of mortgage refinancing options, whether you’re trying to lower your cost of living, change your loan term, or get a different rate. Each option depends on your goals and eligibility.

• Rate and term: A rate and term refinance is when you get a new loan in order to access a different rate, loan term, or both. Refinancing mortgage rates could be lower, or you could swap an adjustable-rate loan for a new loan before your current rate adjusts.

• Cash-out refinance: A cash-out refinance allows you to borrow more money than you currently owe. You receive the cash based on your equity and take out a larger mortgage balance, which can be used for just about anything.

• Cash-in refinance: A cash-in refinance is the opposite, where you take out a new mortgage and pay a lump sum to pay down the mortgage balance. This increases your equity and could help you qualify for better loan terms, especially if you made a low down payment when you first purchased your home.

• Streamline refinance: Some borrowers may be eligible for a streamline refinance with government-guaranteed loans for existing FHA, VA, and USDA mortgages. Usually the application process is quicker. The goal is to lower your monthly payments.

• No-closing-cost refinance: While some refinances may be advertised as having “no closing costs,” the term is misleading. You still have to pay closing costs, but you will either roll them into the new mortgage balance or pay them in the form of a higher interest rate.

How Is Mortgage Refinancing Calculated?

You can use an online mortgage refinancing calculator to compare new loan terms to your existing ones. Here is the information you’ll need to see how your payments and overall costs stack up:

• Current mortgage payment and interest rate

• Remaining balance

• Remaining loan term in years

• New interest rate

• New loan term in years

• Refinancing fee estimates

Once you enter in all of these details, you’ll see an estimate of your new monthly payment, along with a comparison of any potential savings (or extra costs) in interest over time. Finally, the calculator will show you how many months it will take to recoup the costs of refinancing so you can estimate whether or not you plan to live in the home that long. “It’s important to understand that not every mortgage refinance will save you money on interest. For example, if you extend the repayment term, you may have smaller monthly payments, but you’ll end up paying more money over the course of the loan,” says -Brian Walsh, CFP® and Head of Advice & Planning at SoFi.

How Much Can You Borrow With Mortgage Refinancing?

With a rate and term refinance, you’ll borrow the same amount as your existing mortgage balance, unless you decide to roll in some closing costs or pay down a lump sum of your loan.

With a cash-out refinance, you can borrow up to 80% of your home’s value. That means you would subtract your outstanding mortgage balance from 80% of the appraised value, and that’s the amount you could borrow — assuming you meet the requirements to handle the new payments.

The cash-out funds can be used however you’d like. Many homeowners use the funds to pay off other debts, pay for home renovations, or cover education expenses. In recent years, the number of cash-out refinances has increased alongside the cost of living in the U.S.

How to Apply for Mortgage Refinancing

Here are the steps for refinancing a mortgage explained.

1. Research lenders based on your refinance goals.

2. Get prequalified for a new mortgage with several lenders based on the terms you’re looking for.

3. Choose a lender based on its provided loan estimates.

4. Submit a formal application, along with financial documents such as bank statements, pay stubs, and tax returns.

5. Answer any questions from your loan officer or underwriter to keep your application on track.

6. Get an appraisal on your home.

7. Review your closing disclosure and sign your new loan agreement.

After you complete your closing, the new lender pays off your old mortgage balance from the previous lender.

As you consider refinancing your mortgage, here are some benefits and drawbacks to consider.

thumb_up

Pros:

• Potential for lower interest rate

• Monthly payment could decrease

• Access equity with a cash-out refinance

• May remove private mortgage insurance

thumb_down

Cons:

• Resetting your loan term could lead to paying more total interest over time

• A cash-out could increase your loan balance and monthly payments

• Closing costs impact any potential savings

Who Should Get Mortgage Refinancing

Is mortgage refinancing right for you? There are several scenarios when it makes sense (and some when it doesn’t).

You plan to stay in your home for a while: Make sure you plan to live in your home for at least the next few years. Even if a refinance saves you money, it takes time to recoup the closing costs.

You qualify for a better interest rate: Whether rates have dropped since you got your original mortgage or your credit score has increased since you qualified as a first-time homebuyer, you could save money over time.

Your adjustable rate is about to change: Refinancing can help you switch from an adjustable rate to a fixed one. If your rate is about to adjust, compare fixed rate options to see what’s a better deal.

You have an FHA loan and 20% equity: Your annual FHA mortgage insurance premium may be permanent if you took out your original loan after 2013 and your down payment was less than 10%. In this scenario, the only way to stop paying the premium is to refinance.

When to Refinance a Mortgage

In addition to the scenarios above, there are a few things you should track when choosing the best time to refinance.

• Your credit score: Avoid refinancing at the same time you’re seeking financing for other major purchases, like a car.

• Your home equity: Look at sale prices on recently sold homes in your neighborhood to estimate how much yours could be worth or search your property on a real estate site. This gives you an idea of how much equity you may have.

What Are Mortgage Refinancing Rates Expected to Do in 2026?

Average mortgage interest rates for a 30-year loan have drifted downward, hitting a roughly two-year low of 6.06% by mid-January 2026, according to Freddie Mac. Some forecasters expect the 30-year loan rate to drop to 5.50% by mid-2026, though whether this will happen will depend on larger economic forces such as inflation.

Mortgage Refinancing Examples

Here are two examples of how it might look to refinance a mortgage:

1. Rate and term refinance: A homeowner with an FHA mortgage reaches 20% equity in his home. Average monthly expenses have increased, so he wants to cut costs in other areas. He pays 0.5% of his mortgage balance each year in FHA mortgage insurance premium, which is about $1,500 on his $300,000 balance. Refinancing to a conventional loan would save $125 per month, and even more if he can get a lower rate.

2. Cash-out refinance: A married couple has lived in their home for seven years. Over that time, their home value has increased from $250,000 to $500,000, leaving them with more than $250,000 in equity after making payments over the years. Their daughter is about to head to college and they want to tap into their equity to help pay for it. But since their mortgage rate is fixed at 3.99%, they end up opting for a home equity line of credit (HELOC) instead of a cash-out refinance in order to preserve that lower rate.

How Much Does It Cost to Refinance a Mortgage?

There are a number of costs involved with refinancing a mortgage, including:

Your original mortgage lender may also charge a prepayment penalty for closing the loan early. This fee is rare, but it’s still worth researching so you’re not surprised. If you have a jumbo loan, you may also have some extra-large costs associated with refinancing so carefully consider what you will spend on a refinance vs. what you will save.

How to Find Competitive Refinance Rates

To get the best rates and lowest overall cost in a refinance, compare at least three different lenders. Remember, even if a simple interest rate is lower, hefty lender fees could negate any savings.

Mortgage Refinancing vs. HELOC

Both a cash-out refinance and a home equity line of credit (HELOC) allow you to tap into your home’s value, but there are different pros and cons to each option. One key difference is that a HELOC allows you to borrow only as much as you need at any given time, while a cash-out refi will deliver one lump sum payment. Here’s how the differences lineup:

Cash-out mortgage refinance

HELOC

• Fixed interest rate • One lump-sum loan • Rates are usually lower than a HELOC • Interest paid for entire balance for entire mortgage term • Higher closing costs

• Interest is usually variable • Draw funds only as you need them • Rates may be higher than a refi • Interest only accrues on your balance • Minimal closing costs • Line of credit replenishes as you pay off balance

Alternatives to Mortgage Refinancing

There are a few other options to consider if refinancing doesn’t feel like a perfect fit.

Recasting: Instead of refinancing with a new loan, you could make a large payment to your existing lender and request that the lender recast your loan. The lender then lowers the balance and re-amortizes your payments so they reflect the lower balance. This is a good solution if you’re looking to lower your monthly expenses and you have cash on hand.

Make extra payments: If you’re considering refinancing to shorten your loan term, you could simply pay more principal each month without getting a new mortgage. You’d still pay off your loan sooner and wouldn’t have to pay closing costs or lose a competitive interest rate if you have one.

Move to a new location: If you need to lower your monthly mortgage payments — or expenses generally — consider moving to a more affordable area where your money could go further.

The Takeaway

Borrowers have two options for a mortgage refinance: a new loan with terms or rates that will ideally lower your monthly payment, or a cash-out refinance that won’t necessarily save you money but can free up funds to help you meet other financial goals. Refinancing is a similar process to applying for a home loan, so consider the decision carefully. Examine the costs associated and consider how long you expect to own your home before committing to a refinance with a lender you can trust.

SoFi can help you save money when you refinance your mortgage. Plus, we make sure the process is as stress-free and transparent as possible. SoFi offers competitive fixed rates on a traditional mortgage refinance or cash-out refinance.

A mortgage refinance could be a game changer for your finances.

FAQ

What is the point of refinancing a mortgage?

Refinancing usually comes with a couple of different outcomes: changing your rate and term with an eye to lowering monthly payments, total interest paid, or both; cashing out some of your equity; or paying off a large chunk of your mortgage to lower your payments.

What are the risks of refinancing a home?

There are risks if the costs of refinancing don’t outweigh the benefits, so you could end up paying more than with your original mortgage. If you choose a cash-out refinance, you use your home as collateral for borrowing a lump sum of money.

Is it ever a good idea to refinance your house?

It could be a good idea to refinance your house if you can reduce your monthly mortgage payment, save on interest, pay off your loan faster, or access funds for renovations or another big expense at a relatively low interest rate.

Do you get money when you refinance your home?

You only get money when you refinance if you choose a cash-out refinance. With this option, you take out a larger mortgage than your current balance and receive the difference as cash.

Does refinancing hurt your credit?

You may see a slight dip in your credit score when you first apply to refinance your mortgage, simply because of the new inquiry on your credit report. Be sure to keep up with on-time payments when you transition between loans; otherwise you could hurt your score with a late payment.

Is it good or bad to refinance a loan?

Whether or not refinancing is a good idea depends on your goals and your loan terms. If you can save money with a lower interest rate, it could be a good thing — provided you own your home long enough to recoup the closing costs on the refi. But you could end up with larger monthly payments, especially if you cash out some of your equity.

Refinance your way to a better mortgage with SoFi.

By Mario Ismailanji |

|

Comments Off on January 2026 Market Lookback

Political Fuel Meets Fire

The firewall between the executive branch and the central bank was breached in January. Markets were rattled by the unprecedented Justice Department investigation into the Fed’s $2.5 billion renovation of its headquarters as well as the high-stakes Supreme Court case triggered by President Trump’s attempt to remove Fed Governor Lisa Cook.

The political fallout is even complicating the president’s recent nomination of Kevin Warsh as the next Fed Chair. Sen. Thom Tillis, a Republican from North Carolina who is on the Senate Banking Committee that must vote on Fed nominations, said he would block any vote until the Fed investigation is resolved.

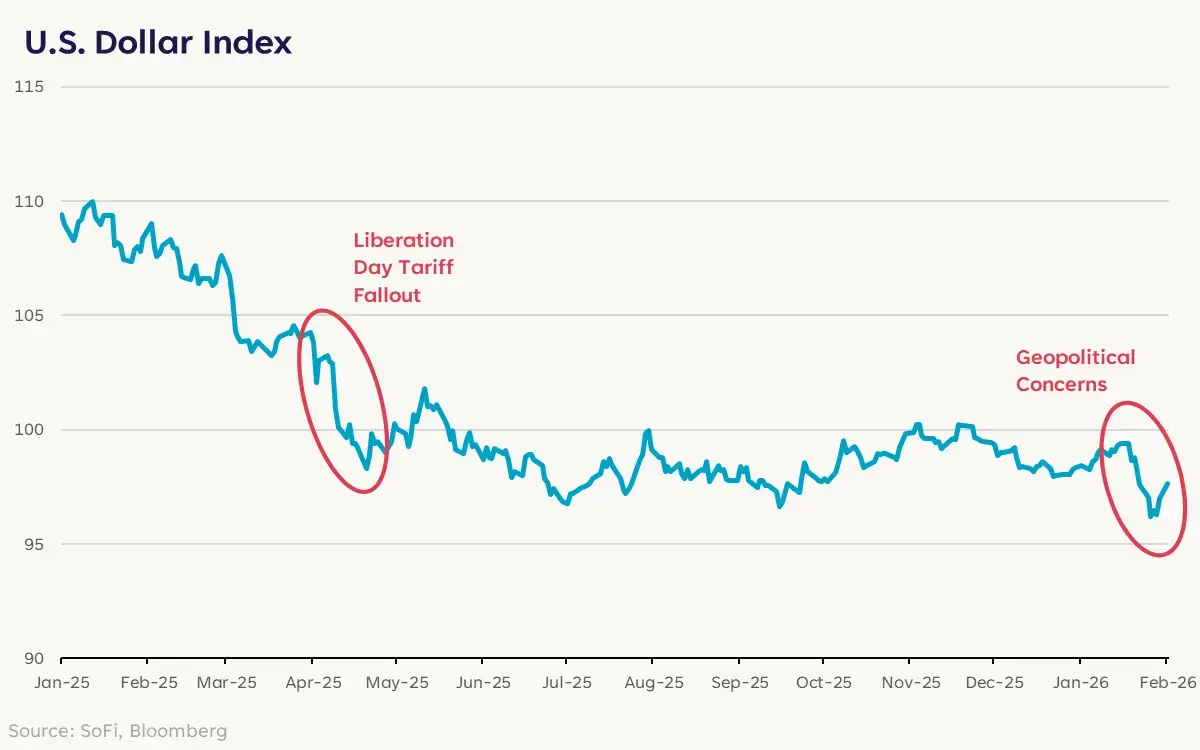

Abroad, the “Sell America” trade gained traction amid U.S. military action in Venezuela, the Trump administration’s interest in acquiring Greenland, and escalating conflict involving Iran. This global rotation away from U.S. assets hasn’t been hard to spot: After falling 9% in 2025, the Dollar Index (DXY) dipped more than 1% in January.

Though it’s hard to say for sure, this year’s developments thus far don’t appear to be just short-term gyrations, but instead a symptom of longer-term, structural shifts in the global order.

Tangible Asset Boom

The politicization of the Fed and the geopolitical fracturing are manifesting themselves in the flow of capital to hard assets.

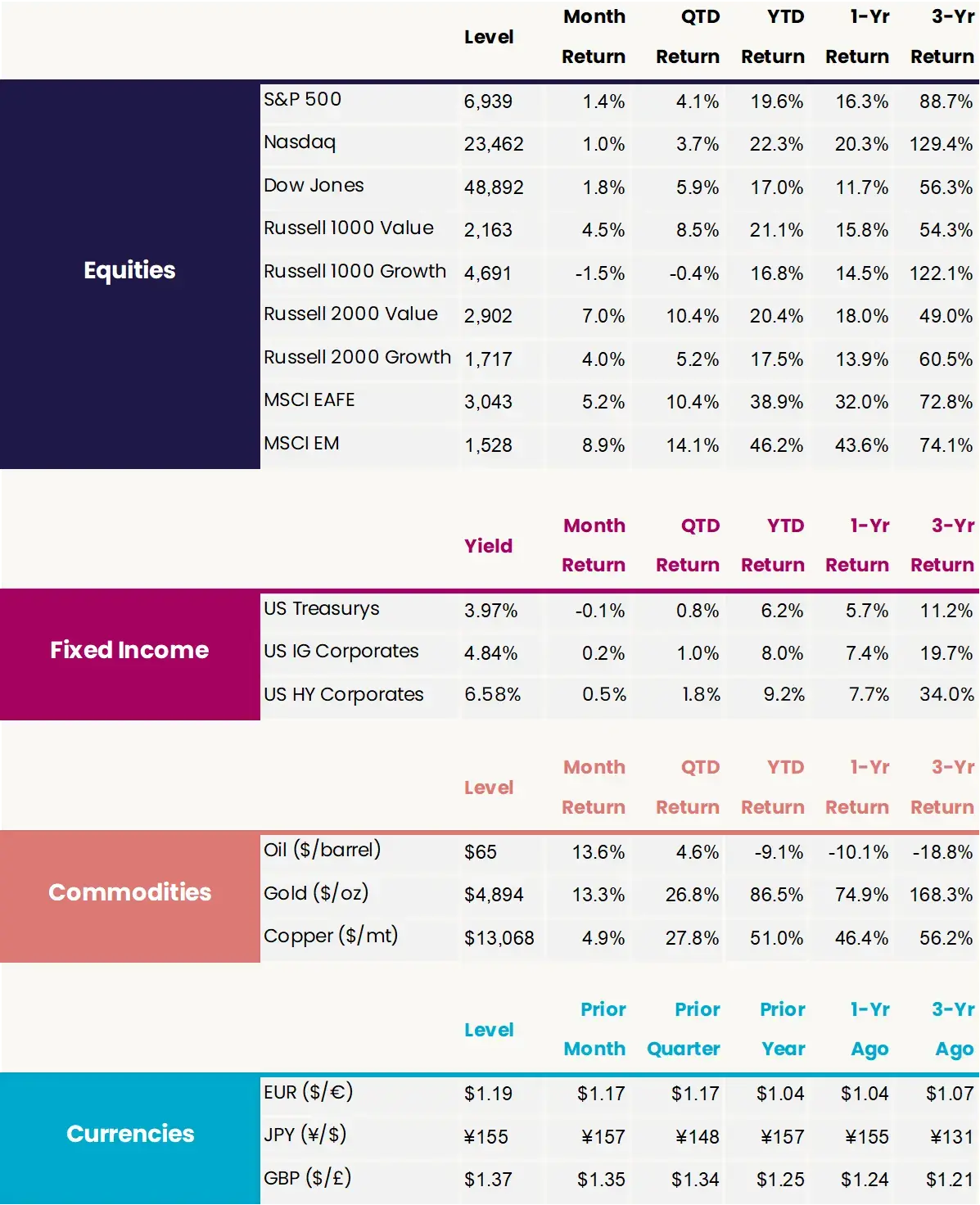

Gold, for instance, rose to as high as $5,595/oz on Jan. 29, before ending the month at $4,894/oz, up 13%. For years, the precious metal has benefited from foreign central banks and governments looking to diversify their reserves in response to geopolitical uncertainty. More recently, however, it has been buoyed by the emergence of new strategic buyers such as Tether and increased popularity of metals among retail traders.

For as good a month as Gold had, Silver had an even better one. It began the month at $71/oz, rose as high as $121/oz on Jan. 29, and then finished at $85/oz, up 19%. The jump was catalyzed by a perfect storm of industrial demand, resource nationalism and, of course, retail interest. China, which controls more than half of global silver refining, implemented strict export licenses to protect its own supply chain. Because silver is used in AI server nodes and other high-tech goods, this kicked off a supply squeeze in the global commodity market.

In fact, because Silver prices rose faster than Gold prices, the Gold to Silver ratio fell to as low as 46, its lowest level since 2011. The long-term average is roughly 70.

Some might argue a lower Gold/Silver ratio is justified by a fundamental change in the supply and demand dynamic, but the size and speed of Silver’s increase suggests that any pullbacks could be quite significant — and unsurprising.

Market Recap

Macro

• President Trump announced Kevin Warsh as his nominee to be the next chair of the Federal Reserve.

• The Federal Reserve left the fed funds rate unchanged at a target range of 3.50%-3.75%, adopting a wait-and-see approach to whether further cuts are needed.

• The December Employment Situation report showed 50k jobs were added and the unemployment rate fell to 4.4%.

• According to the Atlanta Fed’s GDPNow model, fourth-quarter GDP growth is tracking to an annualized 4.2%.

• Oil prices rose 14.5%, as rising geopolitical risks and solid economic data reduced supply glut concerns.

• The supply squeeze in silver continued, finishing the month up 19% despite a major pullback to finish the month. Gold’s multi-year uptrend continued as well, with the precious metal finishing the month up 13%.

• The U.S. Dollar depreciated 1.4% against a basket of major currencies, the biggest decline since August.

Equities

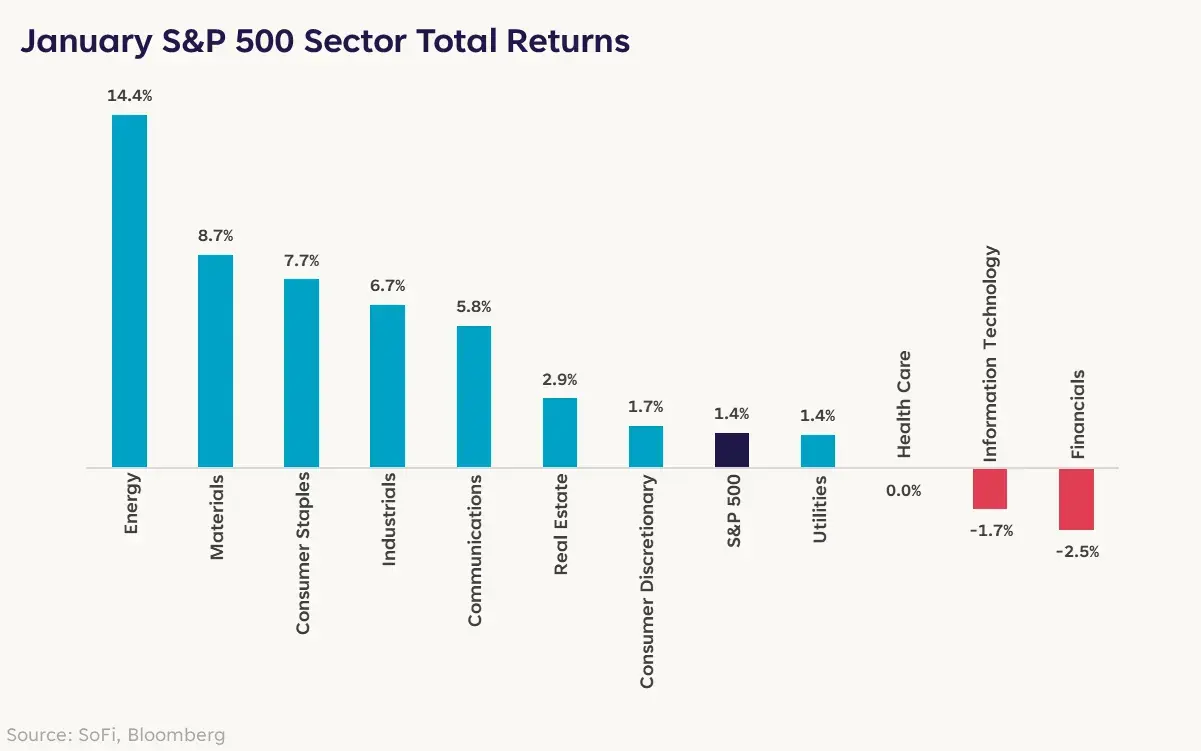

• Energy stocks returned 14.4% in January, their best month since October 2022.

• Buoyed by U.S. Dollar weakness and a strong month for commodities, emerging market stocks rose 8.9% and beat the S&P 500 by 7.4 percentage points. That’s the best relative performance since November 2022.

• Already one of the best performing factors in 2025, the Momentum factor (i.e. the top performing stocks of the last 12 months minus the bottom stocks) was on top of the leaderboards in January, with a return of 2.5%. Meanwhile, Low Volatility stocks fell 7.3%.

• Value stocks beat growth stocks by 5.9 percentage points and small-cap stocks beat large-cap stocks by 4.0 percentage points.

Fixed Income

• 10-year breakeven inflation expectations rose nearly 10 basis points.

• Japan’s bond market saw intense volatility, with its 30-year government yield rising from 3.39% to as high as 3.86% on Jan. 20, before ending the month at 3.63%.

SoFi can’t guarantee future financial performance, and past performance is no indication of future success. This information isn’t financial advice. Investment decisions should be based on specific financial needs, goals and risk appetite. Information is obtained from sources and data considered to be reliable, but its accuracy and completeness is not guaranteed by SoFi.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Mario Ismailanji is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Form ADV 2A is available at www.sofi.com/legal/adv.